Eurozone Q2 GDP - Trade war collides with recovering domestic demand

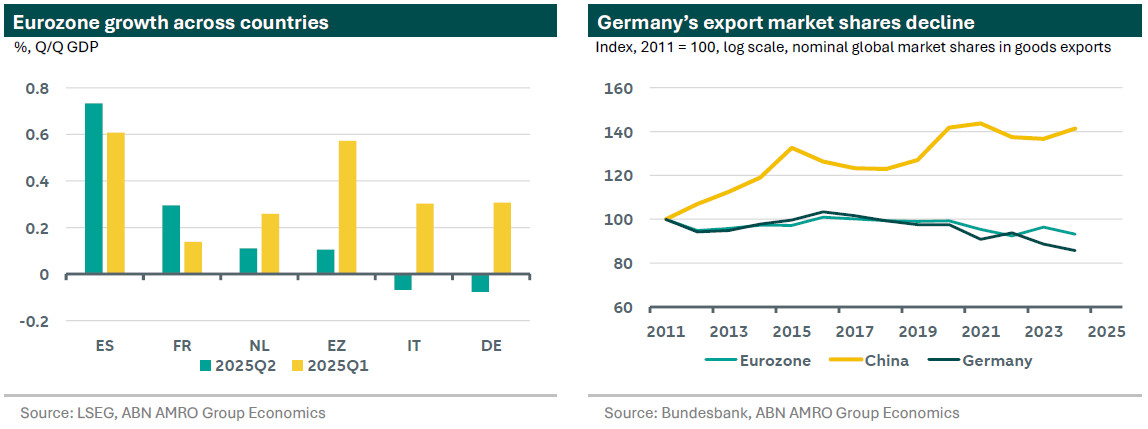

Eurozone Q2 GDP surprised to the upside at 0.1% q/q, following growth of 0.6% in Q1. The Q2 outturn was well above our forecast for a small contraction (-0.2%) and a bit above consensus (0.0%). The miss on our part was largely driven by Ireland, but France also surprised to the upside (see below).

We had expected a much bigger unwind of the massive frontloading of exports to the US that took place in Q1, but this unwind looks to be unfolding more gradually. While we do not have the full breakdown of GDP for the eurozone aggregate, piecing together details from the national GDP releases suggests that underlying domestic demand continued to recover – helped by ECB rate cuts and a slow turn in the credit cycle – but that this is being offset by a fall in exports to the US after tariffs rose in April. Still, that fall in exports is happening more slowly than expected, and there remains considerable uncertainty over how quickly the impact will materialise further over the coming quarters. Even with the recent trade deal (see here), the tariff rises we are talking about are unprecedented in modern history. Our base case sees the economy remaining weak in Q3 on the back of falling exports to the US, before the German fiscal bazooka makes a bigger splash from Q4 and moving into 2026. We will publish updated growth forecasts with our August Global Monthly in a few weeks’ time.

GDP a mixed bag across eurozone countries

Alongside Ireland, which contracted by much less than we expected (-1% q/q after a 7.4% expansion in Q1), GDP in France also surprised to the upside at 0.3% q/q compared with our forecast of 0.1%. This was due to a puzzling mix of drivers: domestic demand stagnated, while net exports subtracted from GDP, leaving the only positive contributor to be a rise in inventories, which added 0.5pp to growth after 0.7pp in Q1. We suspect that there is some mismeasurement going on in the trade side linked to the frontloading to the US ahead of tariffs, and we would not be surprised if there are significant revisions further down the line as the data becomes more complete. Elsewhere in the eurozone the incoming data was a mixed bag. Italy and Germany both saw contractions of -0.1% q/q, while Spain and Portugal continued to be in a seemingly different economic reality to the rest of the eurozone. Helped by ongoing recovery fund disbursements and solid domestic demand, both countries expanded at a well-above-trend 0.7% and 0.6% respectively.

Germany: Rising optimism about 2026 clashes with difficult near term trade reality

The German economy contracted in the second quarter of 2025 by 0.1% q/q, in line with our and consensus forecasts. Though we do not have the full breakdown yet, the press release by Destatis points towards a decline in investment, particularly in machinery and construction which contributed to the contraction in GDP, while private and public consumption expanded. The soft patch in today’s GDP reading was expected given the unwinding of the boost caused by a frontloading of US exports in Q1, tariff impact slowly materializing and general elevated uncertainty that particularly hits Germany’s export-orientated growth model.

The contraction comes at a time when optimism about the German economy was returning, albeit cautiously. Indeed, according to an S&P survey, German companies are the most optimistic about the economy since early 2022. Only last week an investment summit was held, in accordance with Chancellor Friedrich Merz, where large German companies committed to an investment drive worth €100 billion over the next 2.5 years. Here, the significant ramping up of domestic fiscal spending in defence and infrastructure over the coming years lays a floor for private sector confidence to improve and build upon. After some near term drag following from US tariffs, we see the economy picking up pace in 2026 on the back of this fiscal spending surge.

Still, even with fiscal spending improving the growth outlook, the German economy is not out of the woods yet. Alongside the drag from US tariffs, the factors causing the prolonged recession over 2023 and 2024 are still very much present. As the Bundesbank calculated, Germany’s market share in goods exports have fallen since 2017 and have been particularly weak since 2021, especially in Germany’s machinery and energy-intensive industries. High energy prices and structural factors like bureaucracy and demographics are major drags. But most importantly, China going from source of demand for German exports towards a competitor –even in home markets – has contributed to this fall in market share. Most of these factors are unlikely to dissipate soon. If anything they have intensified, with competitiveness pressures aggravated by the strong euro and of course US tariffs. The export-led growth model of Germany therefore remains challenged.

Netherlands: Shifting to a lower gear

Dutch economic growth slowed to 0.1% q/q (ABN AMRO 0.2% q/q), down from 0.3% q/q in Q1. The Dutch economy has been losing steam since 2024Q2 and growth is set to stay subdued in the near term given a difficult landscape for international trade and elevated uncertainty, as well as domestic policy uncertainty with the upcoming snap elections in October. Further out, in 2026 the outlook is more constructive as rate cuts lift activity, uncertainty likely is diminished and spillovers from German fiscal spending add to growth.

In terms of the subcomponents, government consumption and investment, in part due to rising defence investments in ships and aircraft, contributed positively to growth. In contrast, there was a negative contribution from net exports, primarily caused by rising imports, possibly to do with unwinding of frontloading effects as well as rising gas imports as it is filling season for gas storage ahead of winter. Additionally, private consumption surprisingly contracted by -0.4% q/q. While household sentiment remains negative, the fundamentals for private consumption are still solid. Government measures have boosted purchasing power, the labour market remains tight, and wage growth is outpacing inflation leading to real income rises. Despite this, households seem to prefer saving over consuming, as shown by the elevated savings rate. This is probably linked to the elevated uncertainty which is also affecting households.

Zooming out, the Dutch economy is losing steam and continues to face supply side constraints such as on labour supply and the electricity grid which reduce potential growth. The country is set for elections on the 29th of October which offer a chance for a new government to address these supply side constraints and lift potential growth. Given the expectation of a difficult formation process, 2026 will likely be well underway before a new government is installed. We expect the Dutch economy to expand by 1.6% in 2025 and 1.3% in 2026.