Eurozone inflation declines despite higher core rate

Eurozone inflation declined to 8.5% in February, down from 8.6% in January. Meanwhile, core inflation came in higher than expected, jumping to 5.6% in February, up from 5.3% in January. Energy inflation dropped lower again, but food and services price inflation increased. Looking forward, we continue to see both headline and core inflation falling rapidly later in the year on the back of the decline in wholesale energy and food prices as well as dissipating supply chain bottlenecks and lower aggregate demand because of tighter monetary policy.

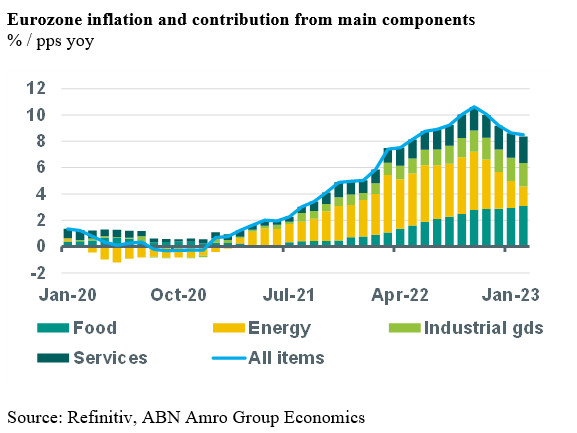

Headline inflation declines but core rises

Eurozone inflation declined to 8.5% in February, down from 8.6% in January. The decline was in contrast to what was signalled by earlier data from a number of big individual countries, which all showed a rise in headline inflation. Meanwhile, core inflation came in higher than expected, jumping to 5.6% in February, up from 5.3% in January.

The breakdown of the main components shows that non-energy industrial goods price inflation edged higher to 6.8%, up from 6.7%, but that services inflation increase more noticeably, to 4.8%, up from 4.4%. Besides core inflation, food price inflation also increased in February, up to 15.0% from 14.1%. Working in the opposite direction, energy inflation dropped to 13.7%, down from 18.9%. As a result the contribution of food prices to total inflation (2.8 percentage points) is almost twice as high as the contribution of energy inflation (1.5 percentage points) at the moment.

Looking forward, we continue to see both headline and core inflation falling rapidly later in the year on the back of the decline in wholesale energy and food prices as well as dissipating supply chain bottlenecks and lower aggregate demand because of tighter monetary policy. Indeed, the drops in oil and gas commodity prices since the summer of 2022 will result in a further drop in energy price inflation during the rest of this year. Also recent trends in food commodity prices indicate that food price inflation should decline in the coming months. Core inflation will probably be more sticky and remain more elevated in the short-term, but should also ease going forward.

Our own calculations for the impact of the rise in energy prices on the inflation rate of goods and services indicates that past rises in energy prices still are being passed on to consumers at the moment. This process could continue for a while, but should end in the second half of the year. Moreover, dissipating supply bottlenecks in industry will reduce the inflation rate of non-energy industrial goods. It seems that the only part of inflation that could actually rise somewhat further in the short term is services sector inflation, which could be pushed higher by rising wage costs on the back of the labour shortages that emerged in the sector after the pandemic. However, the economic slowdown and deteriorating overall labour market conditions are expected to reduce wage growth in the second half of this year, which should also reduce services sector inflation.