Germany - Weaker outlook amid rising risks and political uncertainty

Q1 GDP rose 0.3% q/q in Q1. Leading indicators signal ongoing but slowing momentum. We have downgraded our forecast from 0.8% to 0.7% this year and from 1.2% to 1% next year. Increasing inflation and softening labour market conditions will affect purchasing power. Limited reform progress and growing political fragmentation add uncertainty to the economic outlook.

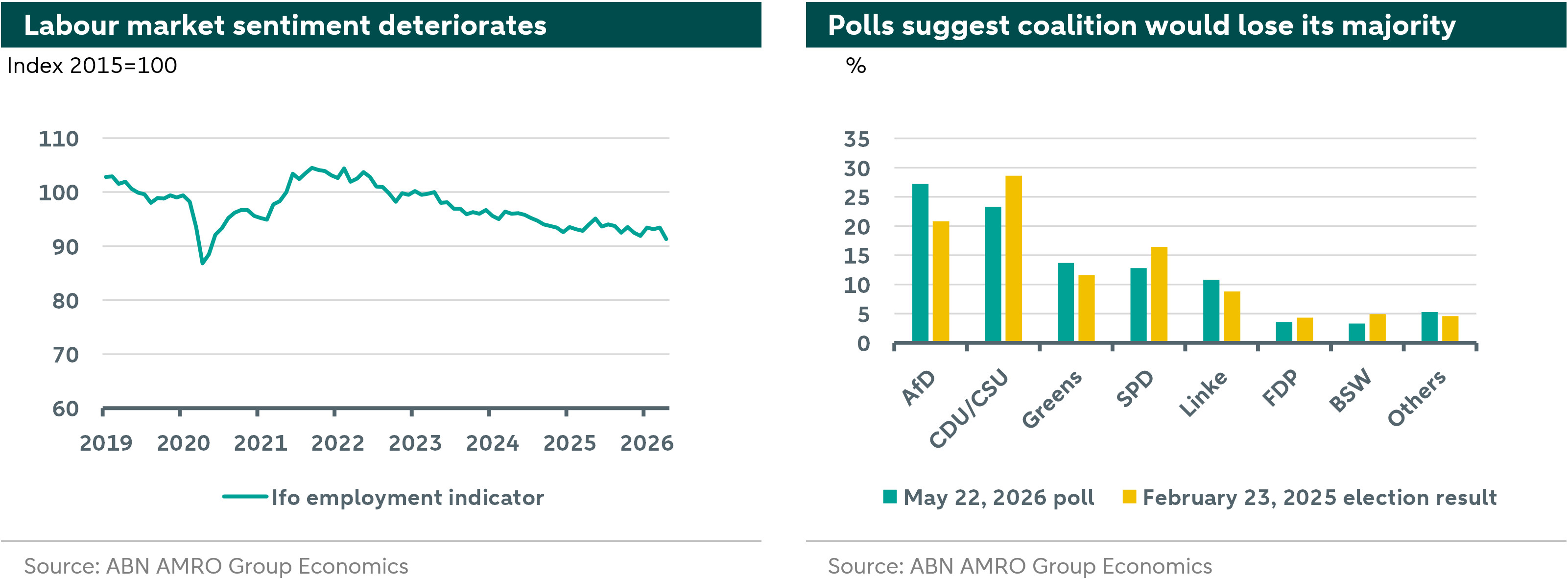

GDP grew by 0.3% quarter-on-quarter in the first quarter, a stronger-than-expected headline figure that overstates the underlying momentum of the economy. Domestic demand remained stagnant, while the increased contribution from exports was likely boosted by temporary factors such as frontloading. The war in Iran weighed only modestly on economic activity, but the negative impact of higher energy prices is expected to intensify in the coming quarters, leading to a slowdown in growth momentum. As a result, we have revised down our GDP growth projections for 2026 and 2027. We now expect growth of 0.7% in 2026 (down from 0.8%) and 1.0% in 2027 (down from 1.2%). While this still represents an improvement from 2025 (0.3%), the rebound is weaker than anticipated at the start of the year. That said, some positive developments are likely to support stronger growth compared with last year. Government spending—particularly on defence—is feeding through into higher industrial demand. For now, however, leading indicators point to a slowdown. The manufacturing PMI fell to 49.9 in May, just below the 50 threshold that signals contraction. Similarly, the Ifo business expectations index declined from 90.3 in February to 83.8 in May. Notably, these weaknesses predate the Iran crisis: industrial production has been stagnating again since early 2026. There are, however, some encouraging signs. According to the , three-quarters of value added in manufacturing now comes from sectors whose product portfolios are largely composed of fast-growing products. This suggests that the German manufacturing sector is undergoing productivity-enhancing restructuring. Hence, the German economy appears better positioned to benefit from rising global demand than in recent years. At the same time, low capacity utilisation and tighter bank lending conditions are weighing on corporate investment, while households are becoming more cautious. Inflation rose from 2.0% in March to 2.9% in April, driven by higher energy prices. Despite temporary tax reductions on energy, further upward pressure on prices is likely as higher energy costs feed through into other categories. Labour market conditions are also becoming less favourable. Wage growth is slowing, and unemployment is rising, partly due to corporate restructuring.

The German economy continues to require structural reforms, which remain difficult to implement. Within the governing coalition, tensions persist over the distributional effects of income and inheritance tax reforms, and disagreements extend to pension reform. Some progress has been made in healthcare, where current proposals aim to better align expenditure and revenues. Nevertheless, the political environment remains challenging. Weak results in recent state elections have deepened divisions between the centrist and left wings of the SPD and further weakened Chancellor Merz’s already limited authority. With state elections scheduled this autumn in Berlin, Mecklenburg-Western Pomerania, and Saxony-Anhalt, uncertainty is likely to increase. In the latter two eastern states, the far-right AfD is leading in the polls. A strong electoral performance could weigh on the business climate and investment. Any decision by the local CDU to consider cooperation and lift the cordon sanitaire would mark a significant political shift.