ESG Economist - Europe’s path to energy security

Expanding renewable energy sources, alongside investments in grids, storage, and supply chains, creates a sustainable and affordable energy system while reducing import dependency. Despite progress, projections show a significant gap between the current trajectory and the 2030 targets, prolonging reliance on imported fossil fuels and increasing geopolitical risks. Reducing energy intensity and improving efficiency decouples economic growth from energy consumption, strengthening competitiveness and lowering exposure to volatile energy markets. The expansion of electrification, based on the expansion of renewable energy, is crucial to safeguarding the EU’s energy security. Energy efficiency, innovation and the reuse of raw materials make countries less dependent on volatile energy markets and imports. Expanding storage capacity, refining facilities, and grid infrastructure ensures stability during energy crises and supports the transition to renewables. Integration of cross-border energy systems, aligned policies, and collaborative strategies strengthen resilience and reduce dependencies on external suppliers.

Introduction

In a world shaped by geopolitical tensions, volatile energy prices and the transition to sustainable sources, energy security has become a core priority. A resilient energy system helps absorb shocks, limit disruptions and safeguard businesses and households, especially in countries highly dependent on foreign energy imports. In this note, we use a broad definition of energy security. It concerns not only the continuous availability of affordable energy, but also the resilience of the wider energy system, including critical raw materials, substitutability, efficiency and innovation. In practice, this means that accelerating the energy transition, improving economic efficiency and lowering import dependency all contribute to stronger strategic energy resilience.

With this note we assess what the EU needs to do going forward to strengthen its strategic resilience further. In our view, this primarily requires greater energy efficiency, a more diversified energy mix centred on renewables, stronger European energy infrastructure, and a more integrated power market.

Accelerating the energy transition for resilience

The energy transition has delivered more sustainable energy, and with that energy security increased. Over the medium to long term, a further improvement of energy security needs an acceleration of the energy transition, provided that the expansion of renewables is matched by investment in grids, storage and strategic supply chains. The outcome of both transformations is a resilient, sustainable and affordable energy system.

