China: Dealing with Omicron and ‘dynamic clearing’

Quarterly growth will drop in Q1 compared to Q4, but improving growth momentum is on the cards. Omicron reduces gains from the shift in covid-19 policy from ‘zero cases’ to ‘dynamic clearing’. Falling inflationary pressures leaves room for further targeted easing including for real estate.

After a pick-up in Q4-2021, we expect quarterly growth to fall back in Q1, with drags from real estate and strict covid-19 policies remaining. That said, we expect qoq growth to pick-up in the course of this year and to be on average higher than last year. We think annual growth bottomed at 4.0% yoy in Q4-2021 and will accelerate towards around 5.5% yoy in the second half of this year. That would leave full-year growth for 2022 at 5.1%. China’s official growth target for this year will be announced at the National People’s Congress in early March. Our expectation of improving growth momentum in the course of this year is partly based on the assumption that the authorities will continue with targeted, piecemeal monetary and fiscal easing and a relaxation of macroprudential regulations, including for real estate.

Omicron reduces gains from the shift in covid-19 policy from ‘zero cases’ to ‘dynamic clearing’

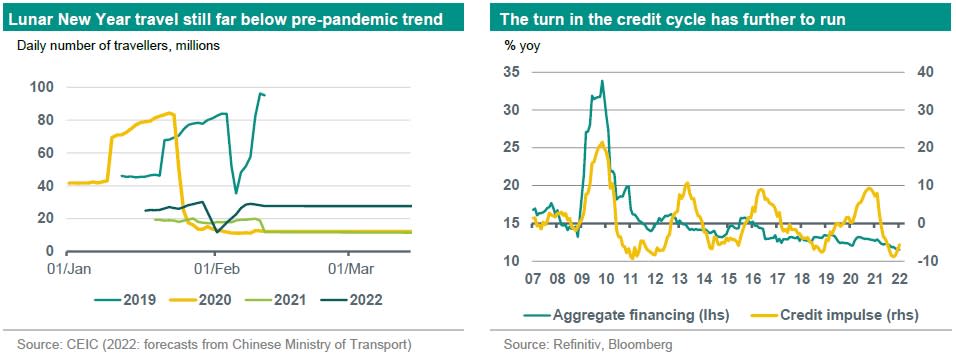

Due to the Chinese New Year (this year scheduled in early February) economic data from China are relatively scarce this month, with the monthly activity and foreign trade data for January/February combined being published in March. Still, from the data that are available we can conclude that the move in covid-19 policy from a centralised ‘aim for zero cases’ approach to decentralised ‘dynamic clearing’ (quickly contain local outbreaks) has been less supportive for consumer services than the authorities had hoped for. In 2021, the central government told people not to travel during the holiday break. This year, such decisions were delegated to local governments. However, due to the spread of Omicron – and the example of Xi’an – local governments became cautious. The result is that travel volume during the LNY break rose by over 30% compared to last year, but remained far below pre-pandemic levels. Tourism spending was actually lower compared to a year ago. All in all, we think that quarterly growth will fall back in Q1-22, after a pick-up in Q4-21, but will be higher than in Q1-21. The January PMIs also pointed in that direction, with the composite indices from both NBS and Caixin dropping significantly (see here).

Falling inflationary pressures leaves room for further targeted, piecemeal policy easing including for real estate

Our expectation that, going forward, growth momentum will improve compared to Q1 partly rests on the assumption of further targeted policy support. Pipeline inflation pressures are easing, although renewed commodity price rises could lead to hiccups (see for more background here). Consumer price inflation fell to below 1% yoy in January. We expect CPI inflation to bounce back in the course of this year, but to remain below the PBoC’s 3% target. All of this leaves the authorities room to add some more piecemeal, targeted monetary and fiscal stimulus and a cautious relaxation of macroprudential regulation (including for real estate), to stabilize growth in a politically important year for the leadership. Moreover, while the credit cycle has already bottomed out and lending growth has begun to stabilize, some more easing seems warranted to realise a modest acceleration in lending growth and to contain the prevailing drags from real estate.