ESG Strategist – ESG issuance expected to considerably lag in 2025

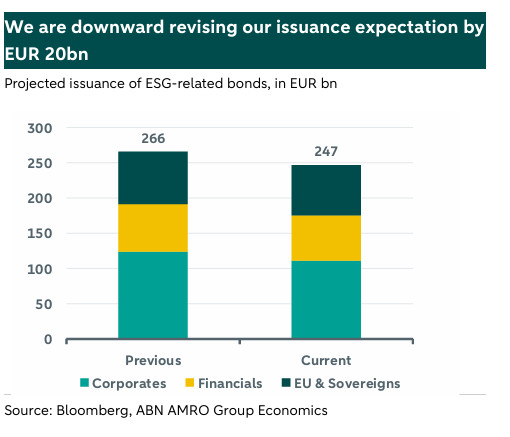

There was a noticeable surge in negative news related to ESG in the first half of the year, which has impacted the issuance of ESG-labelled bonds. Initially, we expected ESG issuance to total EUR 266bn in 2025, but we have adjusted our forecast down to EUR 247bn. In the financials space, that downward revision stems from less ESG-labelled senior non-preferred bonds in Q2. With regards to corporates, the issuance of ESG-labelled bonds by utilities’ companies has also fallen short of our forecast, and we now expect it to total EUR ~50bn by year-end. And, finally, concerning sovereigns, we are also downward revising our forecast for NextGenerationEU issuance in EUR 3bn, in line with the trend registered in the first half of the year.

In the first half of the year, there was a noticeable surge in negative news related to Environmental, Social, and Governance (ESG) issues. In the United States, President Donald Trump declared a "national energy emergency" early in the year, prioritizing fossil fuels over clean energy initiatives. Subsequently, major energy companies like BP announced reductions in renewable energy investments, opting to concentrate on oil and gas production. Additionally, prominent American banks revealed their departure from the Net-Zero Banking Alliance (NZBA), raising concerns about waning climate commitments, while the NZBA also updated its guidelines from a strict 1.5o degree target to a more flexible “well below 2o degree target” (read more here).

In Europe, the European Commission proposed the Omnibus amendment in February (see here), aiming to significantly reduce the number of companies required to adhere to regulations such as the Corporate Sustainability Disclosure Regulation (CSRD). Furthermore, there are considerations to relax the 2040 emission reduction target, as reported in recent updates (see here). These developments suggest that both regulators and companies worldwide might be scaling back their climate ambitions.

This note explores the impact of these developments on the issuance of euro-denominated ESG-related bonds during the first half of the year, as well as how that relates to our initial projections for issuance in 2025.

Total issuance lower than initially forecasted

At the start of the year, our forecast predicted that total ESG issuance in euros would reach EUR 266bn, accounting for issuances from corporates, sovereigns, the EU, and financial institutions. This projection already factored-in a slight decline of 3% compared to 2024. However, in light of the aforementioned developments, issuance is expected to fall short of our initial expectations, and we do not anticipate a recovery to the originally projected levels in the remaining months of the year. Consequently, we now estimate that issuance will most likely total EUR 247bn by year-end, representing a roughly EUR 20bn reduction from our previous estimates.

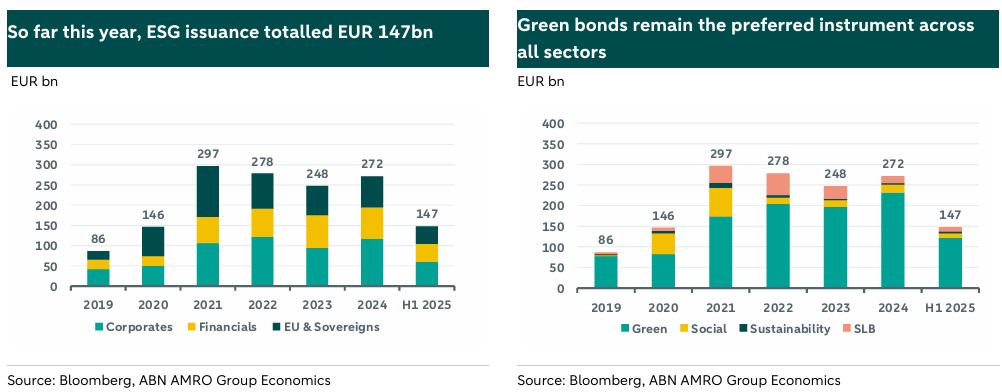

Thus far this year, ESG issuance has reached EUR 147bn. Of this total, 29% originated from financial institutions, another 29% from European sovereign entities and the EU, and the remaining 41% from corporates. As anticipated, green bonds continue to be the preferred choice across all sectors. Out of the total EUR 147bn, 83% carry a green label, 7% have a social label, 3% are classified as sustainable, and the remaining 7% are labelled as Sustainability-Linked Bonds (SLBs). Although sustainable-labelled bonds represent the smallest share, their absolute issuance of EUR 5bn has already exceeded the total issuance for 2024, suggesting a potential resurgence for these instruments.