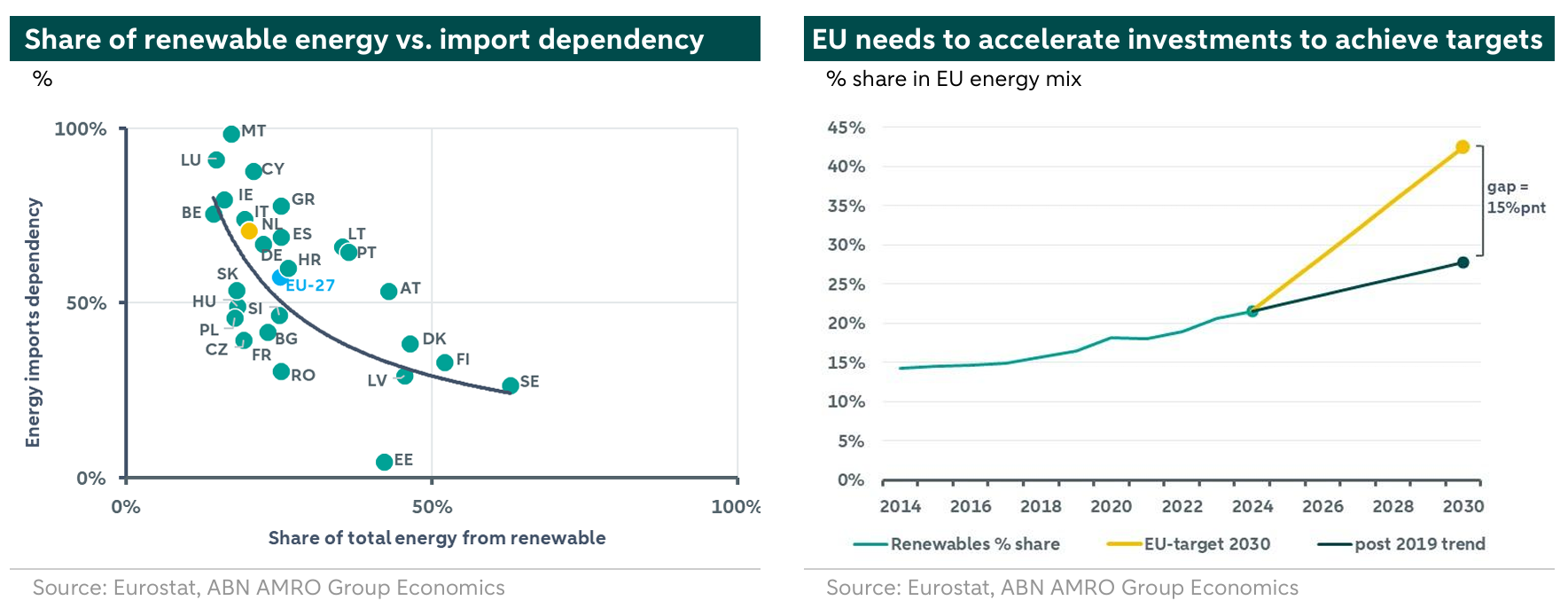

A higher share of renewable energy in the total energy mix, leads ultimately to a lower energy import dependency. This is shown in the left-hand figure below, where we have plotted all EU. However, because solar and wind are not continuously available throughout the year, many European countries are likely to require dispatchable back-up capacity for some time to guarantee security of supply, although the composition of that back-up can evolve over time. Some EU countries have proactive policies aimed at accelerating renewables and simplifying regulation for wind and solar projects going forward.

The share of renewable energy in electricity generation in the EU-27 has risen sharply, mainly at the expense of fossil fuel use. Whereas renewable energy accounted for around 22% of electricity generation in 2010, this had increased to almost 50% by 2025. And going forward, the generation of electricity from renewable energy sources will steadily increase in the EU-27, given the vast investments in renewables. But despite the further increase in renewable investments, the EU-targets on renewables will unlikely be met.

The EU has committed to achieving at least a 42.5% share of renewable energy in its overall energy mix by 2030, with aspirations to increase this to 45%. This target was established as part of the revised Renewable Energy Directive (RED III), adopted in late 2023. While renewable energy accounted for 24% of the EU's energy mix in 2024, projections based on the 2019-2025 trend indicate this share will only reach 28%—leaving a substantial 15%-point gap compared to the 2030 target. If these gaps persist, Europe’s exposure to imported fossil fuels will remain higher for longer, prolonging both geopolitical vulnerability and price risk.

