Fed will still hike 50bp, despite US GDP fall

US GDP contracted in Q1, by -1.4% q/q annualised, against expectations for a continued expansion in the economy (consensus: +1.0% ABN: +1.4%). The contraction reflects continued supply bottlenecks in Q1, with demand remaining strong. As such, the data will do little to sway the Fed from raising rates 50bp at its May meeting, in our view.

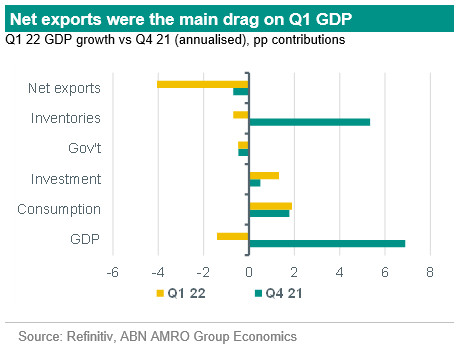

Supply-side continued to struggle in Q1

The details showed domestic demand remained solid, as expected, with private consumption still growing well above trend at 2.7% annualised. We had expected this to be offset by a drag from the struggling supply-side of the economy, but that drag was even bigger than forecast - net exports subtracted -3.2pp, inventories -0.8pp. The contribution from investment was also considerably less than we expected (+0.4pp vs our forecast of +1.8pp), while government spending subtracted -0.5pp. Looking ahead, we are likely to see a strong rebound in Q2, and a reversal in the drivers of GDP. Net exports are likely to make a significant contribution as the exceptional strength in imports of the past two quarters unwinds, partly on cooling demand but also due to lockdowns in China. At the same time, there are other signs that the supply side is recovering, with (trucking and port congestion) easing, and as the Omicron wave recedes. Meanwhile, demand is cooling on the back of elevated inflation and tighter monetary policy; indeed, we already saw this in the latter half of Q1, with retail volumes falling, and we expect consumption to be broadly stagnant in Q2, as a further correction in goods consumption offsetting a continued recovery in services demand. We keep our 2022 growth forecast at 3.1% for now, though today’s release means there are some downside risks to this outturn. Despite the contraction in Q1, we continue to think a recession is unlikely in the US, although the probability is not insignificant given the many headwinds facing the economy – we would peg it at 20-25%.

Fed still on course to hike 50bp in May

The Q1 GDP report does nothing to change our view for the Fed; indeed, the 8% annualised surge in the GDP deflator served to underline the ongoing and significant challenge of higher inflation the Fed faces. We continue to expect 50bp rate hikes in May and June, with the Fed to continue hiking in 25bp steps thereafter. This would take the target range for the fed funds rate to 2.5-2.75% by early 2023. Thereafter, we expect the Fed to pause, with inflation likely to be materially lower by that point, and pipeline pressures such as wage growth also likely to have eased.