Key Views Global Monthly May 2026

The Iran conflict has triggered a new global energy shock. It remains uncertain how long the disruptions to energy supplies will last, but our base case assumes severe disruptions last well into Q3. The inflation shock is outweighing the growth shock, and this is leading to a hawkish pivot by central banks. The ECB is expected to hike rates while the Fed is expected to delay further rate cuts. Still, advanced economies are expected to stay resilient and to avoid recessions, and ultimately we expect central banks to lower rates again once the inflation shock has dissipated. Against this backdrop, US tariffs remain a dampener on global trade, but the AI boom is continuing, German fiscal spending is driving a cyclical eurozone recovery, and China continues to take modest measures to lift demand while keeping its manufacturing growth model intact.

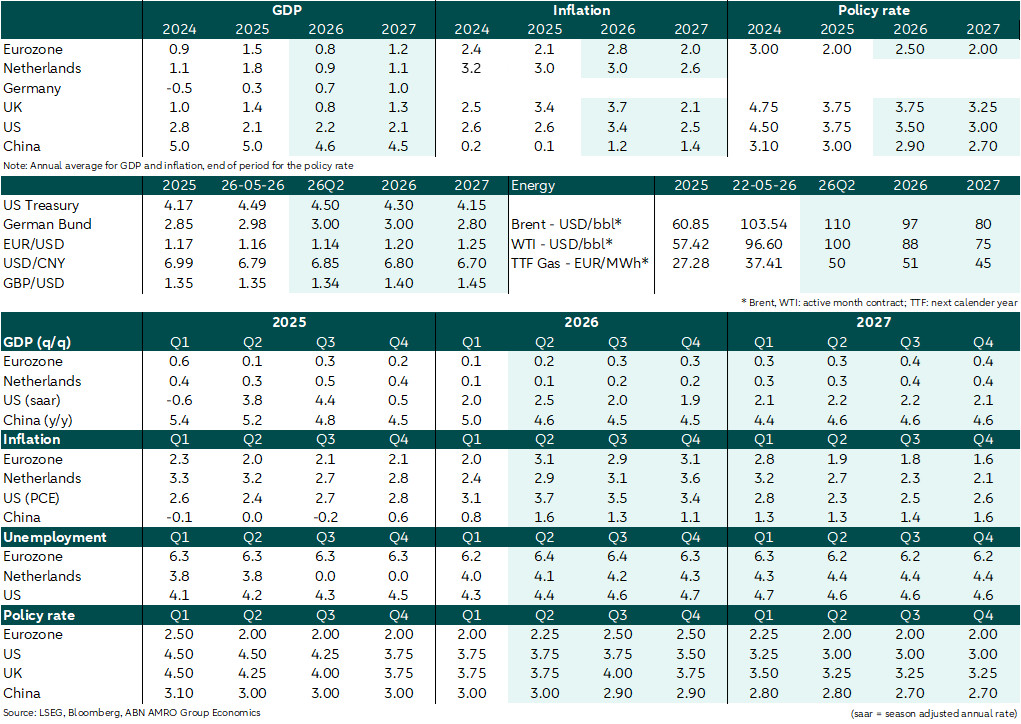

Macro

Eurozone

The inflation jump from the new energy shock will outweigh the hit to growth. However, we expect a much narrower and manageable rise in inflation compared to the 2022-23 shock. This is because the magnitude of gas price rises is much lower, but also because electricity markets have largely decoupled from gas. Still, because the ECB will need to get ahead of any second round inflation effects, growth will be dampened by a tightening of financial conditions. At the same time, the cyclical recovery is expected to broadly continue, helped by higher German fiscal spending.

The Netherlands

On the back of a lacklustre start of the year, with GDP growth slowing to 0.1% q/q, and our new Iran scenario, we downgraded our growth forecasts to 0.9% for 2026 and 1.1% for 2027. Still, the Dutch economy is resilient, in part because of recent economic momentum and because the private sector deleveraged and built considerable buffers. Our HICP forecasts have been upgraded on the back of expected persistence of elevated energy prices. The Dutch economy is prone to second-round effects on wages due to the starting point of inflation and the tight labour market.

