Eurozone - Shallow, yet prolonged recession on the cards

We have changed our base scenario for the eurozone economy and now expect a more shallow but more prolonged recession than we did before. The ECB is expected to continue to hike rates, with the deposit rate peaking at 3%. Policy rate cuts could be on the agenda before the end of the year.

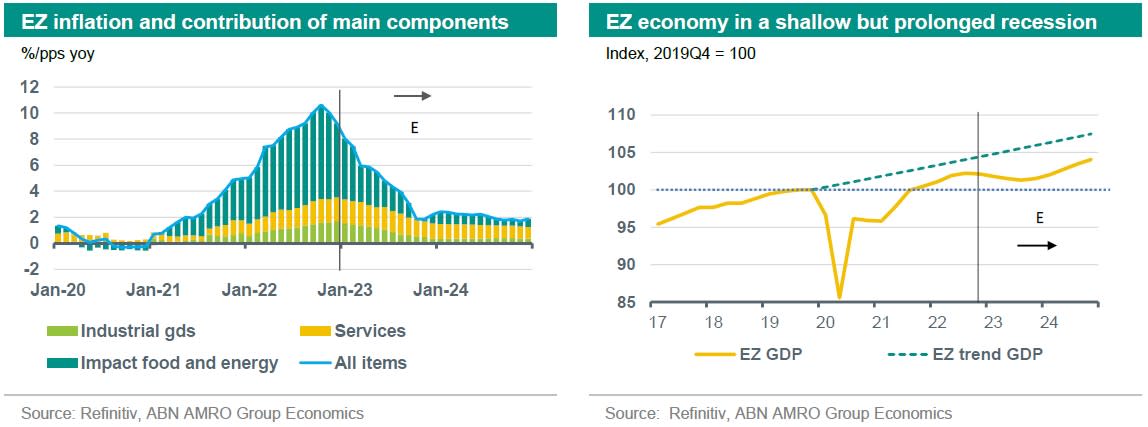

We have changed our base scenario for the eurozone economy. We have revised upward our forecasts for GDP growth in 2022Q4-2023Q1 and have lowered our forecasts for growth during the second half of 2023. There is a number of reasons for these adjustments. To begin with, the economic impact of the energy crisis has been more benign than we thought before. Indeed, there has been no rationing of gas supply to industry and global energy prices have dropped sharply in the past few months, which has also resulted in a drop in energy price inflation. Next, we had expected a rebound in industrial production in the second half of 2022 as supply conditions ease, but this rebound has been stronger than expected, particularly in motor vehicle production. This has also resulted in a sharp jump in new car registrations which will have lifted private consumption growth in 2022Q4 and 2023Q1. Finally, the impact of monetary policy tightening famously works with long and variable lags and we judge that most of the cumulative impact of past and upcoming rate hikes and tightening financial and bank lending conditions is still very much to be felt on the economy. As a result, we now forecast a more shallow, but more prolonged recession.

The tightness in the labour market could result in some labour hoarding, an acceleration in wage growth and a loss in labour productivity during the early phase of the recession. We expect the unemployment rate to start rising gradually from the second quarter of 2023 onwards and for wage pressures to ease in the second half of this year and in 2024.

We have lowered our forecast for headline inflation in 2023 to 4.5% from 5.1% and we expect inflation to fall in line with the ECB’s 2% target by the end of this year. Core inflation (excluding food and energy) is expected to be more sticky and decline more gradually. As a result, core inflation should be higher than the headline rate in the final months of this year. We see core inflation falling gradually towards 2% in the second half of 2024.

Given the more resilient recent macro data, we expect the ECB to continue raising its policy rates until May, with a peak of 3% for the deposit rate (from 2.75% previously). Our new forecast is based on a 50bp rise next month, followed by two 25bp steps in the two subsequent meetings (though a solitary 50bp step in March is clearly also a possibility). We think that policy rate cuts will be on the agenda before the end of the year. Rate reductions would start the process of normalising policy back to more neutral settings in 2024.

This article is part of the Global Monthly of 23 January 2023