Key views Global Monthly April 2024

Growth indicators are bottoming out in the eurozone and China, while the US economy is gradually cooling. Big picture, the global economy is slowly converging towards a more trend-like pace of growth, and this remains our base case for the second half of 2024. Global trade and industry are beginning to recover, but a sharp rebound is unlikely while rates remain restrictive. On the positive side, inflation has fallen significantly and is now within touching distance of central bank targets. The impact of the conflict in the Middle East has receded and the inflation impact is likely to be minimal. Further falls in inflation will enable central banks to pivot to rate cuts by mid-2024, and financial conditions have eased in anticipation of this. Still, interest rates will stay high for some time yet, and this will keep a lid on the recovery.

Macro

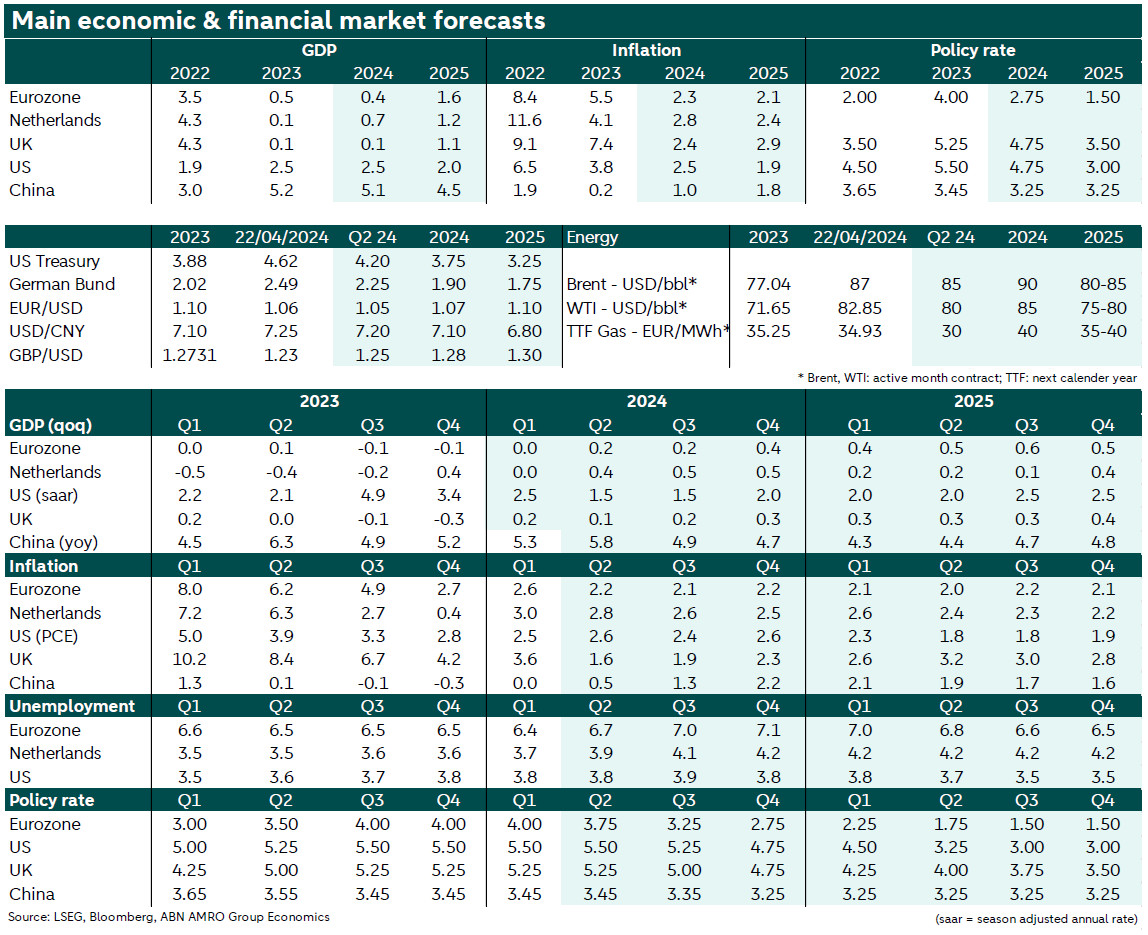

Eurozone – Incoming economic data and survey results for January-March have indicated that GDP stagnated for the sixth consecutive quarter in 24Q1. PMI results of April suggest GDP growth is already picking up slightly moving into the second quarter. Growth should expand moderately during the rest of the year, as global trade and industry bottom out, which will support EZ exports. Domestic spending is expected to increase as well on the back of high wage growth and lower inflation but deteriorating labour market conditions and fiscal retrenchment prevent a strong recovery.

