Eurozone wage growth levelling off

A number of wage growth reports for the eurozone was published in recent days. They seem to indicate that wage growth in the eurozone is no longer accelerating and has leveled off at still elevated levels close to 4.5-5%. We expect a more significant downward trajectory in wage growth to materialize in the second half of this year, as the expected economic weakness should hurt the labour market and result in moderate rises in unemployment.

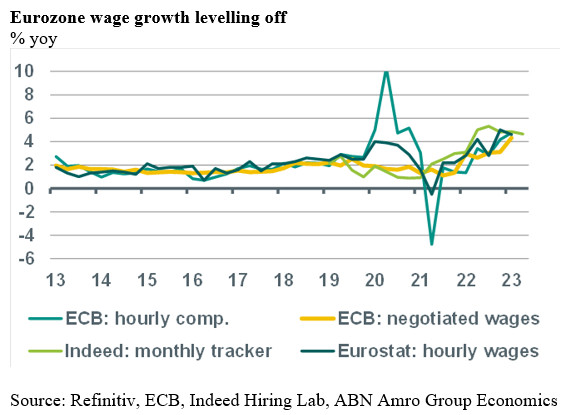

Wage growth probably peaked as vacancy rate edges lower

A number of wage growth reports for the eurozone was publshed in recent days. To begin with, Eurostat published its hourly labour costs report for Q1. The yoy rise in total labour costs (wages and non-wage costs) declined from 5.6% in 2022Q4 to 5.0% in 2023Q1. Hourly wage growth declined from 5.0% yoy to 4.6%, while the rise in non-wage costs (i.e. employers’ social contributions, employment taxes and subsidies) fell from 7.4% to 6.2%. The break-down in to the main sectors shows that wage growth increased in manufacturing (from 4.2% to 5.3%), whereas it fell in construction (from 6.4% to 4.4%) and total services (from 5.6% to 5.1%). The more detailed data shows that wage growth in a number of economic sub-sectors is well above average, for instance mining and quarrying (7.8% yoy), energy supply (9.8%), transportation and storage (7.0%), administrative and support services (7.5%) and arts, entertainment and recreation (6.0%), whereas it falls short in others, such as public administration and defence (2.7%), health and social work (4.8%) and education (3.5%). Next, the ECB has published data on compensation of employees, which differs somewhat from the Eurostat data (particularly with regard to the non-wage part of labour costs) but usually moves very closely in sync with the Eurostat series. The ECB reported a rise in the yoy change in hourly compensation from 4.2% in 2022Q4 to 4.7% in 2023Q1 and a rise in the change in compensation per employee from 4.8% to 5.2%. So, although the level of wage growth according to the ECB is quite close to the Eurostat, it picked up somewhat in Q1, whereas it declined according to the Eurostat data. The ECB’s preferred measure of wage growth, negotiated wages, increased from 3.1% in Q4 to 4.3% in Q1. Finally, monthly high frequency data for wage growth from Indeed job postings indicate (as published by the Indeed Hiring Lab) that wage growth decline from 5.0% in April to 4.3% in May after it had trended around 5% in previous months.

Wrapping up all the above reports, it looks like wage growth in the eurozone is no longer accelerating and has leveled off at still elevated levels close to 4.5-5%. We expect a more significant downward trajectory in wage growth to materialize in the second half of this year, as the expected economic weakness should hurt the labour market and result in moderate rises in unemployment. A first sign of a gradual cooling of the labour market came with the publication of the eurozone vacancy rate last week. It declined from 3.1% in 2022Q4 to 3.0% in 2023Q1. It peaked at 3.2% in 2022Q2 and has edged lower since then. The vacancy rate in industry and construction declined from a peak of 2.9% in 2022Q2 to 2.7% in 2023Q1, while that in services fell from 3.7% to 3.4%.