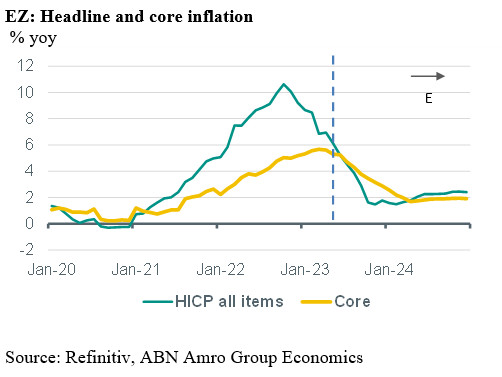

Eurozone core inflation edges lower

Eurozone headline HICP inflation dropped to 6.1% in May, down from 7.0% in April. The fall in inflation was mainly due to drops in the inflation rates of energy (to -1.7%, down from 2.4%) and food, alcohol and tobacco (to 12.5% from 13.5%), which was in line with the expectations and had been pre-signalled by declines in commodity and wholesale prices of energy and food. The drop in food and energy inflation has further to go in the coming months. However, besides the drop in energy and food inflation, core inflation also fell noticeably, to 5.3% from 5.6%. The fall in core inflation was stronger than expected.

Drop in headline inflation augmented by falling core rate

Several factors currently are having an impact on core inflation. As we have mentioned earlier, the pass-through of past rises in energy prices into the prices of goods and services has eased in the past few months, which is lowering the inflation rates of energy-intensive goods and services. On top of that, the inflation rate of non-energy intensive industrial goods is also declining, probably due to a combination of global supply chain bottlenecks dissipating and eurozone goods consumption slowing down. Indeed, total non-energy industrial goods price inflation declined to 5.8% in May from 6.2% in April. It seems that the only part of inflation that is yet to be in a clear down-trend is non-energy intensive services inflation. Although total services inflation declined to 5.0% in May from 5.2% in April, the more detailed inflation data from some individual eurozone member states showed that the inflation rate of services such as leisure and entertainment, maintenance and repair and communication increased in May, probably supported by high wage growth and still elevated demand for these services.

Looking ahead, we expect the inflation rate of non-energy intensive services to remain elevated for a while, but to start falling later in the year as well, as the expected slowdown in economic growth should result in deteriorating labour market conditions and slower wage growth. All in all, we expect both core inflation and the headline rate to fall considerably in the coming month, but core inflation should be more sticky than the headline. Headline inflation is expected to temporarily drop below the ECB’s target of 2% in the final months of this year, whereas core inflation is expected to be around 3% by then.