Euro inflation surge has further to run

According to the flash estimate HICP inflation in the eurozone increased to 9.1% in August, up from 8.9% in July. Core inflation increased to 4.3%, up from 4.0% in July. We think that the rise in inflation has not yet ended and that the peak could be reached in September-October.

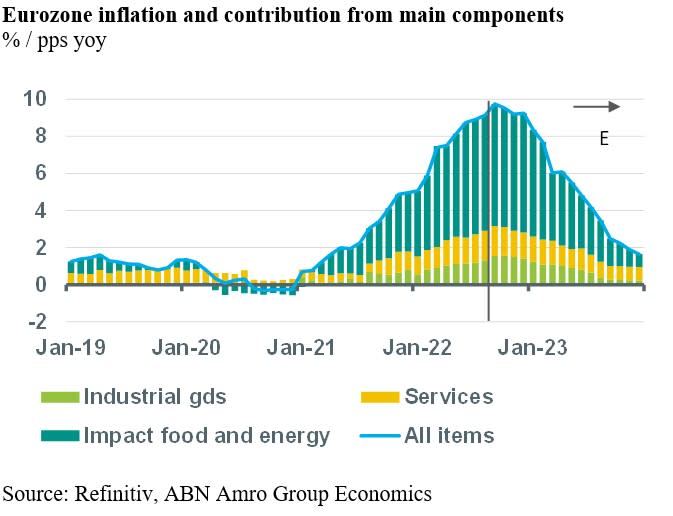

Eurozone inflation continues to rise - peak not yet reached

According to the flash estimate HICP inflation in the eurozone increased to 9.1% in August, up from 8.9% in July. Core inflation increased to 4.3%, up from 4.0% in July. The break-down in the main components reveals that on the one hand the recent decline in oil and food commodity prices has resulted in declines in the energy and food components of the HICP. However, on the other hand, surging gas prices and the filtering through of past jumps in food and energy prices into services and manufactured goods prices has had a upward impact on inflation. Indeed, energy price inflation declined to 38.3% in August, down from 39.6% in July and unprocessed food price inflation fell to 10.9%, down from 11.1% in July, whereas processed food price inflation increased to 10.5%, up from 9.4% in July. Also, the inflation rate of non-energy industrial goods increased to 5.0%, up from 4.5% in July and the inflation rate of services increased to 3.8%, up from 3.7% in July. The idea that falling oil prices and rising gas (and electricity) prices had an opposite impact on inflation in August, was also illustrated by the more detailed inflation reports of the main German states. They showed that the inflation rate of household energy increased sharply in August, whereas the inflation rate of fuel and transportation energy dropped lower.

Looking forward, we think that the rise in inflation has not yet ended and that the peak could be reached in September-October. The historical pattern in energy inflation shows that changes in oil prices tend to have a relatively large and immediate impact on energy inflation, whereas changes in gas prices have a more moderate but much longer impact, which could take almost a full year to work its way through into inflation. Therefore, the impact of the recent surge in gas prices will continue to fuel inflation during the rest of this year. Also, in September there will be a one-off jump in the inflation rate of transport services as the temporary cheap public transport ticket that was introduced in Germany in June expired on 31 August. Moreover, past jumps in energy prices and food prices tend to filter through into manufactured goods and services prices (for instance, transport by air, sea and road, hotels, restaurants, catering) but also often with a delay of a few months. This means that core inflation will probably also rise somewhat further in the next few months.

This impact of high energy and food prices filtering through into core inflation is different from the second round longer-term effect that would result from high inflation leading to wage growth that is well above labour productivity growth. We think that this second effect will be more moderate as the economic outlook and the outlook for employment growth is deteriorating rapidly. Indeed, we think the economy has entered a recession and that the unemployment rate will move higher as from the final months of this year onwards, which will limit wage growth. All in all, we expect inflation to remain elevated throughout this year and to start gradually declining in 2023. Although the uncertainties related to energy and other commodity prices remains very high, based on our current assumptions, the inflation rate is expected to return to around the ECB’s 2% target by the end of next year.