Eurozone inflation to continue falling, but will remain elevated

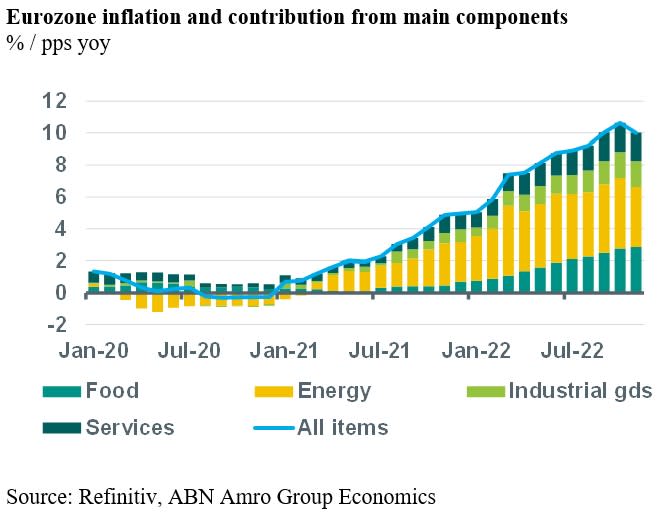

Eurozone inflation declined to 10.0% in November, down from 10.6% in October. The drop was totally due to lower energy price inflation. The inflation rate of food, alcohol and tobacco increased, and core inflation was unchanged. Whereas we expect headline inflation to come down noticeably in the coming months, core inflation probably will be more sticky and decline more slowly.

Eurozone inflation declined to 10.0% in November, down from 10.6% in October. The drop was totally due to lower energy price inflation, which fell to 34.9%, down from 41,5% in October, mainly on the back of the global decline in energy commodity prices. Although global food commodity prices have also declined in recent months, the inflation rate of food, alcohol and tobacco increased to 13.6%, up from 13.1% in October. This rise seems to have been related to past rises in energy and food commodity prices being passed on to consumers with a delay, as processed food price inflation increased (to 13.6%, up from 12.5%) whereas unprocessed food price inflation fell (to 13.8%, down from 15.5%). We expect the declines in energy inflation and unprocessed food price inflation to continue in the coming months, which should further reduce headline inflation. Meanwhile, core inflation stabilised at 5.0% in November. The inflation rate of non-energy industrial goods was unchanged at 6.1%, while the inflation rate of services declined to 4.2%, down from 4.3% in October. Detailed data from Germany suggest that this rise in services price inflation was mainly due to a sharp drop in the inflation rate of package holidays, which tends to be very volatile. Whereas we expect headline inflation to come down noticeably in the coming months, core inflation probably will be more sticky and decline more slowly. Although the drops in food and energy inflation should also reduce the inflation rates of energy-intensive goods and services, we expect this process to be slow, as past rises in food and energy prices still do not seem to have been passed on fully to consumers. That said, non-energy industrial goods price inflation should ease in the coming months, as these prices are mainly driven by global changes in supply and demand for industrial goods, which have become more balanced and should reduce price pressures. But on the other hand, services price inflation (with a weight of more than 60% in core inflation) is expected to remain more elevated. It is more domestically driven and more sensitive to wage growth, which is expected to increase in the next few quarters and decline only gradually in the second half of next year. All in all, inflation should fall noticeably in the coming months, but we expect it to remain elevated and expect it to be at some 5% around the middle of next year.