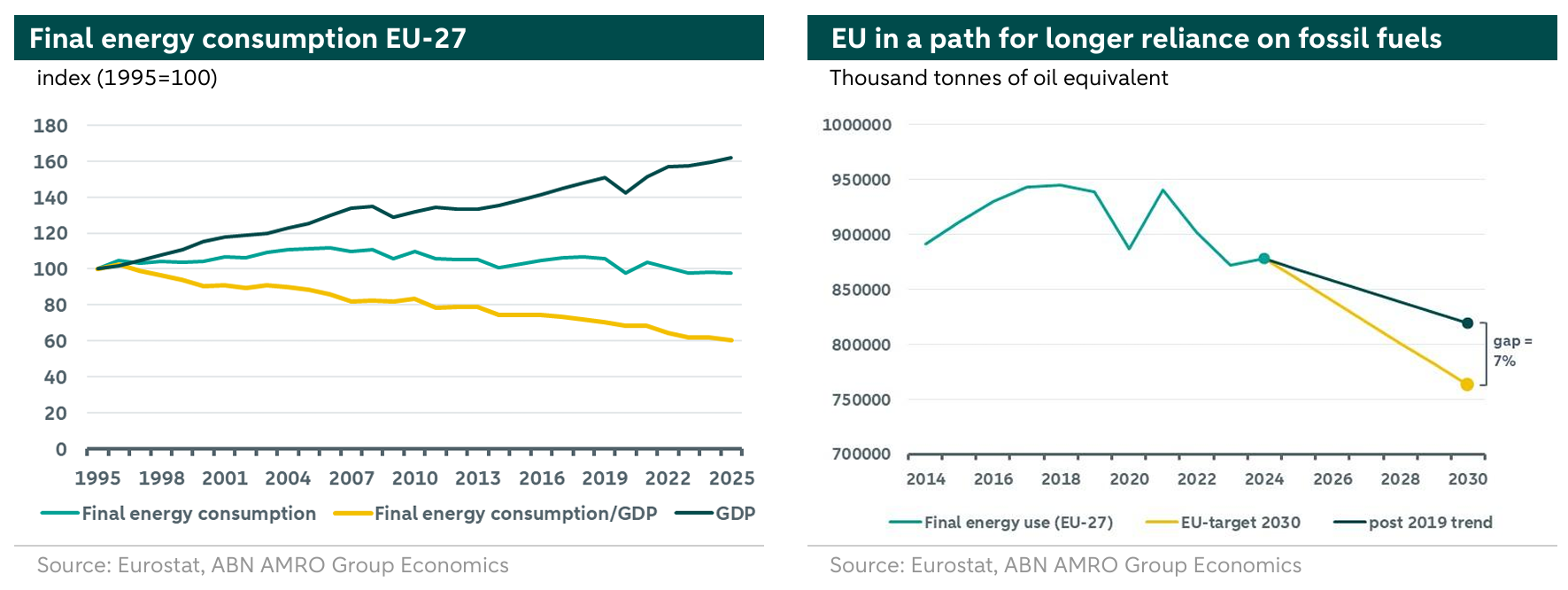

What also helped in improving energy security is the increase of economic efficiency. An increase in energy efficiency reduces the cost per unit of output and thereby increases economic efficiency. This lowers energy demand. The trend in energy efficiency can be tracked by the trend in final energy consumption. From 2006 through 2025, total final energy consumption in the EU-27 dropped by 13%. With GDP increasing over the same period, energy intensity (energy consumption per GDP) fell further. Since 1995, energy intensity has declined by an average of 1.3% per year.

Targeted and binding EU policy helps make future growth structurally less energy intensive. The success of this policy is evident. The EU economy has demonstrated that growth and energy consumption can increasingly be decoupled. More energy efficiency, innovation, but also the recycling and reuse of raw materials not only strengthen competitiveness but also make countries less dependent on volatile energy markets and imports. At the same time, more economic efficiency and innovation remain important components for safeguarding energy security over the longer term.

The European Union's binding Energy Efficiency Directive aims to reduce final energy consumption by 11.7% by 2030, compared to 2020 projections. This corresponds to an absolute ceiling of 763 million tonnes of oil equivalent (Mtoe) for final energy use. However, as shown in the left chart below, if the 2019-2025 trend continues, the EU is likely to fall short of this goal by 7%.

Overall, the EU has made significant progress in strengthening energy security. Renewable deployment and electrification have reduced long-term reliance on fossil fuels, while greater energy and resource efficiency have helped decouple economic growth from energy consumption. These gains improve competitiveness and make economies more resilient to energy shocks. However, Europe remains vulnerable from an import-dependency perspective. Although it has reduced dependence on Russian energy, it has largely replaced one set of external suppliers with another. True energy security therefore requires not only diversified imports, but a deeper shift towards locally produced renewable energy and lower exposure to geopolitical risk.

What does the EU need to do to further improve strategic resilience?

To achieve true energy independence, Europe would need to shift from reactive crisis management to a unified approach that treats energy sovereignty as a key part of its overall security, not just an economic issue. The EU should focus on reducing reliance on fossil fuels while speeding up the energy transition. Because European energy systems are increasingly interconnected, national policy choices have continent-wide consequences. Missing renewable energy targets or delaying cross-border energy projects weakens collective security. To establish lasting independence, Europe should implement a unified energy strategy that combines smart infrastructure planning with clear and enforceable policies.

