Bond sell-off is far advanced

We set out our updated government bond market forecasts following the repercussions of Russia’s invasion of Ukraine. The adjustments are relatively modest, given that central banks are still generally on the path of policy normalisation, while we are seeing higher inflation on the one hand and lower economic growth on the other.

Co-author: Jolien van den Ende

(see our Global Monthly note here). While we think there is still room for yields to rise generally, we see the bond sell-off as being quite far advanced, given that markets are already pricing in an aggressive trajectory for policy rate hikes.

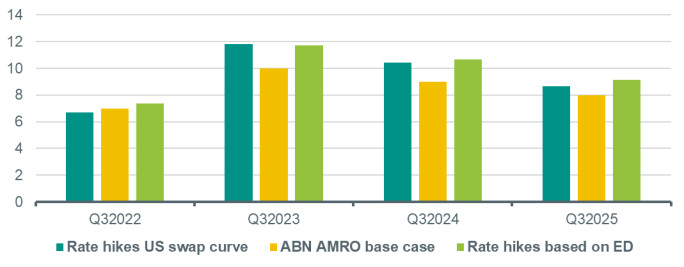

US Treasury yields to move slightly higher during the course of 2022- We brought forward the rate hike cycle in the US, but kept the peak in the fed funds rate at around 2.5-2.75%. Indeed, we now expect an even steeper rise in the fed funds rate, with 50bp steps in both May and June. Thereafter, we expect the Fed to switch to a more gradual pace of 25bp hikes at each meeting until a terminal level of 2.5-2.75% in early 2023 (See here: Fed to start hiking in 50bp steps). On the back of this we have revised our short term rates upwards, especially the 2y US treasury yield which we forecast now at 2.6% at year-end. Moreover, the market is already quite advanced in pricing in an aggressive rate hike cycle by the Fed as shown in the graph below. As a result, we expect the 2y Treasury yield to increase by about 15bp during the course of this year.

The market is well advanced with pricing in an aggressive rate hike cycle in the US

Source: ABN AMRO Group Economics, Bloomberg

Longer term US Treasury yields will settle at around the eventual peak in the fed funds rate, but well ahead. Consequently, the peak in the fed funds rate was already reflected in our US rates forecast. Nevertheless, we have revised the 10y US treasury yield slightly upwards by 10bp to 2.7% at the end of this year to take into account the impact of the balance sheet run-off by the Fed, which we expect to have a positive impact on the term premia, though it will be a slow adjustment given the stock effect. (Jolien van den Ende, Bill Diviney, Nick Kounis)

Bund yields have reached their peak for now – We have revised our forecast for the 10y Bund yield at the end of 2022 upwards from 0.5% to 0.6%, as the correlation between the 10y US treasury yield and the Bund yield seems to be higher than initially thought. We expect the 10y Bund yield to move sideways from current levels with spikes in between. Indeed, we expect that the downward impact of the pricing out of multiple rate hikes in the euro area will be offset by the upward impact of spillovers from the US. Moreover, we expect eurozone short term rates to drop during the course of this year on the back of ECB repricing.

Indeed, we judge that the ECB will tighten policy only modestly given our forecast for growth and inflation. We expect that inflation will remain elevated for a while, but that wage growth will remain relatively subdued. The resulting fall in real wages is likely to weigh heavily on consumer spending, and economic growth is likely to come in below ECB expectations. Furthermore, any adjustments to the deposit rate will take place after the end of the net asset purchases, which we expect to end in September given the ECB’s hawkish tilt. Consequently, we have pencilled in a 10bp rate hike in December 2022 and another one in March 2023. After that, we expect rate hikes to be put on ice. Meanwhile, more than 50bp of policy rate hikes are priced in by financial markets for this year (see graph below), which looks overdone to us against this background. Once financial markets start to price out multiple rate hikes, we expect short term rates to move lower, with the 2y Bund yield dropping to -0.40bp at the end of 2022.

The market is pricing in an aggressive rate hike cycle in the euro area

Source: ABN AMRO Group Economics, Bloomberg

We expect the 2s10s on the Bund curve to bull steepen by about 40bp – Overall, a correction in expectations of ECB rate hikes should reduce rates at the short end, while longer term rates are likely to remain more resilient given that markets should continue to price in a normalisation of monetary policy over the medium term, while there will also be an upward pull from the US. Consequently, we expect the 2s10s on the Bund curve to bull steepen by about 40bp from current levels. (Jolien van den Ende, Aline Schuiling, Nick Kounis)