Key views - Global Monthly October 23

The global economy continues to send mixed signals, with weakness in the eurozone contrasting with strength in the US. Meanwhile, China’s GDP growth picked up in Q3 following a weak Q2, despite ongoing property sector weakness. The impact of monetary tightening is being increasingly felt, with manufacturing and housing in a downturn. Tightening credit conditions are weighing on bank lending, while the rise in bond yields forms another headwind. Headline inflation has continued to trend lower, but higher oil prices are temporarily slowing the return to central bank targets, and tight labour markets are keeping core inflation elevated. Central bank policy rates are peaking, but even with rate cuts starting in the first half of next year, we expect monetary policy to stay restrictive throughout 2024. This will keep a lid on any post-slowdown rebound.

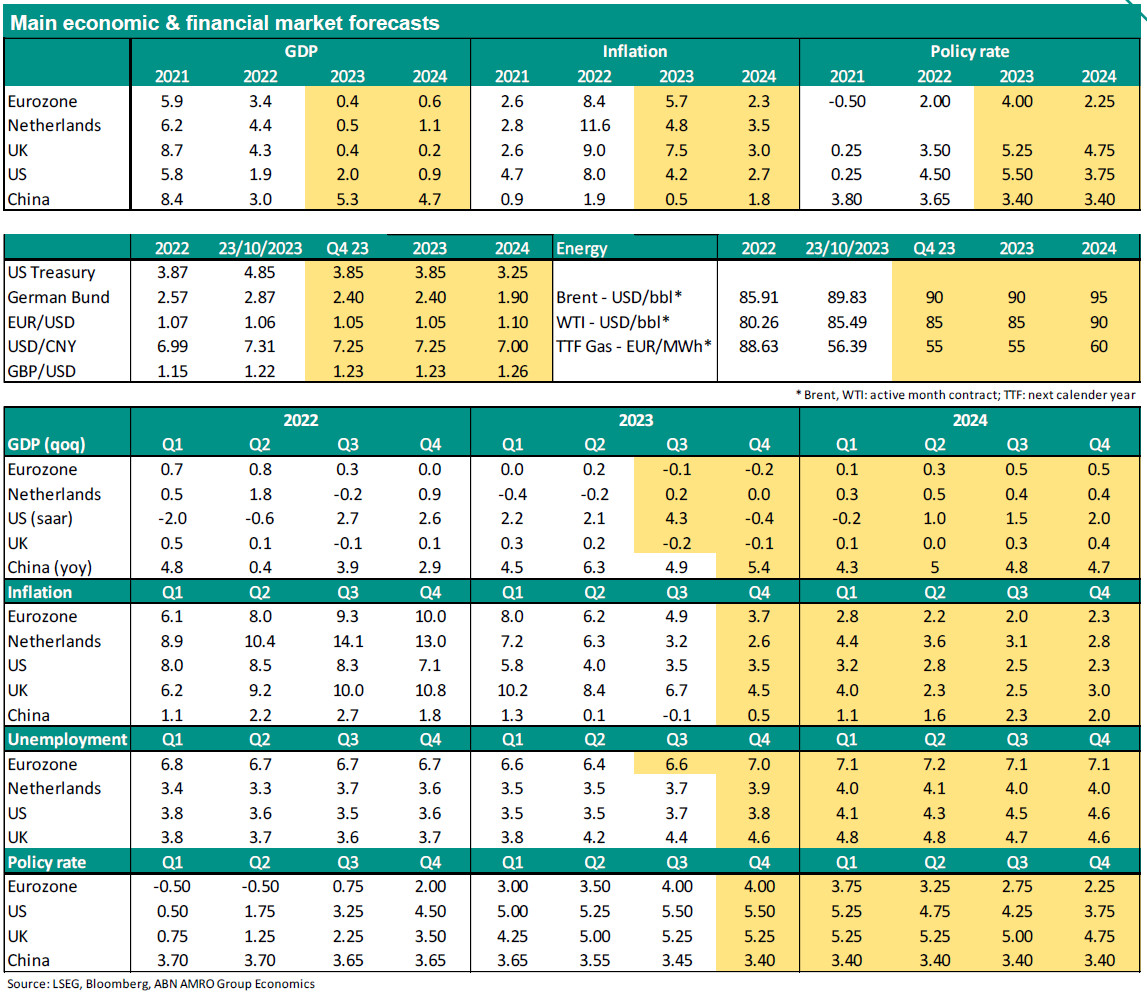

Macro

Eurozone – Economic data and surveys published so far for July-September indicate that GDP probably contracted moderately or stagnated in Q3. The volume of goods consumption, industrial production and construction all declined on a 3Mo3M basis in August. Also, the low level of producer confidence, the rise in interest rates and tighter bank lending standards suggest sluggish private fixed investment. Disinflation has gathered momentum, with the headline and core rate both declining markedly in September. Despite the recent rise in energy prices, inflation is expected to continue to decline this year and the next. Core inflation should fall to around 2% by mid-2024.