Strengthening resilience to fossil fuel dependence

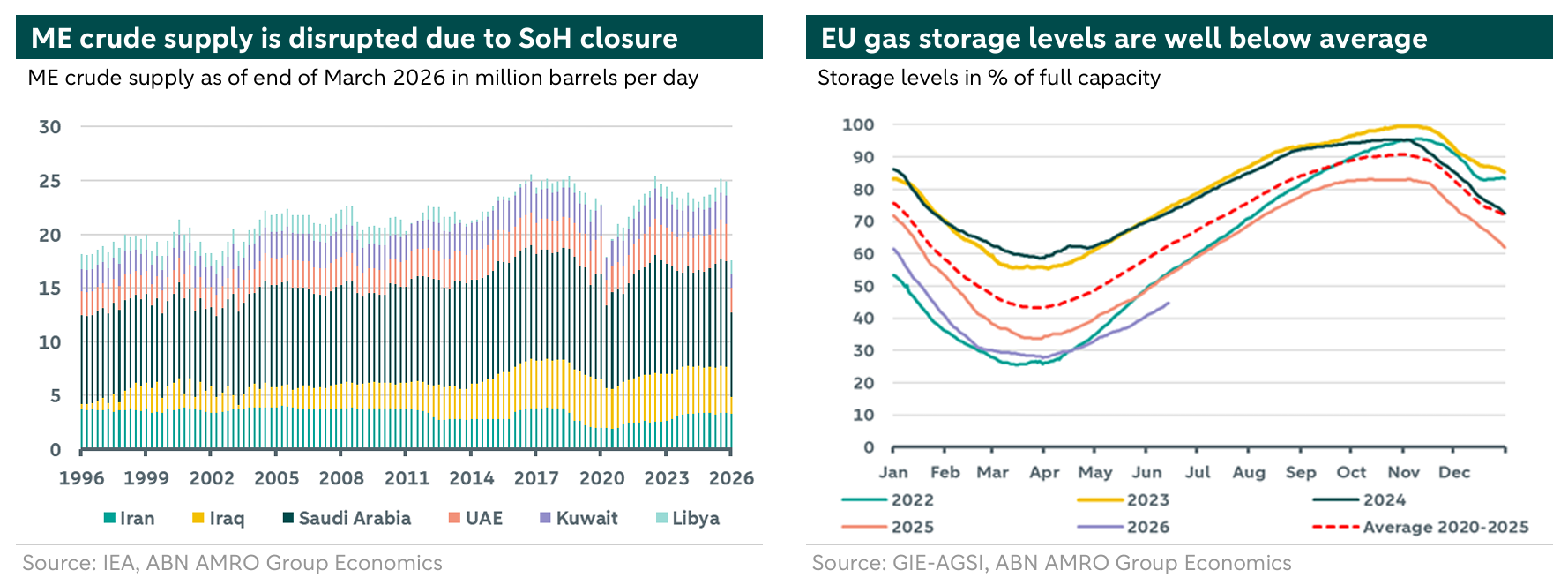

The cost of delayed progress is already visible. Falling short of its energy objectives would extend Europe’s reliance on fossil fuels and leave it more exposed to market shocks. The ongoing Strait of Hormuz disruption, for example, has already led to billions in additional energy costs for the EU within weeks. In times of a crisis, stockpiling fossil fuels can only be a short-term solution but given the foreseen extended reliance on fossil fuels in Europe, increasing European stockpiles becomes a strategic choice that provides a stronger buffer for shocks in an increasingly fragmented world.

The crisis exposed vulnerabilities in Europe’s seasonal energy storage. After a harsh winter, EU natural gas reserves dropped to 31 bcm, the lowest post-winter level since 2018, as illustrated in the right chart below. While the EU has 110 bcm (1131 TWh) of theoretical storage capacity, the loss of Qatari LNG flows has increased demand for spot LNG imports, requiring up to 56 bcm to ensure stability in the coming winter. Securing these volumes becomes an increasingly challenging task given the prolonged tightness in the LNG market. This situation underscores the urgent need for Europe to enhance its energy storage infrastructure and diversify its supply sources. Without significant improvements in storage capacity and more reliable transitional supply arrangements, the EU remains vulnerable to market fluctuations and supply disruptions.

