ECB suggests more hikes to come

The ECB raised interest rates by 25bp at the June Governing Council meeting as was widely expected. Its communication and forecasts suggested that there will likely be more rate hikes to come.

Indeed, we now expect the ECB to hike its deposit rate twice further, by an additional 50bp (previously 25bp) taking it to 2.75% at year end (previously: 2.5%). We expect a 25bp increase in Q3 (with September seeming more likely than July at this stage) and a further 25bp hike in Q4.

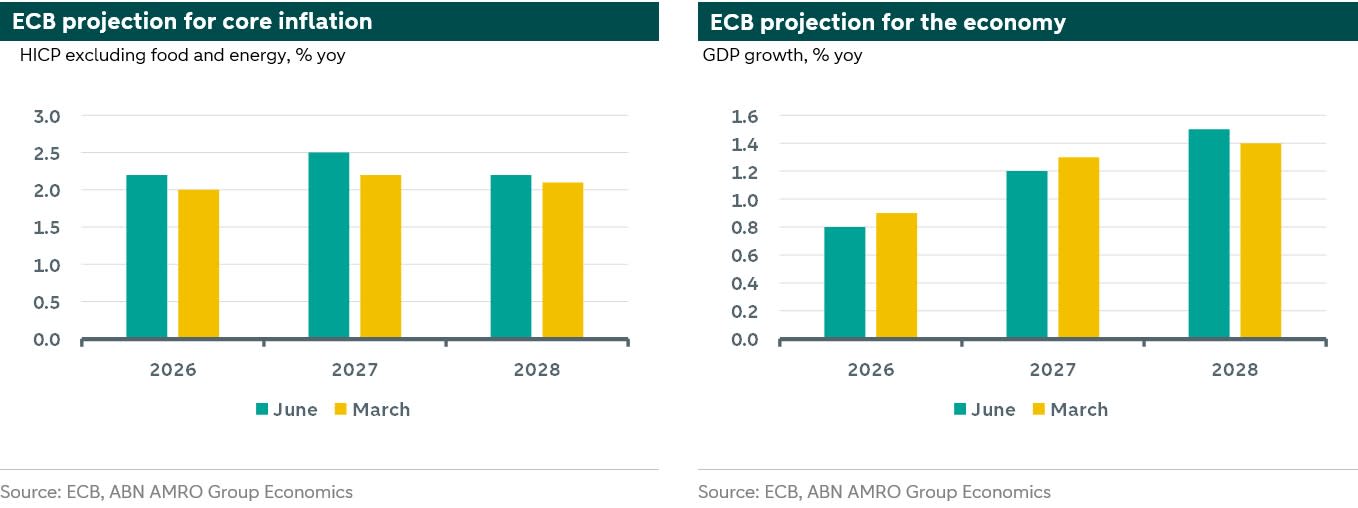

The ECB raised not only its headline inflation projections, but it also raised its core inflation numbers, in line with its view that ‘indicators of underlying inflation have already been driven higher by the energy shock’. Indeed, core inflation remains above 2% through the whole horizon that runs to the end of 2028. Crucially, its June inflation forecasts is predicated on somewhat more than three hikes (including the June move) suggesting that inflation would be even higher if it does not take further action

Indeed, the ECB continues to see the risks to inflation as being to the upside. It noted that ‘if energy prices were to rise by more and for longer than currently expected, euro area inflation would increase further. This could be reinforced and become more persistent if higher energy prices were to spill over by more than expected to other prices and to wages.’

The overall tone of the press conference was hawkish. President Christine Lagarde seemed to go out of her way to dismiss the idea that this was an insurance hike. This also suggests that there is more monetary tightening on the cards, as insurance moves are often associated with being isolated or one-off changes.

As well as its base case, the ECB published alternative more favourable and more negative scenarios for energy markets, and it noted that ‘the decision to raise rates is robust across a range of scenarios mapping out how the shock might evolve and affect the medium-term outlook for the euro area’.

President Lagarde also played down the economic growth effects of the energy shock saying that ‘It’s not as if we are in an environment where growth is absent or under significant threat’. Indeed, its base case sees economic growth continuing at a moderate pace this year, before firming further out in the horizon. This again confirms that the Governing Council is much more concerned about the inflation impact than the growth impact of this energy shock.