Were the second half of the year to follow the same issuance trend registered in the first half of the year, total issuance would equal EUR 215bn, 19% less than our initial forecast. This is one of the reasons prompting us to revise our issuance forecast for 2025. The factors contributing to this decline in issuance will be explored in detail within each sector’s section below.

Financials

Up to this point in the year, financial institutions have issued EUR 43bn in ESG-labelled bonds, accounting for 15% of the total bond issuance. This is only slightly lower than last year’s share, which was 16% during the same period, indicating that despite negative news surrounding ESG, both issuers and investors remain interested in ESG-labelled instruments.

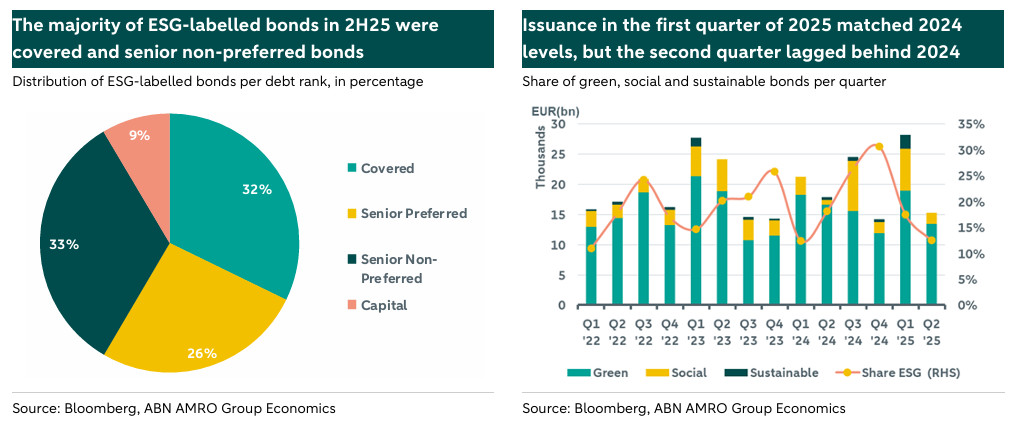

Of the EUR 43bn, 32% consists of covered bonds, 26% are senior-preferred bonds (SP), 33% are senior non-preferred bonds (SNP), and the remaining 9% pertains to capital instruments, including Tier 2 and AT1 bonds. If the second half of the year mirrors the trend observed in the first half, the total issuance of ESG-labelled bonds would reach EUR 63bn, falling EUR 4bn short of our initial forecast for the year.

This shortfall is primarily driven by senior non-preferred bonds. Initially, we anticipated that ESG-labelled senior non-preferred bonds would total EUR 27bn in 2025, comprising 30% of the total issuance of senior non-preferred bonds, consistent with 2024 figures. However, in the first half of the year, only EUR 14.35bn have been issued, accounting for only 16% of the total senior non-preferred bond issuance. This lower share is not due to a lower number of ESG-labelled bonds being issued, as a similar volume of ESG senior non-preferred was placed during the same period last year. As such, the decrease in share is mainly driven by a larger issuance of non-ESG-labelled senior non-preferred bonds. This likely results from banks prioritizing riskier ranks in the first half of the year, as issuance conditions remained relatively favourable despite geopolitical tensions and heightened financial market uncertainty. We note as well that there is a lengthy process for ESG bond issuances, and timing for issuance becomes a key factor during volatile markets, which might have been an additional contributing factor for why issuers have given preference to non-ESG labelled debt. This reasoning helps to explain also why particularly the second quarter was a lagger this year (see chart on the next page on the right). Looking ahead, we expect the ratio of ESG-labelled bonds to total senior non-preferred issuance to increase from 16% to 20% by year-end, which is still significantly lower to our initial forecast of 30%.

Regarding the other categories of debt, we do not expect significant deviations from our initial forecasts. Therefore, we anticipate ESG-labelled covered bond issuance to reach EUR 18bn by year-end, accounting for 12% of total covered bond issuance. The proportion of ESG-labelled senior-preferred bonds relative to total senior-preferred bonds is expected to be approximately 25% by year-end, amounting to EUR 17.5bn. Lastly, for capital instruments, we foresee a slight decrease in the share of ESG-labelled bonds from 9% to 7% by year-end, totalling EUR 5.2bn.

Corporates

So far this year corporate euro ESG issuance has amounted to close to EUR 61bn, which is roughly half of what we forecasted at the beginning of this year. ESG instruments represent around 15% of total corporate issuance in 2025, a considerable decrease from last year’s 20%. In contrast to financials, corporate issuers seemingly have been impacted by the negative sentiment around ESG this year.

