Fed hikes 75bp, with another 75bp likely in July

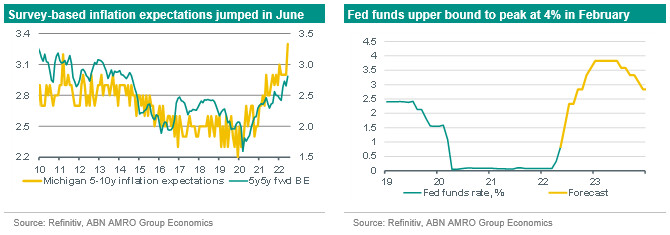

At its June policy meeting, the FOMC raised the target range for the fed funds rate by 75bp, taking it to 1.50-1.75%. Following the move, we now expect a further 75bp rate hike in July, but keep our expectation for the upper bound of the fed funds rate peaking at 4% in February.

While the 75bp hike was higher than our base case of 50bp, we saw a of such a move following the upside surprise in the May inflation reading last Friday. The inflation reading, combined with a surprise rise in long-term consumer inflation expectations, drove a rapid repricing in market expectations for rate rises for the coming year, with markets now fully pricing in our revised call last week for the upper bound of the fed funds rate to peak at 4% in early 2023. There was little notable change to the policy statement, but the quarterly update to the Committee’s projections showed that it expected much steeper rate rises than in the March projections, with the expected peak in the fed funds rate now consistent with our own of 3.75-4% in 2023 (previously around 1pp lower). Thereafter, the Committee expects policy to be modestly eased in 2024, although to a lesser extent and later than our expectation (around 50bp of rate cuts in 2024 vs our expectation of 100bp in cuts in H2 2023). Growth forecasts were significantly downgraded, and unemployment forecasts raised, although the extent of these changes was also less marked than published Tuesday. The Committee now expects unemployment to rise around half a percentage point over the coming year, to 4.1% by Q4 2023, while we expect a considerably bigger rise of 1.5pp, to around 5% by early 2024. In the press conference, Chair Powell continued to emphasise price stability as the ‘bedrock’ of the economy and a strong labour market, thereby acknowledging that some rise in unemployment in the near-term would be a necessary sacrifice to get inflation back to target. While stating that rate hikes of 75bp and 50bp should be viewed as rare steps, he said that it was quite likely the Fed would raise rates by a similar magnitude at the July meeting, thereby giving the FOMC more ‘optionality’ as it approaches the likely long-run neutral rate of c.2.5%.

Fed funds upper bound still likely to peak at 4% in early 2023

Following the meeting, we have revised our Fed call to include one further 75bp hike in July, with this followed by 50bp moves in September and November, and 25bp hikes in December and February. With this, we maintain our expectation for the upper bound of the fed funds rate to peak at 4% in February, but with a greater front-loading of tightening than we previously expected (previously, we expected 50bp moves at each meeting until February). The risks to rates continue to be to the upside, as are the risks to the inflation outlook itself.