Eurozone - Spreading the pain

The tariff shock is unfolding more gradually, with a milder but more prolonged growth hit. The impact is also blunted by solid consumption, helped by falling rates and benign inflation. The ECB is now expected to look through the undershoot of its 2% inflation target. This means no further rate cuts on our forecast horizon, and the deposit rate holding at 2% for the foreseeable future.

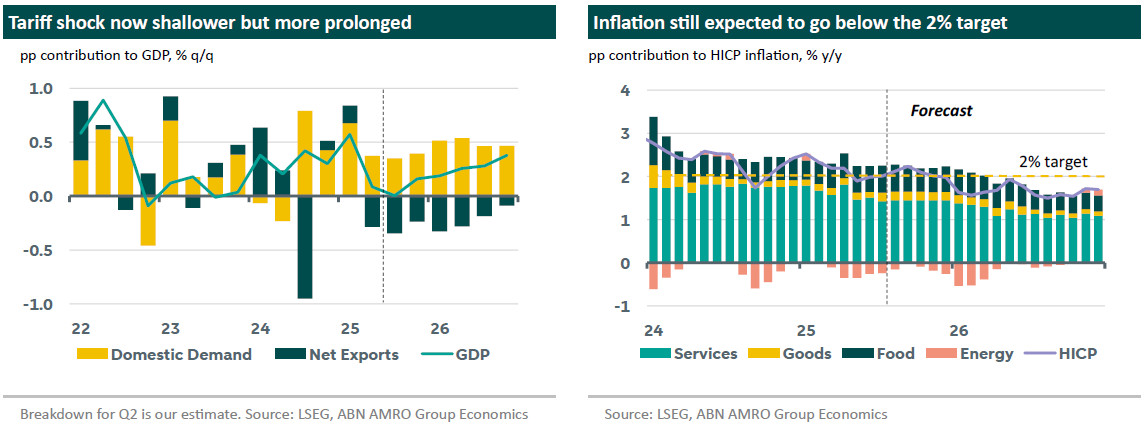

The eurozone proved more resilient than expected in Q2, with the economy eking out growth of 0.1% q/q, following the 0.6% jump in Q1; we had expected a small contraction reflecting the unwinding of US export frontloading in Q1. While that unwind is happening, it is unfolding more gradually than expected. A number of factors likely explain this. First, we have yet to see any tariffs on pharmaceuticals, which represent ¼ of EU exports to the US. With tariffs still looming for this sector, it is likely that the frontloading that started in Q1 extended into Q2. Second, it appears that large multinationals are initially opting to take a hit to their margins rather than immediately passing on the tariff to US consumers. Some European car and alcoholic beverage brands have pointed to margin hits from tariffs in their investor communications rather than price rises. This will not be sustainable over time, as businesses will be unlikely to accept a permanently lower profit margin (or even losses) in one of their biggest markets. But for the time being, this response to tariffs is blunting the consumer demand impact, which in turn blunts the fall in exports to the US. This means a milder near-term shock from tariffs than we previously assumed, but this spreads the pain over a longer time horizon rather than avoids it entirely (see also this month’s Global View).

The other factor keeping the economy going is a further solid expansion in consumer spending. While we do not have the full breakdown for Q2 GDP as yet, monthly data for retail sales and services in April-May points to growth of c0.3% q/q in private consumption. Consumption is being helped by falling interest rates, which are lifting housing transactions, as well as rising real incomes as wage growth continues to outpace inflation. Indeed, inflation remained broadly benign in July, with services inflation in particular normalising more quickly than expected. With that said, food inflation has been picking up again over the past few months, and this bears close watching given the outsized impact this typically has on household inflation expectations. Goods inflation also surprised to the upside, though this was more likely to be an anomaly. If anything, we expect goods inflation to face downward pressure over the coming year, on weaker demand from the US on the back of tariffs, as well as from more intense competition from Chinese goods. All told, we continue to expect falling energy prices to drive an undershoot of the ECB’s 2% inflation target in the coming quarters.

Despite the expected inflation undershoot, recent communication from the Governing Council (President Lagarde: policy is in “a good place”) suggests it is happy to look through this on the basis that inflation will eventually return to target during 2027. Although the ECB’s inflation projections factor in one more 25bp rate cut (based on market rate expectations in June), we doubt the Governing Council is minded to fine-tune policy to that degree. Cutting rates once after an extended pause risks sending confusing signals to markets. Given the recent emphasis in ECB communication on policy being in a good place, the more gradual hit from US tariffs, and the upside risks to growth in 2026 from higher German fiscal spending, we now expect the ECB to keep rates as they are for the foreseeable future, with the deposit rate staying at 2%. This represents a change to our previous base case that there would be another 50bp of rate cuts.