Key views Global Monthly June 24

Growth indicators are showing signs of a pickup in the eurozone and China, while the US economy is gradually cooling. Big picture, the global economy is slowly converging towards a more trend-like pace of growth, and this remains our base case for the second half of 2024. Global trade and industry are slowly recovering, but a sharp rebound is unlikely while rates remain restrictive, and possible new trade tariffs pose an additional risk. Inflation has fallen significantly, and progress towards the 2% target has resumed in the US following the hiccup in early 2024. The impact of the conflict in the Middle East has receded and the inflation impact of the rise in shipping tariffs is likely to be minimal. The ECB has started lowering interest rates, and we expect falling inflation and a softening labour market to enable the Fed to do the same in September. Still, rates will stay high for some time yet, and this will keep a lid on the recovery.

Macro

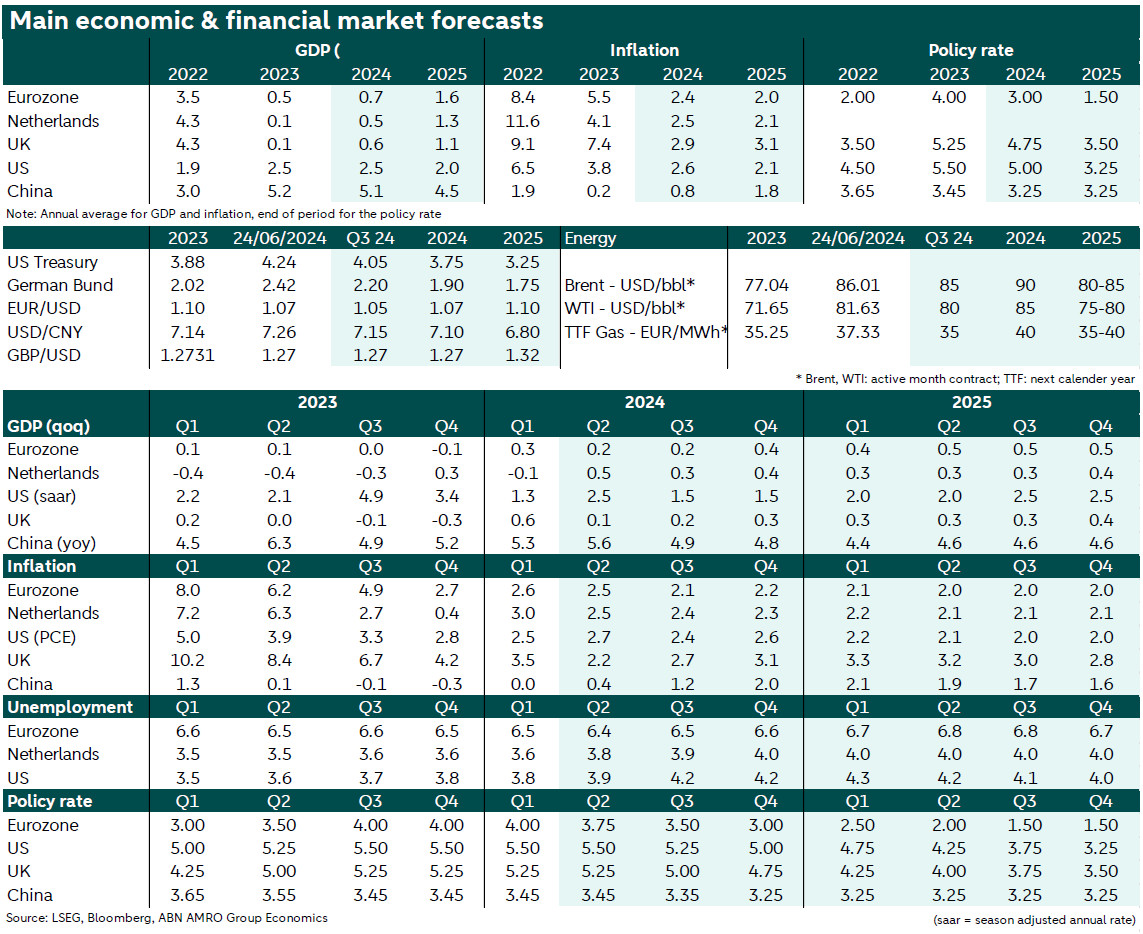

Eurozone – Growth is expected to remain positive in Q2 but edge lower compared to the strong Q1 reading. We have penciled in 0.2% of qoq growth in Q2. Overall, the eurozone economy is slowly regaining its footing, economic activity is expanding in the services sector while manufacturing continues to bottom out. Growth is expected to remain below the trend rate over 2024. In May, core inflation surprised to the upside due to strong services inflation, in part driven by the pass-through of wages. Leading indicators however suggest disinflation will broadly continue in the coming months.

