Carbon Market Strategist - The downward trend is here to stay

EUA prices keep their downward trend and hit pre-(energy) crisis levels. The decrease in EUA prices is driven by structurally lower demand for power generation as more renewables are deployed and efficiency measures seem to be sustained. Recovery in prices in the short run is unlikely, with the next MSR decision – which could potentially change the picture – not until May.

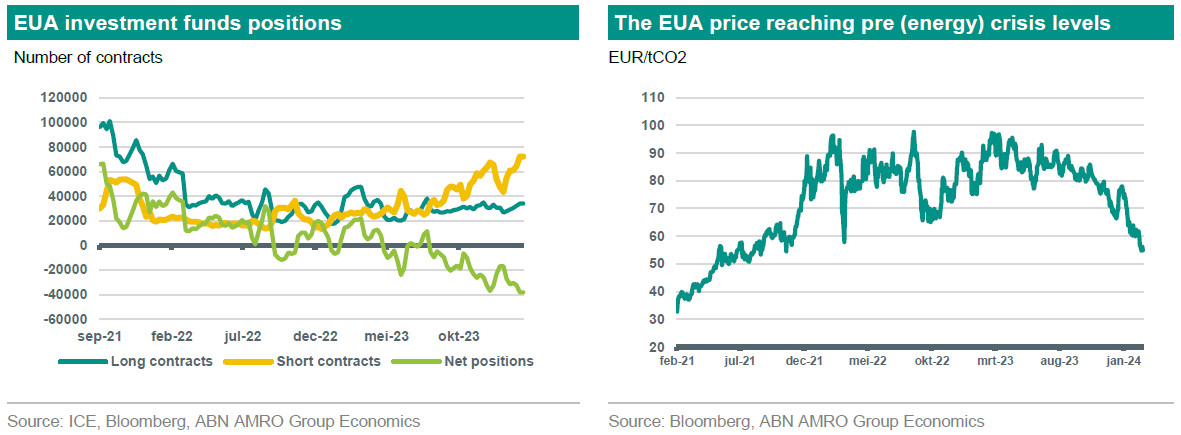

EUA prices have stayed on a downward trend during the month of February. In a new development, the market reached 53.5 EUR/tCO2 level. Although the market has not seen such levels since October 2021 (see figure below), the current levels should not be surprising as this trend has been driven by multiple factors, some of which are structural and call for action by the Market Stability Reserve in May.

If we look at the graph below on the right, we see that the EUA price was around the current levels before the energy crisis which started in 2022. The energy crisis in Europe was mainly visible in soaring gas prices that induced a shift to coal for power generation, which has higher emission intensity than gas fired power plants, driving the demand for allowances upwards.

At the same time, the crisis drove other structural (fundamental) changes in the EUA demand side. One of which is that the energy crisis have delivered a strong incentive for renewable investments both for consumers and utilities alike, increasing the share of renewables in the power mix, while that of coal and gas decreases. The high gas prices and electricity prices made the business case for these investments more and more into the money territory. The impact of the energy crisis on the transition in the power sector was unprecedented and outpaced any investment levels that could have been motivated by the allowance price alone.

Similarly, the energy crisis have encouraged energy saving and efficiency measures by both consumers and producers. These measures seems to be more sustainable than previously anticipated, reducing demand for fossil fuels for power and industrial production.

Currently, European gas prices have also dropped to much lower levels than the same period of last year, driven mainly by the mild whether we have witnessed this Winter, along with the ample storage levels, and the increase in LNG importing capacity that allowed for a diversification of suppliers in LNG markets.

The low gas prices have the reverse impact explained above in power markets. It basically induce a shift from coal to gas for power generation, and thus lower demand for allowances.

Another factor affecting the demand side, but is less fundamental and more related to the business cycle, is the weakness in economic activity due to rise in interest rates in Europe and sluggish global economic growth. Lower aggregate demand means lower industrial output, lower emission levels, and lower demand for allowances. Industrial demand for allowances is expected to remain low for the coming months until the economy picks up real momentum, which is likely towards the end of the year.

To sum up, the high demand for EUAs in the past two years has been mainly driven by the energy crisis. Now that the energy crisis is behind us, along with the fundamental changes in the energy mix in Europe that took place in the meanwhile, demand for EUAs has decrease fundamentally in the covered sectors. In other words, the speed of the transition from the covered sectors has been faster than anticipated. That is, the speed of the decrease in allowances demand outpaced that of supply, even with the EU-ETS reforms that were made under “fit-for-55” and RepowerEU packages.

From the supply side in 2024, the supply of allowances is going to be decreased by the annual linear reduction factor of 4.2%. However, such a decrease is going to largely offset by the continuation the frontloading of allowances under the REpowerEU package in 2024, along with additional allowances that are expected to be put in the market as a result of the extension of EU-ETS to the shipping sector.

Taking both demand and supply factors into account, we conclude that there is an oversupply in the EUA market. This is also reflected in the rise in the number of short positions by investment funds as shown in the left hand chart in the figure above.

The EU-ETS market has a Market Stability Reserve (MSR) which was established in January 2019 with its main objective being to balance the supply and demand of allowances in the long term, which should in turn increase the resilience of EU-ETS to future shocks. By 15th of May every year the commission announces the number of allowances in circulation, which in turn determines whether there will be any additions or withdraws from the reserve based on a predetermined threshold. As of 2023, allowances held in the MSR above the previous year’s auction volumes will be invalid.

Outlook

As a main driver for EUA’s demand, gas prices are not expected to pick up any time soon following the forecast of mild temperatures in the remaining Winter months, the continuation of weak economic growth, and the ample storage levels. Furthermore, any cuts in interest rates that could boost aggregate demand (in consequence, industrial demand and allowances demand) are widely expected to take place starting in June, with the economy not picking up real momentum until towards the end of the year. Also, any correction by the MSR mechanism will only be announced by mid-May. Therefore, our outlook for the market is to keep trending downward during March and April and the EUA price is to average around 48 EUR/tCO2 during this period.