Eurozone - Core inflation has probably peaked

Eurozone GDP grew slightly in 2023Q1, but moderate contractions in GDP seem on the cards. Core inflation probably has peaked, with the pass through of high energy prices easing. We expect the ECB to hike rates further in the short-term, but the first rate cut could follow already by the end of the year.

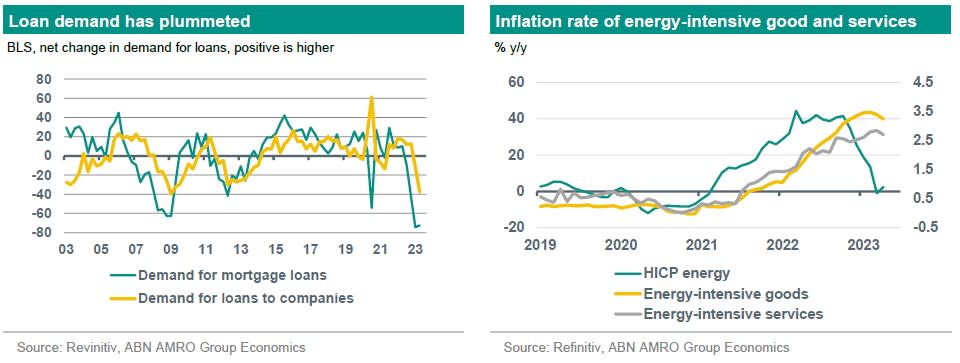

Eurozone GDP expanded by 0.1% qoq in 2023Q1, whereas we had expected a small contraction similar to the -0.1% qoq that was recorded in 2022Q4. The detailed GDP report has not yet been published, but monthly activity data and details from individual countries indicate that growth was mainly driven by services consumption and a temporary jump in construction on the back of mild winter weather. Goods consumption and investment in machinery and equipment and inventories probably contracted in Q1, while net foreign trade probably lifted growth somewhat. Looking beyond Q1, we think modest contractions in GDP are on the cards. Past interest rate hikes by the ECB have already resulted in banks tightening credit standards on all types of loans, and demand for loans has also fallen. Moreover, actual loan growth has slowed down noticeably in recent months and house prices have declined. Also, the post-pandemic rebound in certain parts of services seems to have largely run its course, and construction will likely slow after the temporary boost in Q1. Finally, industrial production and exports are expected to remain weak as the global economy loses momentum. Despite the expected modest quarterly contractions in GDP, the annual average change in GDP will probably be slightly positive (+0.2%) this year, which is higher than our previous forecast of zero growth.

Inflation edged slightly higher in April (to 7.0%, up from 6.9% in March), but core inflation declined (to 5.6% from 5.7%). Base effects due to changes in energy prices last year temporarily lifted energy inflation in April, but it should fall sharply in the coming months. Food price inflation is also expected to decline based on recent trends in commodity and wholesale prices. Finally, core inflation is also expected to fall. Indeed, our calculations show that the pass-through of the rise in energy prices into the prices of goods and services that began with a lag of about six months after the start of the War in Ukraine, is easing. The inflation rate of energy-intensive industrial goods fell by 0.2 percentage points in April, after it declined by 0.1pp in March, while that of energy-intensive services fell by 0.1pp in April after being unchanged in March. We expect a further significant easing of the energy-intensive parts of inflation in the coming months, which should reduce core inflation. Our expectation of a recession should also bring wage growth down, helping inflation to fall back to the ECB’s target over time.

As expected, the ECB raised the deposit rate by 25bp in May – a slowdown from earlier 50bp hikes. The ECB clearly signalled that its bias is towards further rate hikes. We expect two more 25bp hikes in both June and July, before a rate cut cycle begins in December and continues during 2024. Indeed, we think that as monetary policy tightening feeds through, the economy is likely to prove much weaker than the ECB currently expects in the second half of the year. As such, we expect an easing cycle to start from around the turn of the year.

This article is part of the Global Monthly of May 23