Carbon Market Strategist - EUA prices show signs of stabilization as we enter summer period

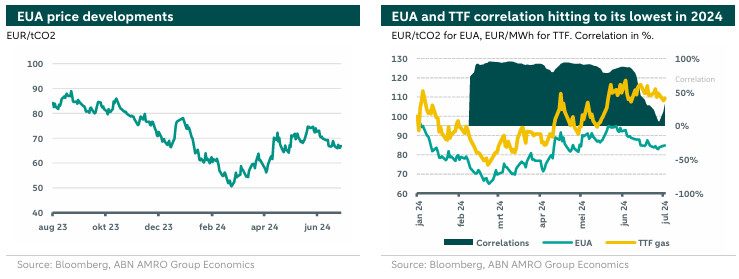

Carbon prices leveled out after the decision on Total Number of Allowance in Circulation (TNAC) was announced Early June. They further manifested a downward trend as EUA prices decouple from European gas prices.

Emissions from power generation retain its downward trend, while Eurozone PMI composite shows weak signs of industrial recovery

Market sentiment is still bearish on the outlook for EUA prices

As we approach the summer period, we expect the EUA price to range between 65-70 EUR/tCO2 during July, though markets remain responsive to extreme weather or geopolitical tensions

EUA prices averaged 68.4 EUR/tCO2 in June. The European Commission’s decision on TNAC on 1 June entailed supply tightening but was not enough to totally wipe out the surplus in the market. Meanwhile, EUA prices witnessed a decoupling to gas prices during June. Demand from main sectors remains weak and the bearish sentiment is back. EUAs are trading at 67.43 EUR/tCO2, at the time of writing.

On 1 June the commission announced the TNAC of around 1112 million (see our previous note here) which was not enough to completely eliminate the surplus in the market driven mainly by the front-loading under REPowerEU package. This, however, removed the supply uncertainty in the market. As a result, the market showed signs of relief and the focus was back to the fundamentals. The EUA prices started to decouple from the gas markets, with EUA and TTF correlation hitting its lowest level of 6% since the start of 2024, which is manifested in the chart below (right). Accordingly, EUA prices started to show a downward trend as can be seen in the left-hand chart below. This downward trend is further supported by several other factors.

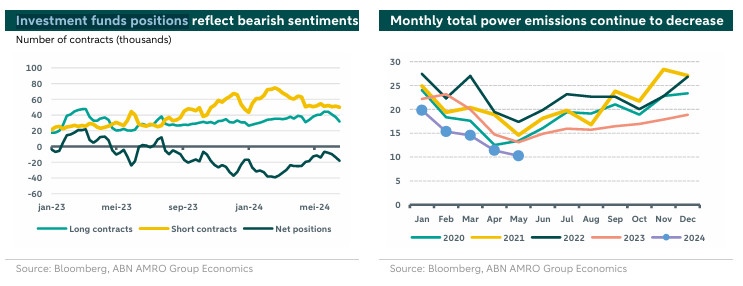

First, monthly emissions from the power sector kept its downward trend with renewables holding higher share in the electricity mix and coal and gas power generation going down. This is evident in the graph below (right).

Second, another important driver for prices is the state of the industry. There were still no signs of recovery in June in industrial production. Indeed, the main indicators such as the composite Purchasing Power Index (PMI) for the Eurozone, declined compared to May, but stayed in expansionary territory (at 50.8, down from 52.2 in May). The main driver for this decline was weak demand as subcomponents for demand such as new orders in the manufacturing PMI and the new business subcomponent of the services PMI declined considerably (see our note on Eurozone PMI here).

Third, market sentiment is still bearish on the outlook for EUA prices with indicators leaning to the bearish territory. This is evident in the chart below (left) where net short positions by investment funds have increased. This increase in net short positions is driven by lower long contracts, with short contracts remaining relatively constant. So investors that held a positive view on prices have reduced their positions while a large majority of investors remain negative on prices

Outlook

As we enter the summer period, carbon markets are expected to be relatively stable but still responsive to some weather conditions, such as heat waves or slow wind which would decrease renewables output and increase the need for conventional power generation. Furthermore, impacts of geopolitical tensions on energy markets might still spillover to carbon prices especially in the event of escalation in the war in the Middle-East to involve Iran. Finally, as we approach the coming surrender date for 2023 emissions (30 September 2024), we might witness a rise in demand for EUAs from installations aiming to cover their emissions for 2023. However, we expect such impact to be limited given the current market conditions and since given that the total emissions for 2023 were relatively low. Accordingly, our outlook for the EUA price is neutral with a price range between 65-70 EUR/tCO2 during July.