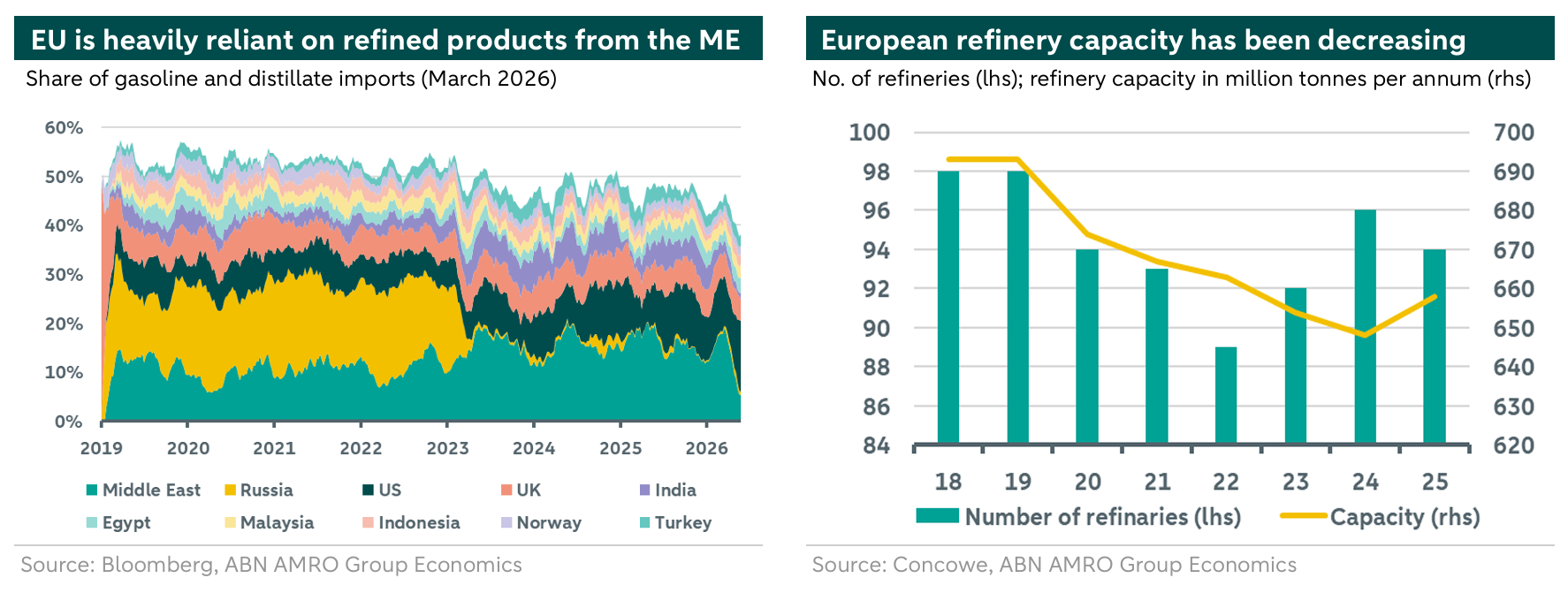

Furthermore, the crisis highlighted Europe’s deficit in middle distillates like diesel and jet fuel. With imports of Russian refined products reduced from 27% to under 2%, Europe now relies heavily on imports from the Middle East and Asia. Rerouting these supplies around Africa has caused regional shortages. Meanwhile, EU refineries have been working to optimize operations, processing heavier crude grades from West Africa and the US to maximize middle distillate production. These efforts are critical to maintaining industrial logistics while planning for the eventual phase-out of fossil fuels. Europe’s middle distillate deficit highlights the need to reduce reliance on external suppliers and boost refining capacity.

To strengthen Europe’s resilience during the transition, it is crucial to expand seasonal energy storage and foster partnerships with reliable suppliers to ensure stability. It is also essential to move from voluntary storage goals to mandatory requirements. For instance, France’s "Public Service Obligation," which requires energy suppliers to store 50% of historical winter consumption for residential use, provides a model that should be implemented across the EU. Relying solely on market forces to manage storage creates systemic risks that could leave Europe vulnerable during energy crises.

In addition to storage reforms, investing in refinery upgrades is crucial for industrial stability and the transition to cleaner energy. Europe may need to preserve or selectively upgrade critical refining capacity to reduce short-term dependence on external suppliers during times of crisis. Additionally, existing refineries should maintain strategic reserves of middle distillates, such as diesel and jet fuel, to minimize reliance on imports while transitioning to cleaner energy sources. Operational mandates should also be introduced to ensure industries have access to adequate supplies during disruptions.

The EU is also taking steps to advance storage systems for alternative fuels like hydrogen and Sustainable Aviation Fuel (SAF). Accelerated planning under the European Hydrogen Bank is driving the development of underground salt caverns and depleted fields for hydrogen storage. Meanwhile, transport hubs are upgrading infrastructure to meet ReFuelEU Aviation mandates, aiming for a 2% SAF integration target. These initiatives are key to diversifying Europe’s energy mix and reducing its dependence on fossil fuels over the long term.

Under current policies, resilience to fossil fuel dependence will likely take at least 5–10 years to develop, as infrastructure upgrades, regulatory harmonization, and increased refinery capacity require time and investment. However, under more ambitious scenarios, such as accelerated adoption of mandatory storage targets and expanded refinery capacity, resilience could be significantly strengthened within 3–5 years. These outcomes depend on the EU’s willingness to implement systemic reforms and allocate funding to energy security measures.

At the same time, several barriers stand in the way of building resilience quickly. First, the financial cost of expanding storage capacity and refinery operations is substantial, requiring coordinated investment from both public and private sectors. Second, geopolitical tensions and market volatility continue to challenge stable access to fossil fuel supplies. Third, regulatory fragmentation across member states slows the implementation of unified policies and creates inefficiencies in crisis response. Finally, the transition to cleaner energy sources adds complexity, as the EU should balance investments in fossil fuel resilience with its broader decarbonization goals.