UK

The energy shock is leading to a new inflation surge at a time when inflation expectations are already unanchored. Still, the labour market is much looser than it was when the last energy shock hit, and this should help to contain second round effects. The growth impact is expected to be manageable, and our base case sees the economy continuing to gradually recover. Uncertainty over the leadership could start to weigh on growth in the event of a prolonged contest. See our Q&A on the UK’s political turmoil here for more.

US

The final quarter of 2025 saw some stalling momentum, partly due to the government shutdown, while the first quarter of 2026 was solid, even if mostly AI-driven. The recent oil shock increases inflation but has a limited impact on growth. We still expect decent headline growth figures due to the positive impulse of AI investments, and monetary and fiscal easing. Core inflation remains elevated, due to the final pass-through of tariffs, demand effects from stimulus, and spillovers from energy inflation. Unemployment continues a gradual increase, with limited demand matching the strong decline in supply.

China

Despite foreign trade remaining solid on the back of the global tech/AI boom, the economy is not immune (though cushioned) to the Iran conflict. April data showed quite a broad weakening. Producer price inflation has risen sharply, but (core) CPI inflation remains low reflecting weak domestic demand. We keep our growth/inflation forecasts unchanged for now, after having tweaked them in March. A slowdown in global demand still is the biggest risk from the conflict. The recent Trump-Xi meeting helps to stabilise US-China relations, with their tariff/chokepoint truce extended. Still, risks related to trade, tech and wider geopolitics (incl. Taiwan) remain.

Central Banks & Markets

ECB

The Governing Council has shifted to a tightening bias, and we expect rate rises at the June and July meetings, taking the deposit rate to 2.50%. Lagarde herself sent a strong signal that June would be a good moment to adjust policy. The tightening bias is further supported by the recent rise in longer term inflation expectations. Ultimately, we expect second round effects to be contained, and by early 2027 we expect the ECB to be confident enough in the inflation outlook to gradually bring rates back to its estimate of a neutral policy setting. We expect one rate cut each in Q1 and Q2 2027, bringing the deposit rate back to 2%.

Fed

The Fed held rates at the 3.50-3.75% target range in the April meeting. They signalled that the FOMC saw no consensus to ease before goods (i.e. tariff) inflation starts to abate. With the added impact of the oil shock on energy and headline inflation, we expect the Fed to remain on hold for longer than previously anticipated, waiting until December to convince themselves of limited second round effects. We then see a dovish Fed gradually easing, despite elevated headline, and elevated core inflation, with quarterly 25bps cuts to end up at 2.75-3.00% by the June of next year, the lower end of neutral estimates.

Bank of England

The MPC has struck a more dovish tone following its hawkish communication at the March meeting. We still expect the BoE to do an insurance rate hike over the summer, but with a lower conviction. Ultimately we expect the MPC to pivot back to a wait-and-see approach, assuming energy supplies gradually normalise in Q3. This reflects that rates are already in restrictive territory, and the MPC’s historically volatile but ultimately dovish bias. We expect rate cuts to resume from late 2026 onwards.

Bond yields

The ongoing uncertainty in the Middle East has intensified concerns about inflation due to the significant decline in oil supply. As a result, bond yields increased further, with the market pricing in more than two rate hikes by the ECB and nearly one by the Fed for this year.As the market anticipates more rate increases in both Europe and the US compared to our base case scenario, we expect yield curves to re-steepen again, driven by the short end. Meanwhile, LT rates will lag the decline in front end yields, owing to increased term premiums caused by the deteriorating fiscal situation.

FX

EUR/USD has moved volatile within a range depending on optimism about reaching an agreement to reopen the Strait of Hormuz. Even if a deal is reached, we think will take time for the supply to normalise. Therefore, we think oil prices will remain elevated. It is likely that this will weigh on EUR/USD in the coming months as the euro is dependent on energy imports. So, in the near-term EUR/USD could move towards 1.14. Later in the year we expect lower energy prices. This and a more hawkish ECB compared to the Fed should support EUR/USD higher. We still expect the EUR/USD rate to be 1.20 by the end of 2026.