Key views Global Monthly May 2024

Growth indicators are bottoming out in the eurozone and China, while the US economy is gradually cooling. Big picture, the global economy is slowly converging towards a more trend-like pace of growth, and this remains our base case for the second half of 2024. Global trade and industry are beginning to recover, but a sharp rebound is unlikely while rates remain restrictive. On the positive side, inflation has fallen significantly, although progress towards the 2% target has slowed in the US. The impact of the conflict in the Middle East has receded and the inflation impact is likely to be minimal. Further falls in inflation will enable central banks to pivot to rate cuts by mid-2024, and financial conditions have eased in anticipation of this. Still, interest rates will stay high for some time yet, and this will keep a lid on the recovery.

Macro

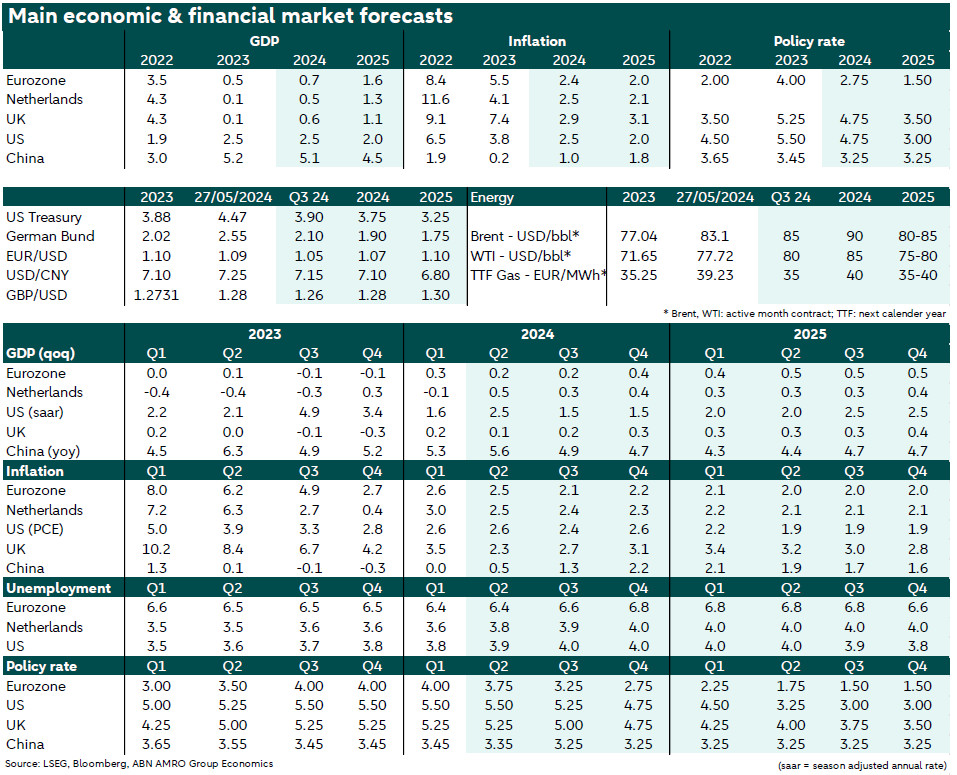

Eurozone – Q1 GDP for the eurozone came in above expectations (+0.3% qoq) ending a 5 quarter period of roughly stagnation. This provides cautious room for optimism about the bloc’s economic performance this year. As growth was driven by some one-offs, Q2 activity is likely lower. Growth should expand moderately during the rest of the year, as trade and industry bottom out, which will support EZ exports. Domestic spending is expected to increase on the back of high wage growth and lower inflation but deteriorating labour market conditions and fiscal retrenchment prevent a strong recovery.

The Netherlands – First quarter GDP showed an unexpected contraction of 0.1% qoq. We have revised our growth forecasts to 0.5% in 2024 (was 0.7%) and 1.3% in 2025 (was 1.2%). Growth will be driven by internal demand from households and the government. Later in 2024, as financial conditions ease and external demand increases, growth will pick up further. Inflation is continuing its downward trend. Although the price trend of products with a large wage component – such as labour-intensive services – cause the path down to take longer. We expect inflation to average 2.5% in 2024 and 2.1% in 2025.