The long-term solution to Europe’s energy security challenge lies in accelerating the energy transition through expanded renewable capacity, stronger grid infrastructure, alternative sustainable fuels and a more integrated European power market.

The central role of hydrogen and alternative sustainable fuels

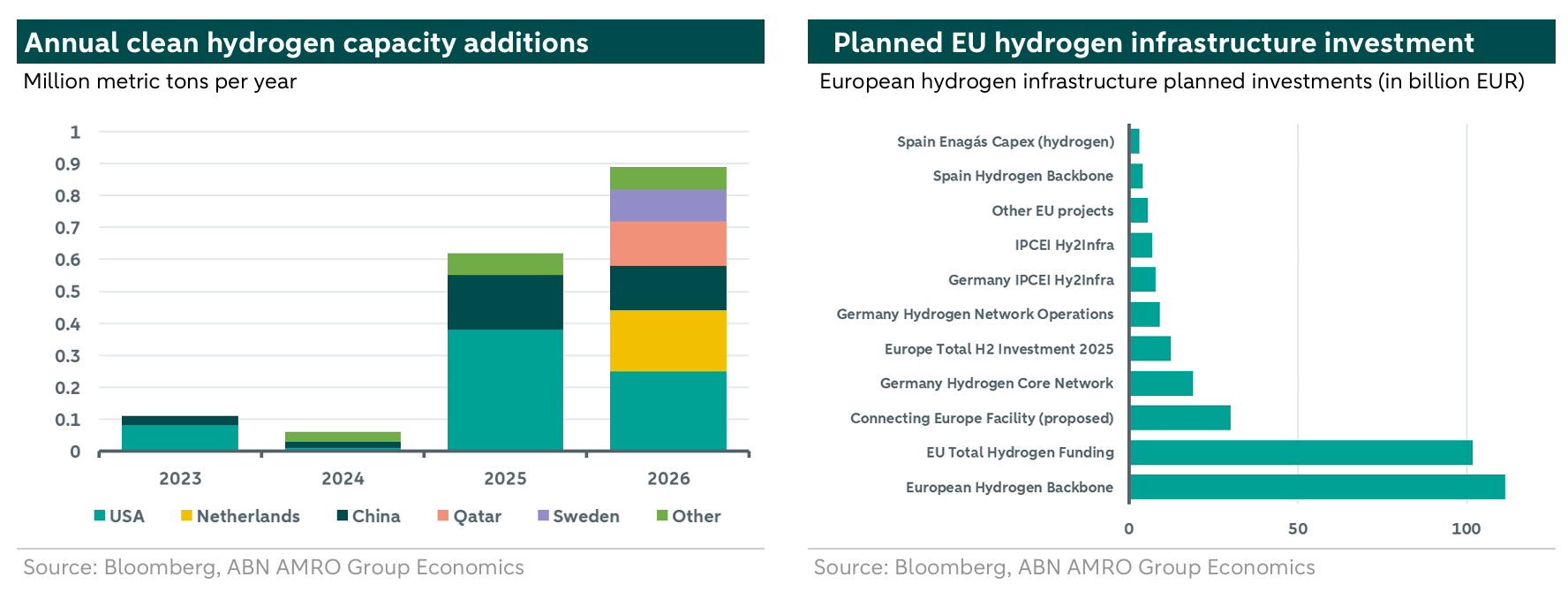

The EU is positioning hydrogen as a key pillar of its energy transition strategy to enhance energy security and achieve its "Fit for 55" and net-zero emission goals. Green hydrogen, produced from renewable energy, is critical for decarbonizing industries like steelmaking, oil refining, and chemical manufacturing, as well as transport sectors such as aviation and shipping, where batteries are impractical for long-range travel. Hydrogen also strengthens energy security by enabling long-term storage and balancing the power grid during seasonal shortages. You can read more about the role of hydrogen in the energy transition in our earlier publications here and here.

Recognizing its strategic importance, the EU has committed EUR110.6 billion to hydrogen-related support, while planned hydrogen infrastructure investment across Europe exceeds EUR311 billion, according to the project pipeline shown below. This includes grants for production, electrolyzers, pipelines, and storage. Major national initiatives, such as Germany's Hydrogen Core Network and Spain's H2Med Corridor, complement cross-border collaborations like the Nordic-Baltic Corridor to expand hydrogen infrastructure. However, renewable hydrogen production remains far below targets, with output at just 0.06 Mtpa in 2026 compared to the regulated demand of 2.2–2.8 Mtpa by 2030.

