Macro Watch - Well, that de-escalated quickly

This morning, China and the US announced a significant de-escalation in the trade war, bringing the bilateral tariffs of 145% (on Chinese exports) and 125% (on US exports) down to 30% and 10% respectively.

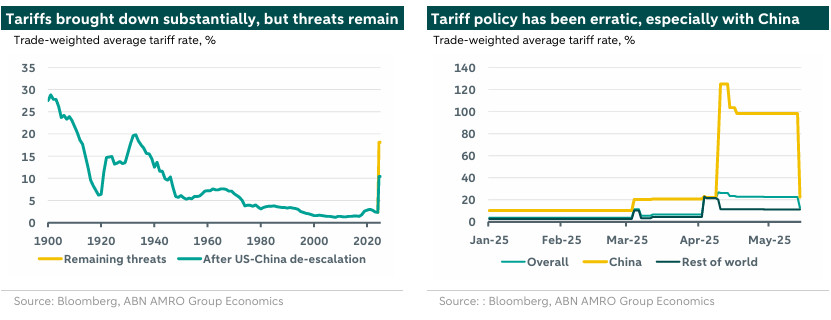

After weekend talks in Geneva, the US and China announced a significant de-escalation of the tariff war, exceeding expectations

For the next 90 days, instead of 145%, China faces the 10% baseline + 20% fentanyl-related tariffs, with no further reciprocal tariffs

Instead of 125%, the US faces 10% tariffs on exports to China

Last Thursday, the US and UK also reached a trade agreement that predominantly limited downside risks

The trade deals set the tone for the EU – 10% is likely a floor

We expect to modestly raise our growth forecasts

Tariff rates came down a lot, but they’re still substantial

This morning, China and the US announced a significant de-escalation in the trade war, bringing the bilateral tariffs of 145% (on Chinese exports) and 125% (on US exports) down to 30% and 10% respectively. The 30% tariff encompasses the liberation day package universal rate of 10% and the 20% fentanyl-related tariffs but excludes the various section 232 sector-specific tariffs, as well as any tariffs at the start of the year. All combined, this lowers the US average tariffs on China from well over 100% to around 40%, while the total trade weighted average tariff rate on US imports drops to slightly above 10% from over 20% before the weekend. A decoupling is averted for now, limiting downside risks to both economies, and reducing the risk of an extended supply shock in the US. Still, both the China and overall tariff rates are four times higher than they were at the start of the year, which continues to exert negative pressure on especially the US economy, although by less than the policy in place before the weekend.

In addition to the agreements made this weekend, the US and China established an economic and trade consultation mechanism, that allows the two countries to continue their negotiations. This will be necessary, as this agreement merely reflects a pause, not a cancellation. One may recall the 30-day pause Mexico and Canada faced on their tariffs and the chaos at the end of those periods. With that said, both parties will want to continue negotiations. China will be looking to remove the final fentanyl tariffs, while the US will continue to seek a lift of the export restriction on rare earth minerals. Communication has been notably absent on that last part, although China has pledged to move towards cancelling non-tariff barriers put in place since April 2nd, which likely refers to those exact export restrictions.

China: 90-day truce will soften biggest drag on economic growth for now

Following the sharp escalation of the bilateral tariff war between the US and China in April, we adjusted our quarterly growth profile to reflect this and lowered our annual growth forecasts for 2025 and 2026 further to 4.1% (from 4.3%) and 3.9% (from 4.2%), respectively. We noted that big exemptions (e.g. for consumer electronics, car parts) would mitigate the direct export shock to the US, while trade circumvention (e.g. transshipments to the US via South East Asia, also see our recent global trade watch on frontloading here) and trade reorientation/diversification - combined with some ‘tariff dodging practices’ - would make China’s total export shock even smaller than the direct shock. And indeed, China's monthly export data for April show that direct exports to the US were down by around 20% m/m, but this was largely offset by a rise in exports to ASEAN and the EU. What is more, container flow data from China to the US have shown a pick-up in May so far, after having nosedived in the course of April. We also expected Beijing to continue with monetary easing and adding fiscal support, to soften the blow from the tariffs shock (see for instance here).

All in all, the sharp (temporary) reduction in bilateral tariffs as mentioned above, will take away the biggest drag for the Chinese economy in the coming quarters. This would also imply that Beijing will likely shift to a lower gear in terms of adding additional support. All in all, we see upside risks to our growth forecasts rising at the moment. We will publish an update later this month.

US-UK trade deal is no game changer, but limits downside risks

Last Thursday, the US also announced an outline deal with the UK (). Two key elements stuck out to us. First, a big concession from the UK is that it tacitly endorsed the 10% baseline tariff, which remains in place and with no mention of any prospect of it being removed. Second, the US lowered its new 25% tariff on cars to the 10% baseline rate subject to a 100,000 annual quota on imports from the UK. This figure is around the current level of UK car exports to the US. In return, the US received vague promises on market access for US agriculture (with the US acknowledging that the UK would not be forced to change its food standards), and more concretely, a removal of the 19% tariff on US ethanol up to a quota of 1.4bn litres (far higher than current US ethanol exports, but valued at $700mn, is less than 1% of total US exports to the UK in 2024). Notably absent from all of this was any changes to the UK’s digital services tax, which will remain in place, as well as VAT which had been previously called a trade barrier by the US. UK Prime Minister Starmer remarked that the deal would ‘boost trade’ between the two countries, ignoring the fact that in the aggregate, US trade barriers are much higher now than they were a couple of months ago. Our view is that the deal reduces the downside risks, but that there will still be a hit to UK exports to the US under the 10% baseline tariff. This will dampen growth over the coming quarters, though to a lesser degree than if the full 25% car tariff had gone ahead.

What does all of this mean for the eurozone?

We see three main takeaways of all of this for the eurozone. First, with the China-US de-escalation, there is now likely somewhat less of a global demand and supply shock, and a reduction in the negative spillover effects that would have entailed. Second, there is also less risk from a dumping of Chinese goods into the EU market, with US-China trade likely to rapidly resume over the coming months (even if trade volumes don’t fully recover given still-high tariffs). These two factors should reduce the growth impact, as well as the near-term downside risks to inflation.

Third, the UK-US deal likely offers a template for a future EU-US deal. Most notable here is that the US seems determined to keep a 10% baseline tariffs come what may, with the negotiations therefore centred around the threatened 20% higher ‘reciprocal’ and other higher tariffs, such as on cars and steel & aluminium. We think it is likely the US will strike a similar deal with the EU as it did with the UK, to: 1) not raise the reciprocal tariff to 20%, and 2) implement quotas for car imports at 10%, likely in return for a mixture of vague and concrete EU promises to expand market access for US exporters. This is likely to focus more on expanding LNG imports, something that the EU wants to do anyway as it approaches a 2027 deadline to fully end its reliance on Russian energy, but we expect vague promises similar to those made by the UK to improve market access for US agriculture.

Will the EU accept the 10% baseline tariff remaining in place?

EU trade commissioner Šefčovič was asked directly by thewhether the EU would accept 10% as the floor on US tariffs, to which he responded that 10% was a ‘very high level’. We take this to be an expression of grievance while also not ruling out the EU accepting such an outcome. The EU has a lot more negotiating heft with the US than does the UK, but at the same time, there seems little appetite to get embroiled in an escalating trade war with the US, particularly among some key countries like Italy and Spain. As such, we would have as our base case that the EU would reluctantly accept the 10% baseline tariff as a least-worst outcome. All in all, the de-escalation is likely to somewhat dampen the growth shock to the eurozone from US tariffs, but it will not eliminate it. We plan to update our forecasts later this month.