UK – Disinflation is continuing, providing some relief to the Bank of England, but upside inflation risks remain significant given that wage growth is still elevated and well above levels consistent with the 2% target. The economy is recovering from a prolonged period of stagnation, having been weighed by high rates and weak confidence. Wage growth is coming down, which should help to bring down services inflation. But the normalisation in inflation may take longer in the UK than in other advanced economies, due to historically higher inflation expectations, and stickier wage growth.

US – Following a surprisingly low growth reading in Q1 of 2024 on the back of higher imports, we expect a reversal with above trend growth for Q2. Still, weak bank lending and pockets of financial stress among households are likely to contribute to a slowdown in growth in the second half of the year, before returning to trend next year. Inflation has come in on the firm side in recent months, but pipeline pressures – particularly benign wage growth – continue to point to disinflationary progress resuming over the coming months.

China - Divergence remains between strong supply and weak domestic demand, dragged down by real estate woes. Partly on the back of improving external demand, industrial production remains solid. Still, China’s overcapacity leads to a broadening of trade spats with the West. Meanwhile, Beijing started a new approach to break the negative feedback loop in property – by facilitating local governments to buy homes from developers and turn them into affordable housing. While it is uncertain whether these measures will bring a ‘quick fix’, they signal an increasing sense of urgency to tackle the biggest macro drag.

Central Banks & Markets

ECB – The ECB is expected to start cutting rates in June, in a widely telegraphed move. The ECB has said that if the inflation outlook, underlying inflation and the strength of monetary policy transmission were according to expectations, it would be appropriate to cut the policy rate. We believe these three conditions have been largely met already. ECB officials have so far played down expectations of a follow-on July cut, reflecting a general tendency to avoid forward guidance. Our base case sees rate being cut at each meeting after June, for a total of 125bp rate cuts in 2024.

Fed – We expect rate cuts to start in July, with a pause in September as the Fed waits to gain confidence in the inflation outlook. We expect consecutive rate cuts from November on. Hawkish Fed communication suggests the start of the easing cycle will be delayed in case of upside surprises to inflation this quarter. Monetary policy is expected to remain restrictive throughout 2024 and into 2025. We expect the upper bound of the fed funds rate to reach 4.75% by end-2024, and 3% by end-2025. Starting in June, the Fed will reduce the pace of QT, which has no implications for its monetary policy stance.

Bank of England – The MPC has kept policy on hold since last August. We think Bank Rate has peaked at 5.25%. The BoE is in full data-dependent mode, and UK macro data has been erratic over the past year. Our base case continues to see the BoE starting to cut rates in August. However, sticky wage growth – which poses upside risks to medium-term inflation – is likely to keep rate cuts at a more gradual pace than for the ECB and Fed; we expect only two rate cuts (total 50bp) in 2024, and four rate cuts (total 100bp) in 2025.

Bond yields – Uncertainty about the number and timing (at least for the Fed) of rate cuts remains the key driver for markets. Recent macroeconomic data has once again reduced the number of cuts priced in for this year. However, our view remains that rates will fall going forward as we expect markets to reprice the estimated terminal rate lower once rate cuts start. The ECB is widely expected to start first (in June) and is likely to trigger such a move. Downward pressure is expected particularly on short-term rates, leading the yield curve to steepen in the second part of the year and beyond.

FX – EUR/USD has been rangebound. EUR weakness from current levels will materialize in the coming months as long as the cut expectations on the ECB run ahead of rate cut expectations of the Fed. As soon as the Fed begins the easing cycle and markets start to anticipate a larger number of rate cuts in 2025, the dollar will probably decline. Our forecasts for Q2 and Q3 are 1.05 and for year-end 1.07. Our forecast for end 2025 stands at 1.10.