Several barriers hinder rapid adoption of hydrogen. High production costs limited green electricity availability, and reliance on fossil-based hydrogen slow progress. Regulatory inconsistencies across member states, inflation, and rising energy prices deter investment and have led to project cancellations, such as Statkraft halting new initiatives. Additionally, delays in infrastructure development and fragmented funding mechanisms further impede scaling efforts. Overcoming these challenges will require cohesive policies, accelerated investments, and enhanced collaboration to ensure hydrogen’s role as a cornerstone of the EU’s energy security and decarbonization goals.

That is why the EU is expediting regulatory reviews and policy updates to advance its green hydrogen strategy in response to energy security concerns, industry demands, and the need for streamlined adoption. The European Commission plans to revise Renewable Fuels of Non-Biological Origin (RFNBO) rules by June 2026—two years ahead of schedule—to introduce more flexible criteria for renewable electricity sourcing, aiming to reduce production costs and improve project feasibility. While these revisions may enhance affordability, critics caution that such changes could undermine regulatory stability and investor confidence. Progress on the Hydrogen and Gas Decarbonisation Package continues, with national transpositions expected by August 2026 and European Network of Network Operators for Hydrogen (ENNOH) coordinating cross-border infrastructure planning. However, delays in member states’ implementation of RED III rules and sluggish infrastructure development threaten the EU’s ability to achieve its ambitious targets for renewable hydrogen adoption by 2030.