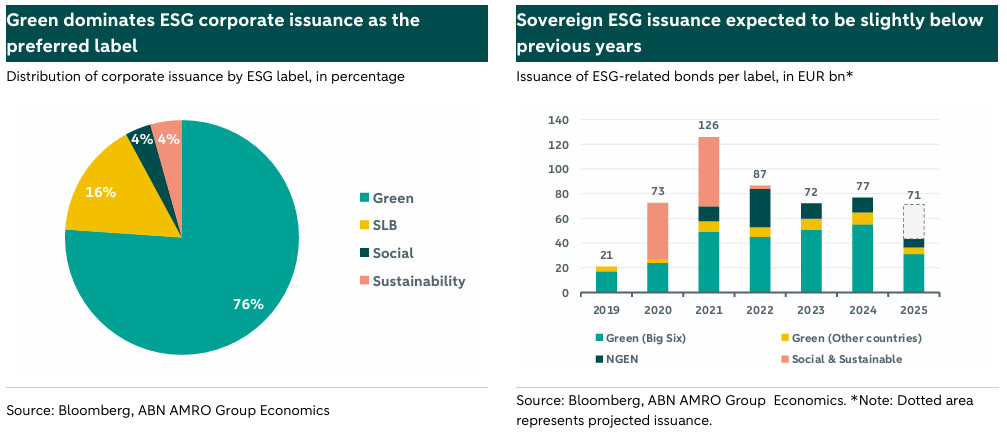

This year, the green label continues to dominate corporate issuance (see chart below on the left), with 76% issued in this format (vs 79% in 2024), followed by SLBs (16%, vs. 15% in 2024). Social and sustainability bonds each represent 4% of total issuance.

For the remainder of the year, we revised down our forecast for total issuance by EUR 12.4bn, considering an adjustment in our expectations with regard to utilities’ issuance. All categories considered, we forecast another EUR ~50bn to be issued in ESG format until the end of this year. That would imply total issuance for 2025 will be around EUR 111bn, slightly below last year’s EUR 117bn.

Sovereigns

In the sovereigns and EU space, approximately EUR 43bn in ESG-format bonds have been issued so far in 2025. Were the second half of the year to mirror the first half's trend, the total ESG bond issuance for 2025 would amount to EUR 63bn, which is around EUR 10bn less than our initial forecast. However, we anticipate that some sovereigns will increase their ESG bond issuance, but we still forecast EUR 3bn less ESG bond issuance than we initially projected. As such, for sovereigns we also revise down our forecast from EUR 74.3bn to EUR 71.3bn. The reason for that regards a reduced issuance under the NextGenerationEU (NGEU) programme, which we initially projected to reach EUR16bn by year-end, similar to the proportion issued in 2024. However, we are now revising the annual issuance downward to EUR13bn, given that the EU has issued EUR6.85bn under the NGEU in green format so far—already 40% less than during the same period last year—and we do not expect them to meet the initial EUR 16 bn forecast. These EUR 6.85 bn represent 7.6% of the total EU's bond issuance in 1H25 (EUR 90 bn). Assuming a similar share in the second half of the year and considering EU’s plans to issue EUR 70bn in 2H25, we arrive at a total of close to EUR 13bn of green bonds issued by the EU.

Regarding sovereigns, the “Big Six” (Germany, Italy, France, the Netherlands, Belgium and Spain) have issued EUR 31bn in ESG-labelled bonds so far this year, reflecting a 7% increase compared to the same period last year. However, in percentage terms, the share of ESG-labelled bonds relative to total bonds has slightly decreased from 5% to 4%, due to increased issuance of non-ESG-labelled bonds this year.

The rise in ESG-labelled bonds is mainly driven by Italy, which has already issued almost as much as it did throughout last year. Looking at the other sovereigns, some are currently below our initial expectations; nevertheless, we expect them to ramp up issuance in the second half of the year. Thus, we have not revised our forecasts downward for sovereigns. Overall, considering these elements, we still anticipate total sovereign issuance, encompassing all EU countries, to reach the initially expected EUR 58bn by year-end.

All in all, we expect EUR 20bn less of issuance than initially forecasted

In summary, despite the adverse news surrounding ESG-related matters, the impact has varied across sectors. In the financial sector, we've only adjusted our forecast downward by EUR 4bn, primarily due to lower-than-anticipated issuance of ESG-labelled senior non-preferred bonds, implying we project now a total issuance of EUR 63bn in 2025.. As for corporate issuers, we have revised our forecast down by EUR 12.4bn, resulting in a total of EUR 111bn, mainly due to a reduction in our utilities issuance forecast. Finally, regarding sovereign issuers, our expectations have also been lowered by EUR 3bn, attributed to a reduced issuance of NGEU bonds. Overall, these adjustments have culminated in a EUR 20bn downward revision of our issuance forecast, which we consider not as negative, given the significant policy shifts in some other Western countries.