The Netherlands – Despite the contraction in Q1, GDP growth is expected to pick up and to average 0.5% in 2024. Government spending and household consumption are the drivers of this gradual growth. The stimulus measures in the newly announced coalition agreement led us to slightly raise our growth forecast for 2025 from 1.2% to 1.3%. Inflation is continuing its downward trend. However, the price trend of components with a large wage element – such as labour-intensive services – is slowing the path downward. Inflation is expected to average 2.5% in 2024 and 2.1% in 2025.

UK – The election is expected to have no implications for growth and inflation, despite the expected change of government. This is due to the lack of fiscal space and the limited appetite to re-open Brexit policy. The economy is recovering from a prolonged period of stagnation on the back of high rates. Disinflation is continuing, but services inflation is stubbornly high, due to wage growth that is still well above levels consistent with 2% inflation. The return to 2% inflation will take longer than in other advanced economies, due to historically higher inflation expectations in the UK.

US – Following a surprisingly low growth reading in Q1 of 2024 on the back of higher imports, we expect a reversal with above trend growth for Q2. Still, weak bank lending and pockets of financial stress among households are likely to contribute to a slowdown in growth in the second half of the year, before returning to trend next year. The disinflationary process has resumed in recent months, and we expect it to continue in the remainder of the year, with the 2% y/y target in sight in the course of 2025.

China – Recent macro data confirm that drags from the property sector remain, despite the rolling-out of further measures to stabilise the sector. Growth is supported by stronger momentum in exports, but external risks are rising, as China's overcapacity contributes to trade spats. Following an investigation launched in September 2023, Brussels announced it would raise import tariffs on EVs made in China. We still expect European authorities to maintain a balanced approach, also taking into account the risk of Chinese retaliation. Meanwhile, Germany is trying to water down these tariffs.

Central Banks & Markets

ECB – The ECB started its rate cut cycle with a 25bp rate cut at the June meeting, in a widely telegraphed move. In the policy statement the ECB refrained from pre-committing to a particular rate path. In the press conference however Lagarde hinted that a signal on a future move would come only after the July meeting. May’s inflation data support this wait-and-see approach. As a result, we no longer expect a follow up rate cut in July. Starting at the September meeting, our base case still foresees an extensive rate cut cycle with 25bp cuts at consecutive meetings.

Fed – We expect rate cuts to start in September, with additional rate cuts once every quarter until March 2025. Afterwards, we expect consecutive rate cuts at each meeting. The Fed will remain attentive to upside risks to inflation and downside risks to the labor market. Monetary policy is expected to remain restrictive throughout 2024 and into 2025. We expect the upper bound of the fed funds rate to reach 5.00% by end-2024, and 3.25% by end-2025.

Bank of England – The MPC has kept Bank Rate at 5.25% since last August. Incoming data suggests stubbornly high underlying inflationary pressure, but Governor Bailey’s dovish bias continues to support our expectation for rate cuts to start this coming August. With that said, sticky wage growth – which poses upside risks to medium-term inflation – is likely to keep rate cuts at a more gradual pace than for the ECB and Fed, even into next year. We expect only two rate cuts (total 50bp) in 2024, and four rate cuts (total 100bp) in 2025, with Bank Rate falling to 3.5% by end-2025.

Bond yields – The French snap election created high uncertainty and volatility in the European debt market, leading to a sell-off in OATs that also spilled over to other EGBs. Once the political outcome is known and investors get a better insight into the economic policy and approach to the EU of the new government, we expect country spreads to tighten (with OATs still underperforming). Regarding outright yields, levels came down following recent macro data in the US and in EZ indicating weaker economic activity. Markets repriced the terminal rate lower in response for both the Fed and the ECB.

FX – EUR/USD has been rangebound. EUR weakness from current levels will materialize in the coming months as long as rate cut expectations for the ECB run ahead of rate cut expectations of the Fed. As soon as the Fed begins its easing cycle and markets start to anticipate a larger number of rate cuts in 2025, the dollar will probably decline. Our forecasts for Q2 and Q3 are 1.05 and for year-end 1.07. Our forecast for end 2025 stands at 1.10.