Gas market update - Markets are trending downwards as winter enters its second half

European gas markets are relaxed with the heating season entering its second half with high storage levels, sustained supplies, and low industrial demand. Impact on prices of attacks in the red sea have been limited but the market remains vigilant to any further escalation. The USA emerges as the world’s top exporter of LNG in 2023.

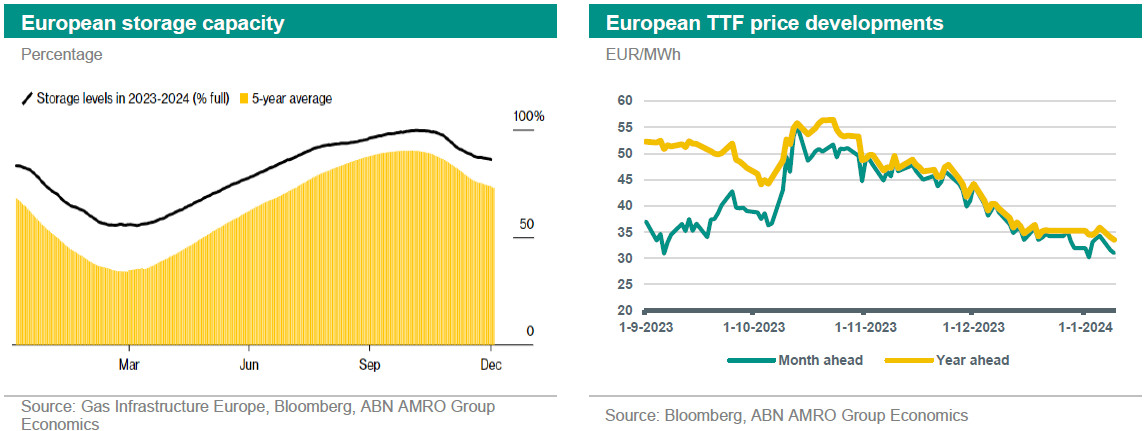

In December and early January, European gas prices sustained the downward trend that has been in place since mid-October. The European month ahead TTF price averaged 35.12 EUR/MWh in the past 40 days, touching a five-month low of 30.57 EUR/MWh. The mild weather and higher than average storage level for this time of year were the main factors that boosted market confidence in the ability of Europe to bypass this winter without any supply disruptions.

Europe’s gas storage level stood at 84.27% at the time of writing, still well above seasonal averages (75% mid-January average) thanks to the low demand for industrial purposes and the mild weather the region has been witnessing so far, which brought down heating consumption.

So far the impact on prices of the attacks on cargos by Al-Houthi group has been limited, but the market remains vigilant to any escalation that could impact the LNG tankers passing through the Red Sea towards Europe.

From the LNG supply side, 2023 witnessed the emergence of the USA as the world’s top exporter of LNG, overtaking the exports of Qatar and Australia. The increase in the US output was mainly driven by the restart of in Texas. Furthermore, the USA become Europe biggest LNG supplier with a share reaching 45% in 2023.

One development that could affect the European gas market in the coming months is the extension of the EU-ETS to the shipping sector in the EU, which will increase the cost of LNG shipping to the continent and put an upward pressure on the price.

Industrial demand for gas has been low with the economy slowing down driven by high interest rates. These rates are not expected to be cut until the middle of 2024. Moreover, output from renewable power resources have been increasing with more deployments of solar and wind projects, which reduces gas demand for conventional power generation. Saving measures have also played a role in demand destruction which seems to be more sustainable than previously anticipated. Furthermore, now that the heating season has entered its second half with a strong buffer, worries about supply disruptions have weakened. Therefore, the impacts of cold spells on prices are becoming less severe, weakening the price reaction to temperature fluctuations.

Outlook

Given the aforementioned developments, our outlook for the TTF year ahead contract is to average around 35 EUR/MWh during the first quarter of 2024. As the industrial demand starts to bottom out, the anticipation of economic recovery spurred by the anticipated cuts in interest rates in the second half of 2024, should see gas prices reaching 40 EUR/MWh by the end of 2024 (1).

(1) Assuming storage will be filled in time and that no supply disruptions will take place as the continent enters next winter.