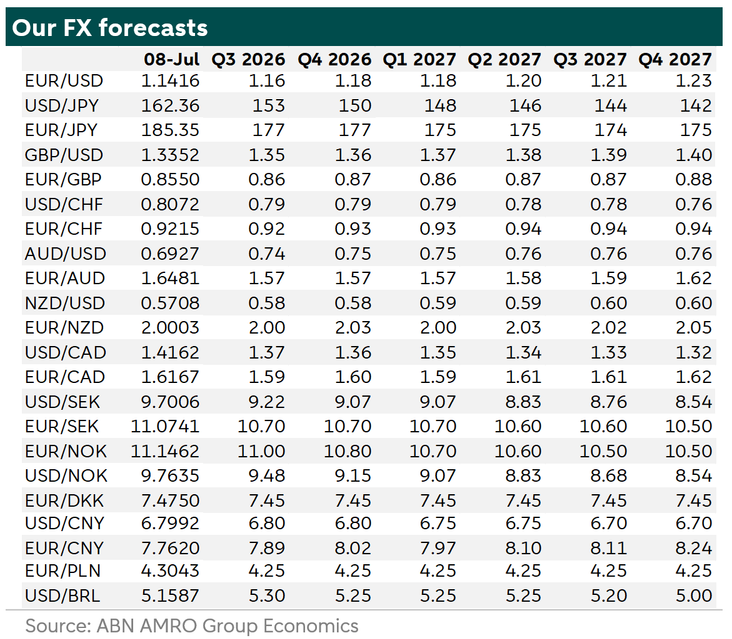

FX Weekly - Energy prices back in focus

The euro’s sensitivity to energy prices has shifted, but the recent rise in energy prices has again weighed on the currency. Financial markets are testing how far the authorities will tolerate yen weakness. The Reserve Bank of New Zealand raised rates by 25 bp and signalled that further rate hikes are likely.

Euro and energy prices

The sensitivity of the euro to energy prices has shifted. At the start of the US-Iran conflict, higher energy prices weighed on the euro against the US dollar. During the conflict, however, EUR/USD became less sensitive to energy prices and more sensitive to expectations for the Fed and the ECB. When a Memorandum of Understanding was announced, energy prices fell sharply, but the euro gained little against the US dollar because markets were focused on expectations of Fed rate hikes. More recently, Iran attacked an LNG tanker and the US launched airstrikes on 80 sites in Iran. As a result, oil and gas prices rose strongly, supporting the currencies of energy exporters such as the Norwegian krone, Canadian dollar and US dollar. At the same time, currencies of energy importers weakened. The euro again declined against the US dollar as energy prices rose. Going forward, the direction in EUR/USD will depend on expectations for the Fed and the ECB, inflation expectations, changes in nominal and real yield spreads between the US and Europe, and perceptions of possible energy shortages in the eurozone. Thinner markets during the holiday period could amplify moves compared with normal market conditions.

The market is testing the authorities’ stance on yen weakness

Investor sentiment towards the yen remains weak. The push by the Japanse government for fiscal expansion and a preference for a more accommodative Bank of Japan policy stance are weighing on the currency, while Japan’s position as a major energy importer adds further pressure. Despite these factors, we noted in last week’s FX Weekly that the risk of intervention in the yen had increased. The market was cautious last week after reports suggested that Japanese officials may stop signalling intervention intentions in advance. However, as no intervention took place, investors became more confident and pushed the yen lower against both the US dollar and the euro. USD/JPY is now approaching last week’s high of 162.84 and could move towards 164.50. The fact that intervention has not yet happened does not mean it will not happen. Market conditions remain risky. A stop-loss order may not provide full protection, as the next traded price could be much lower if intervention occurs. As we mentioned last week, positioning remains stretched: the market is long US dollars and very short yen. If sentiment turns in favour of the yen, be it because of intervention concerns or other factors, the rebound could be sharp. In that case, USD/JPY may not return to this week’s levels for some time.

Reserve Bank of New Zealand hikes by 25bp and signals more to come

This week, the Reserve Bank of New Zealand raised its policy rate by 25bp to 2.5%. In its statement, the central bank said that although energy prices have fallen, the impact of the shock will continue for some time and the outlook for medium-term inflation pressures remains uncertain. It also said that, with inflation still above target and economic activity expected to strengthen, further reduction in monetary stimulus is likely to be needed to bring inflation back to the 2% target midpoint. Future OCR decisions will depend on incoming data, price-setting behaviour and the strength of economic activity, and how these factors affect medium-term inflation pressures. The market is pricing in almost 40bp of additional rate hikes this year. Our RBNZ view is close to market consensus, although we are more dovish than the market for the Fed. As a result, we expect modest upside for the New Zealand dollar against the US dollar.