The Netherlands – Growth will increase to 0.7% in 2024 and 1.2% in 2025, mostly driven by private consumption on the back of a purchasing power recovery. First quarter GDP is expected to roughly stagnate, as consumption falls back, and private investments and exports stay weak on the back of elevated interest rates and the weak external environment. Over the course of 2024, as financial conditions ease and external demand increases, we will see a more broad-based pick-up in growth. Labour market tightness remains, but the unemployment rate will marginally rise to 4.0% in 2024.

UK – Disinflation has continued, providing some relief to the Bank of England, but upside inflation risks remain significant given that wage growth is still elevated and well above levels consistent with the 2% target. At the same time, the economy has continued to stagnate, weighed by high rates and weak confidence. Over time, we expect the weakness in demand to dampen wage growth, which should help to bring down services inflation. But the normalisation in inflation may take longer in the UK than in other advanced economies, due to historically higher inflation expectations.

US – Growth is slowing to a more trend-like pace in the early months of 2024, following well above trend growth in H2 2023. However, the economy continues to be more resilient than expected in the face of high rates, likely reflecting the solid balance sheets of households and businesses. Still, weak bank lending and pockets of financial stress among households are likely to contribute to a further slowdown in growth. Inflation has come in on the firm side in recent months, but pipeline pressures – particularly benign wage growth – continue to point to the Fed meeting its 2% target in the course of this year.

China – Qoq growth accelerated in Q1-24, in line with our base case, benefiting from stimulus and a bottoming out in global manufacturing. However, the latest data confirm that the recovery remains unbalanced, with the supply side still stronger than the demand side, and property still adding to headwinds. Meanwhile, risks from trade spats are rising. On the back of the Q1 GDP data, we made some backward-looking revisions to our growth forecasts. We raised our 2024 forecast to 5.1% (from 4.7%) and cut our 2025 forecast to 4.5% (from 4.6%).

Central Banks & Markets

ECB – The ECB kept policy rates unchanged in April. In the Policy Statement the ECB explicitly mentioned rate cuts for the first time. In the press conference the ECB made clear that if the inflation outlook, underlying inflation and the strength of monetary policy transmission were according to expectations, it would be appropriate to cut the policy rate. We believe these three conditions have been largely met already and continue to expect a June start to rate cuts, after which the ECB will cut rates at each meeting from June onwards for a total of 125bp rate cuts.

Fed – We expect rate cuts to start in July, with a pause in September as the Fed waits to gain confidence in the inflation outlook. We then expect consecutive rate cuts from November on. Even with rate cuts starting this year, monetary policy is expected to remain restrictive throughout 2024 and into 2025. We expect the upper bound of the fed funds rate to reach 4.75% by end-2024, and 3% by end-2025. The Fed also looks set to slow down its quantitative tightening somewhat sooner than previously expected. We expect an announcement in May, with a slower pace of QT starting in the second half of 2024.

Bank of England – The MPC has kept policy on hold since last August. We think Bank Rate has peaked at 5.25%. The BoE is in full data-dependent mode, and UK macro data has been erratic over the past year. We do not expect rate cuts until next August. The risk is tilted towards somewhat earlier cuts given the more rapid progress on inflation. However, sticky wage growth – which poses upside risks to medium-term inflation – is likely to stay the MPC’s hand. Rate cuts are likely to be more gradual than for the ECB and Fed, with only two rate cuts (total 50bp) expected in 2024, and four rate cuts (total 100bp) in 2025.

Bond yields – The higher-for-longer theme is back after a few months of dovish sentiment in markets. There are now only 1.5 rate cuts priced for the Fed and 3 for the ECB. The market also now prices in a higher terminal rate (to 4.2% and 2.5% for the Fed and ECB respectively). This is roughly 100bp higher than what both central banks estimate as neutral rate. In our view, the recent market shift is overdone. We expect the market to gradually adjust its terminal rate estimates lower once we enter into the rate cut cycle. This will lead to a sharp drop in bond yields overall.

FX – Following the update to our Fed view, we are now more dovish for the ECB than for the Fed compared to the market and this justifies a stronger dollar and lower EUR/USD. EUR weakness from current levels will materialize in the coming months as long as the cut expectations on the ECB run ahead of rate cut expectations of the Fed. As soon as the Fed begins the easing cycle and markets start to anticipate a larger number of rate cuts in 2025, the dollar will probably decline. Our new forecasts for Q2 and Q3 are 1.05 and for year-end 1.07. Before, these forecasts stood at 1.10.