The Netherlands – GDP contracted in the first two quarters of 2023 which means the Dutch economy is officially in a technical recession. We expect growth to resume but remain sluggish in the coming quarters on the back of higher rates and lower external demand. Dutch GDP growth is expected to average 0.5% in 2023. The Dutch economy remains resilient; the labour market is still tight and bankruptcies – although increasing in recent months – are still below 2019 levels. We expect inflation (HICP) to average 4.8% in 2023 and 3.5% in 2024.

UK – Disinflation has continued, providing some relief to the Bank of England, but upside inflation risks remain significant given that wage growth is still elevated and well above levels consistent with the 2% target. At the same time, unemployment has started rising, and we expect a softening in demand to dampen wage growth over time. The economy is expected to broadly stagnate over the coming year or so, weighed by tight monetary policy.

US – Growth remains strong for now, but headwinds for the economy are building, including from the restart of student loan repayments, and tighter financial conditions stemming from the bond yield surge. We expect a sharp slowdown in Q4, with the risk of a contraction. While higher oil prices are boosting headline inflation, wage growth has peaked, and we judge that a slowdown and a period of below trend growth will be sufficient to return inflation back to target. Inflation falling sustainably back to target hinges on a rise in unemployment over the coming year.

China – Despite ongoing distress in the property sector, Q3 GDP came in stronger than consensus expectations, although closer to ours. With support measures filtering through, quarterly growth rose to 1.3% qoq (Q2: 0.5%). Annual growth slowed to 4.9% yoy (Q2: 6.3%), but that was mainly due to a base effect from last year. September macro data also pointed to an improving momentum, but property sector data remained weak. All in all, China’s growth target of 5% is within reach, but given remaining headwinds we expect growth to dip below 5% next year.

Central Banks & Markets

ECB – Following the policy rate hike in September, the ECB has probably done enough and we think the rate hike cycle may be over now. Although the recent rise in energy prices will have an upward impact on headline inflation, it also means a weaker economic outlook, which is already quite bleak at the moment. Nevertheless, the ECB probably will keep rates at their current level for a while. We expect a pivot in ECB policy around March 2024, when we expect a rate cut cycle to begin. We see the deposit rate at 2.25% by the end of 2024.

Fed – The FOMC kept rates on hold in September, but the Committee made clear that it is open to further tightening. We think July was the last hike of the cycle, and that benign core inflation readings will give the FOMC the confidence to keep policy on hold over the coming months. We continue to expect the Fed to start cutting rates from next March. Falling inflation will push real rates higher, and the recent jump in bond yields also represents a significant tightening in financial conditions. Even with rate cuts starting next year, monetary policy is expected to remain restrictive throughout 2024 and even into 2025.

Bank of England – The MPC kept policy on hold in September, in a knife-edge vote. We now think Bank Rate has peaked at 5.25%. However, we would not rule out one last rate hike if inflation springs another upside surprise. The BoE is in full data-dependent mode, and UK macro data has been erratic over the past few months. We do not expect rate cuts until next August, and there is a risk that rate cuts get delayed even further, if inflation proves to be more persistent.

Bond yields – The ‘’higher-for-longer’’ theme remains well anchored in the rates market. Recent geopolitical events led to further inflation concerns which drove bond yields even higher rather than triggering a rise in safe-haven demand. Given our macro and central bank view, we judge the 10y yield development to be overdone. We expect rates to have reached their peak and to decline by year-end and throughout most of 2024. Looking at current rate levels, it’s increasingly evident that a more dramatic shift in the central banks’ narrative will be needed to generate a sustained turnaround in yields and meet our base forecast.

FX – Compared to the forecasts published in our previous (September) Global Monthly, we have downgraded our year-end EUR/USD forecast to 1.05, from 1.08. For end-2024, we upgraded our EUR/USD forecast to 1.10, from 1.05. Following these changes in our US dollar forecasts, we have also revised the forecasts for most of the other major currencies, as well as for the key emerging market currencies that we cover (Chinese yuan, Brazilian real, Polish zloty).