US and eurozone growth downgrades

Following the significant changes to our central bank views last week, we have made major downgrades to our macro scenarios for the eurozone and the US.

Growth to slow to sub-trend in the eurozone; stagnation in the US

Following the significant changes to our central bank views last week, we have made major downgrades to our macro scenarios for the eurozone and the US. Our most important changes are to 2023 growth forecasts. In the eurozone, we now expect growth of 1.3% in 2023, down from 1.7% previously. In the US, we have made an even bigger downgrade, also to 1.3% but from a higher previous forecast of 2.2%. On a quarterly basis, we expect growth to slow to sub-trend rates in the eurozone following pandemic-related catch-up growth in 2022, while in the US we expect the sharp rises in interest rates to lead to broadly stagnant growth already in the second half of 2022 and in the first half of 2023. We do not expect recessions according to the strict definition of two consecutive quarterly contractions in output, but given the broader recession definition used in the US used by the NBER, its could well call a recession next year given the rise in unemployment that we foresee in the US. In any case, we continue to think the combination of very strong household balance sheets and significant buffers in the economy will prevent a prolonged or deep downturn of the kind seen in 2008 or 2020; instead, any downturn is more likely to resemble the early 2000s recession following the dot-com bust in the US, which was comparatively mild. In addition to growth forecast changes, we have also made further upgrades to our inflation forecasts. While forecast upgrades continue to be driven largely by the supply-side, the risk this is posing to inflation expectations is one of the main reasons we expect much more aggressive central bank policy tightening (and therefore weaker growth). We describe our scenarios in more detail for each region below, and will communicate more in our June Global Monthly, out later this month.

Eurozone: Sub-trend growth in 2023 following the pandemic rebound of 2022

Eurozone GDP growth in 2022 will probably turn out somewhat higher than we expected before (around 2.9% compared to our earlier forecast of 2.6%). This change is mainly due to upward revisions of previous quarterly growth numbers by Eurostat. For instance, growth in 2022Q1 was revised higher to 0.6% qoq from an initial estimate of 0.3%. We have kept the quarterly growth pattern for 2022Q2-Q4 largely unchanged. We still expect growth to be weak in Q2 but to rise to above the trend rate in 2022H2, as the easing of supply chain bottlenecks and the ongoing recovery of services consumption should result in a temporary bounce in production and spending. However, moving into 2023 growth should slow down noticeably, probably to levels well below the trend rate. By then, consumers should have spent most of the savings that they accumulated during the pandemic. Consumption growth is expected to be supported by robust employment growth in 2022, but the outlook for the labour market should deteriorate towards the end of the year. Moreover, temporary catch-up effects in industrial production and fixed investment will fade. On top of that, eurozone domestic spending as well as global trade will slow down on the back of the more aggressive interest rate hikes by the Fed and ECB, which will result in global financial conditions tightening more than we estimated before. We have roughly halved our quarterly growth numbers for 2023, to around 0.1-0.2% qoq. As a result, our annual average growth estimate declines to around 1.3%, down from 1.7%. Our new growth estimate for 2023 is well below the ECB’s June projection (2.1%), but not that far below the OECD’s June Economic Outlook (1.6%). Eurozone inflation came in higher than expected in May, at 8.1%, up from 7.4% in April. Although the rise in inflation continued to be driven by energy and food prices, core inflation increased as well. Services price inflation is currently being lifted by normalisation of holiday and leisure prices as well as the pass-through from high food and energy prices into, for instance, transportation services and restaurant and catering services. Meanwhile, supply chain disruptions and high energy prices also contribute to higher non-energy industrial goods price inflation. Recent trends in commodity markets suggests that food and energy inflation will move even higher in the months ahead, but should start to decline in the Autumn. This will also reduce the energy-related rises in goods and services inflation. Wage growth is expected to increase this year and next, but the upward impact on underlying inflation will be moderate as labour productivity is expected to increase as well. Moreover, the deteriorating economic growth outlook should limit wage growth in 2023, as labour market conditions become less rosy. We expect the unemployment rate to rise somewhat next year. All in all, we expect inflation to be around 7.4% on average in 2022 (around a full percentage point higher than our previous forecast) and 3.7% in 2023 (previous forecast was 2.5%). By the end of next year, inflation could already fall to levels close to the ECB’s symmetric 2% target.

US: Underlying growth to stagnate after a strong Q2

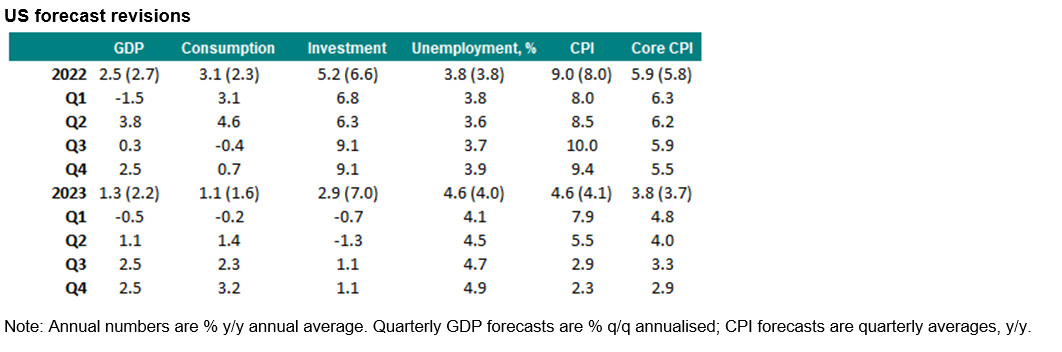

Demand indicators so far in Q2 have been very strong, with private consumption suggesting continued above-trend demand for goods, and services continuing to recover back towards trend. Alongside an improvement in net exports, we expect this to drive a 3.8% annualised rise in GDP in Q2, following the 1.5% contraction in Q1. As we move into the second half of the year, however, we expect the growth environment to deteriorate. The deepening inflation hit to real incomes, combined with the tightening effect of higher interest rates – which is already hitting many households via higher mortgage payments and reduced net wealth via stock market declines – is likely to lead to broadly stagnant consumption (i.e. near zero growth) over the coming quarters. Fixed investment will be supported in the near-term by catch-up from the pandemic, as the supply-side continues to recover, but we expect investment to subsequently contract in the first half of next year. The headline growth picture is complicated by the supply-side disruptions and pandemic recovery distortions, and as such headline GDP growth is likely to continue to be volatile over the next few quarters on the back of swings in inventories and net exports. In the current environment, it is therefore better to focus on underlying demand (consumption and investment) and not put too much weight on the precise quarterly profile we lay out here.

The projected weakening in demand is likely to lead to some rise in unemployment, probably beginning in late Q3 this year and picking up pace in Q4/Q1 next year. Our new base case is that unemployment peaks at c.5% in early 2024 from 3.6% as of May. This, combined with a significant fall in job vacancies, should bring the unemployed-job vacancy ratio down to below 1 by late next year from around 2 at present. This ratio has become a key metric for the Fed, as it reflects the significant supply-demand imbalance in the labour market that is risking a de-anchoring of inflation expectations. Finally, on inflation itself, we have made a further upward revision to our 2022 annual average forecast to 9.0% y/y from 8.0% previously, and expect more of this strength to carry over into 2023, with inflation expected to average 4.6% (previously 4.1%). The Fed’s key focus is on month-on-month readings, and here we expect readings to remain far above levels consistent with the Fed’s 2% target for much of the remainder of 2022. Thereafter, the weaker labour market should drive a sufficient cooling in inflation by Q2 2023 to convince the FOMC that it has tightened policy enough.