Advancing grid infrastructure and battery storage systems

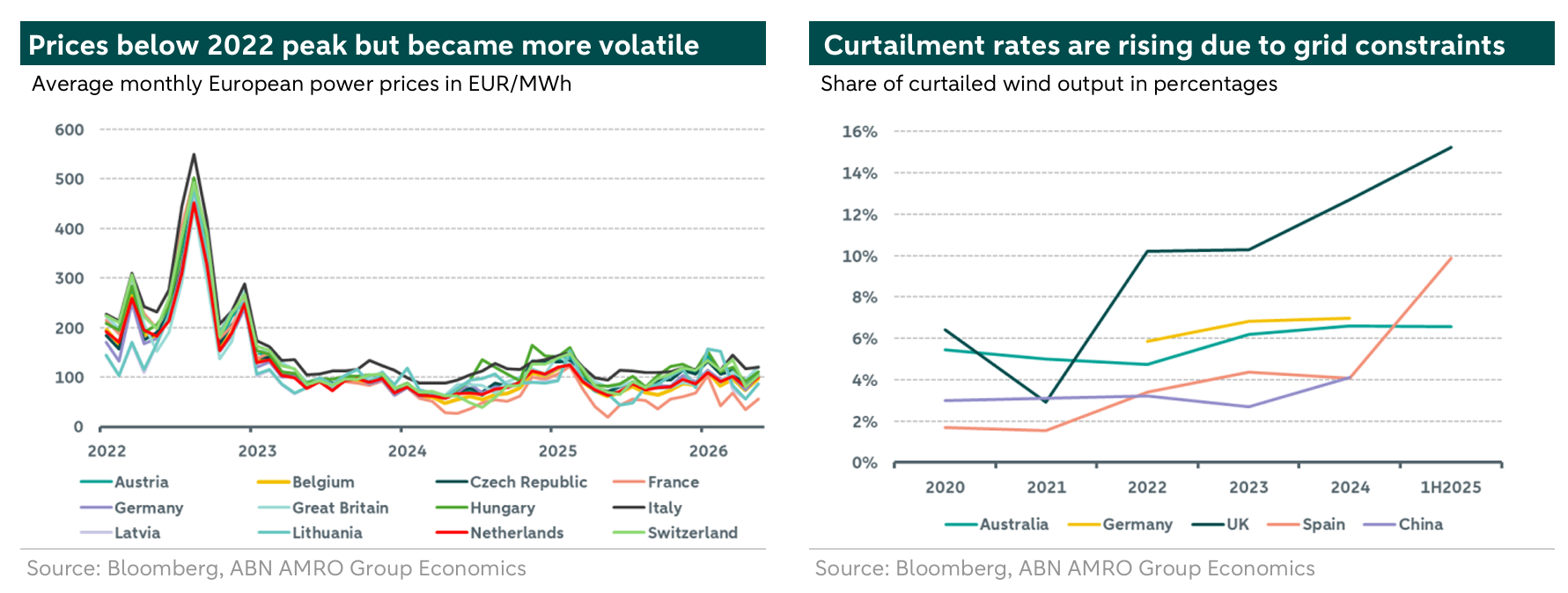

Through the REPowerEU package, the EU has added 76.8 GW of renewable energy generation between 2022 and 2024, bringing the EU’s total renewable fleet to over 406 GW, enabling annual savings equivalent to 15.8 billion cubic meters (bcm) of natural gas. However, increasing renewable energy generation is ineffective without the infrastructure to absorb and distribute it. Limited grid capacity across different European countries has been a major bottleneck which slows down the energy transition. Intermittent solar and wind production without sufficient storage has caused high curtailment rates and negative pricing hours, creating financial and operational risks for developers.

To address this, the EU has initiated the European Commission’s Grid Package, which funds over 10,000 kilometres of new cross-border transmission lines. Additionally, utility-scale Battery Energy Storage Systems (BESS) are being deployed to provide 11 GW of storage capacity. These systems help stabilize grid fluctuations and reduce reliance on gas-fired power plants during peak demand periods, thereby strengthening the EU’s resilience to fossil fuel market shocks.

However, achieving a fully resilient and advanced grid under current policies could take 10 to 15 years, though accelerated measures like increased funding, streamlined permitting, and enhanced cross-border cooperation might reduce this to 7 to 10 years. Nevertheless, practically, several barriers impede such rapid progress: substantial financial investments face competition from other EU priorities, permitting and regulatory delays slow cross-border projects due to fragmented policies and legal frameworks, and technical challenges arise from the need for sophisticated grid management tools and forecasting systems still under development.

Additionally, discrepancies in regional grid capacities and energy policies create structural bottlenecks, disrupting cross-border electricity flows and weakening EU energy resilience. These barriers cannot be solved by infrastructure investment alone. They also require deeper market integration, which is why the Single European Power Market is central to Europe’s energy security strategy.

Strengthening the single European power market

A more integrated Single European Power Market is vital for strengthening Europe’s energy security and resilience. By creating a unified system, Europe can effectively respond to localized energy crises and balance supply and demand across the continent. Recent progress, such as the agreement with Switzerland to harmonize electricity flows, has demonstrated the benefits of collaboration. This interconnected network serves 460 million consumers and uses advanced tools like algorithmic day-ahead market coupling to redistribute surplus renewable energy to areas experiencing shortages. Such mechanisms ensure efficient energy use while minimizing disruptions and reducing dependence on fossil fuels.

To fully realize the potential of the Single European Power Market, member states should treat it as a cohesive system rather than a collection of national markets. Protectionist measures, such as cutting cross-border interconnectors to stabilize local prices, undermine mutual trust and weaken the overall effectiveness of the market. Instead, Europe should prioritize collaboration and solidarity, ensuring that resources are shared equitably and that the market functions as a unified entity. While these changes will require significant investments and collective action, they are essential to building a system that can withstand supply chain disruptions and geopolitical challenges. As mentioned above, infrastructure expansion, such as new cross-border interconnectors and improved energy storage systems, is crucial to support the higher volumes of electricity that will flow across borders. Member states also need to align their energy policies and regulations to eliminate barriers and ensure smooth operation. Creating this unified market could take up to a decade, but its benefits for Europe’s energy security and sustainability will be profound.

Conclusion

Our analysis shows that the EU has made meaningful progress in strengthening energy security through electrification, renewable deployment and greater efficiency. These developments have improved resilience and reduced some of the vulnerabilities exposed by the 2022 energy crisis.

Yet Europe remains heavily dependent on external energy and raw material flows. Diversification has reduced reliance on Russia, but it has not removed the structural vulnerability created by imported fossil fuels.

The strategic response must therefore combine short-term resilience with long-term transformation. In the near term, Europe needs stronger storage, critical fuel buffers, grid readiness and coordinated contingency planning. Over the longer term, it needs faster renewable deployment, deeper electrification, stronger infrastructure, a more integrated power market and sustained political coordination across Member States. Energy security will ultimately depend not only on where Europe imports energy from, but on how quickly it can reduce the need for those imports altogether.