Eurozone economy stayed resilient at the end of 2025

Q4 growth figures in the eurozone suprise to the upside in the final quarter of 2025.

Eurozone economy stayed resilient at the end of 2025

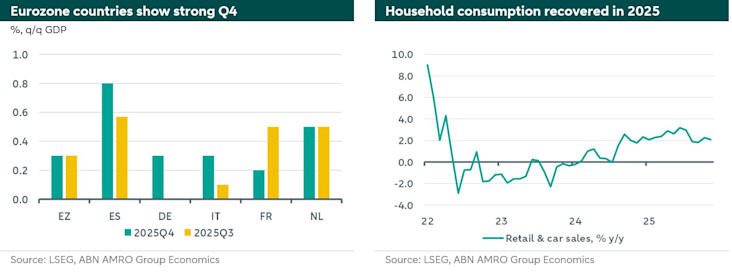

Eurozone GDP surprised to the upside in Q4 at 0.3% q/q, above our (0.1%) and consensus (0.2%) forecasts. Incoming data had already suggested strength in the domestic economy (see ), but we expected net exports to have been more of a drag. We do not have the full details for the eurozone aggregate, but piecing together the details from some individual countries suggests that household consumption and government spending were significant drivers of growth in Q4, while net exports were a drag in most countries – with some exceptions such as the Netherlands (see below) and France (the latter largely due to falling imports). Looking at country level data, GDP growth was particularly strong again in Spain (0.8% q/q), while France was surprisingly solid (0.2%) considering this came after an already very strong Q3 (0.5%). This suggests the private sector appeared to shrug off the uncertainty surrounding the 2026 budget wrangles.

All told, the eurozone economy continues to be resilient in the face of extraordinary uncertainty and US tariffs. We expect the latter to continue to weigh on exports over the coming months, keeping a lid on headline GDP growth, but we expect the domestic economy to continue to firm this year on the back of rising German government spending, and reduced caution on the part of households and businesses. Indeed, the strength on the domestic side coming out of 2025 bodes well for 2026.

Germany – Solid Q4 Momentum Paves the Way for Stronger Growth in 2026

The German economy also contributed to the upside surprise of the eurozone aggregate. Indeed Q4 GDP in Europe’s biggest economy expanded by 0.3% q/q, up from 0.2% q/q in the preliminary estimate of Destatis and above consensus. Although details on subcomponents are still limited, the headline GDP figure appears broadly in line with most eurozone peers, with household consumption and government spending serving as the main drivers of growth. This means 2025 growth landed at 0.3% after two consecutive years of recession. Where aggregate figures might signal some relief, the German business sector however is not out of the woods yet. Key sectors such as manufacturing and construction still saw decreases in annual value-added and most recent bankruptcy data, roughly at level on par with 2014, still signal an ongoing upward trend.

For 2026, we expect growth to pick up as federal fiscal spending gains traction and strengthens domestic demand, supported by contributions from private consumption. Exports, however, are likely to remain weak. Although demand in key export markets is expected to improve, German exporters are set to benefit only marginally. Price competitiveness has eroded in recent years, reflected in a declining share of global export market share, while a stronger euro and the tariffs further weigh on the outlook. For now, we are maintaining our annual growth forecast at 0.9%.

Netherlands — A Strong Finish to a Strong Year as the Coalition Agreement Is Presented

Q4 GDP surprised to the upside and grew by 0.5% q/q in the final quarter of 2025 (ABN AMRO 0.3%, consensus 0.3%). Annual growth therefore came in at 1.9% q/q. This means the incoming cabinet, set to present its coalition agreement later today, will take office with an economy that is rather resilient (look out for our note on the coalition agreement later today). Unsurprisingly were strong positive contributions to GDP from private consumption and government consumption, in particular through spending on healthcare. With inflation gradually easing and wage growth in 2026 still expected to be around 4%, Dutch households are experiencing solid gains in purchasing power, which in turn supported higher consumption in 2025 and continues to do so in 2026. However, elevated uncertainty continues to restrain how fully these gains feed into spending, leading consumers to maintain higher savings rates. More surprising was the strong contribution from net exports. The drag in 2025 from tariffs is visible in export values to the US, particularly in value-added heavy exports of Dutch manufactured products, but this is more than offset in export volumes to other countries resulting in an increase in exports of 1.3% q/q. Stronger‑than‑expected growth in Germany (see above), the Netherlands’ main trading partner, may help explain this development. Robust export performance in machinery, in particular, suggests that Dutch chip‑making equipment has been a contributing factor of the export upswing.

For 2026, we expect growth to moderate. Part of this moderation reflects persistent supply‑side constraints – such as electricity grid congestion and nitrogen regulations, which are limiting activity and weighing on growth, while the labour market continues to ease slightly. Our current forecast is 1.2% annual growth, but today’s strong data release adds upward pressure to that figure, reinforced by mechanical carry‑over effects.