China - After resilience comes the slowdown … and more support

Q2 GDP data showed a remarkable resilience, with exports holding up despite tariff war … but recent activity data confirm domestic imbalances, and weakening growth momentum. Beijing focuses on ‘excessive competition’; additional demand support still likely.

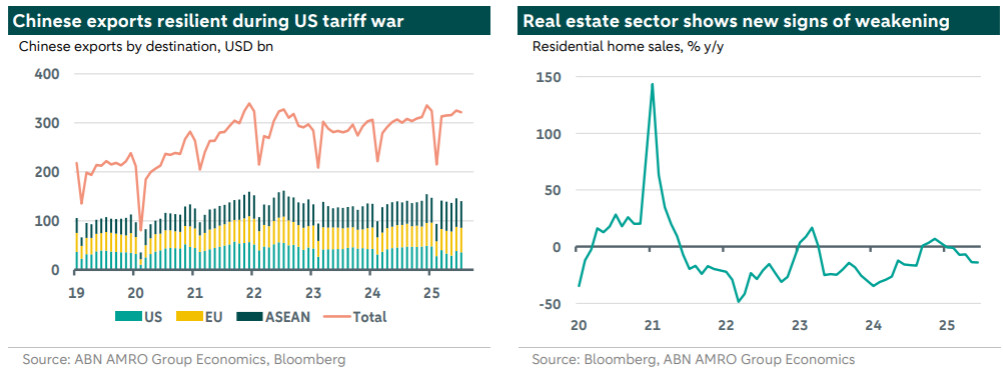

Q2 GDP data showed a remarkable resilience on the external front…

Considering how the second quarter started, with US-China tariffs initially skyrocketing in the post-US ‘Liberation Day’ escalation, the Chinese economy has been remarkably resilient. Quarterly growth slowed marginally to 1.1% q/q (Q1: 1.2%) and annual growth to 5.2% y/y (Q1: 5.4%). Exports held up well despite tariffs. The drop in direct exports to the US in April/May following the tariff escalation was offset by trade rerouting and reorientation, with exchange rate and inflation developments supporting competitiveness. Following the Geneva truce agreed mid-May. which reduced new US tariffs from 145% to 30%, Chinese exports to the US recovered a bit in June/July. Although US-China tensions flared up from time to time since, with the focus shifting from tariffs to chokepoints (see here), talks in London (June) and Stockholm (July) confirmed the status quo, in line with our expectations. The tariff pause has now been extended until mid-November, and there are talks of a potential meeting between presidents Trump and Xi in late October.

…but recent activity data confirm domestic imbalances and a weakening momentum

Despite this external resilience, domestic imbalances remain. Except for foreign trade, July data surprised to the downside, and pointed to weaker momentum. Retail sales slowed more than expected, with the effects of consumer subsidies fading. Particularly striking was the turnaround in fixed investment, with manufacturing investment cooling sharply and infrastructure investment showing a rare monthly contraction. Next to some specific, technical issues, the crackdown on so-called disorderly (‘involutionary’) competition seems to be a key driver (see below). Deflationary pressures are also still abundant (ongoing producer price deflation and weak corporate profitability go hand in hand), although core inflation rose to a 17-month high of 0.8% y/y. The negative feedback loop from real estate to demand has not yet been broken, with the annual contraction in property investment and new home sales deepening. The labour market also shows signs of weakness, with the jobless rate picking up to 5.2% in July (June: 5.0%).

Beijing focuses on ‘excessive competition’; additional demand support still likely

Beijing’s recent crackdown on excessive competition aims to fight deflation and restore corporate profitability by trying to prevent aggressive price wars in some sectors (like EVs) and to keep supply abundance in check. It remains questionable to what extent this crackdown will be effective, as the deflationary environment is in the first place a function of broad supply-demand imbalances, and previous crackdown policies haven often caused counterproductive side effects on confidence and demand. Although we have marginally raised our 2025 growth forecast (to 4.9%, from 4.7%) on resilient Q2 GDP data, we still expect (annual) growth to slow materially in 2H-2025, partly reflecting base effects from last year. All in all, we still expect more fiscal support and piecemeal monetary easing aimed at stabilising domestic demand, the key policy goal for 2025, with the July data likely adding some sense of urgency. In fact, recent announcements already point to a stepping up of specific income support for households. Stabilising property will also remain a focus area, with plans to create room for SOEs to buy unsold homes from developers now floating around.