May flash PMIs - Widening gap between manufacturing and services

Flash PMIs for both the US and the eurozone point to a widening divergence between manufacturing and service sector performance.

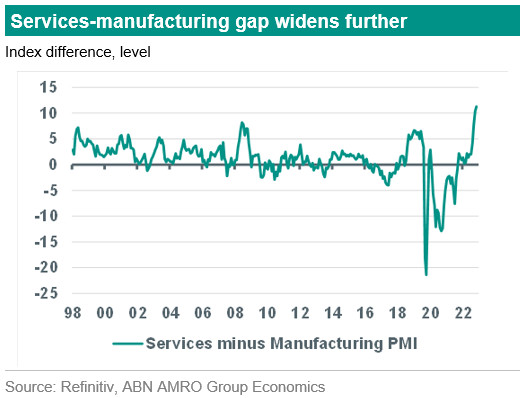

Gap between Manufacturing and Services PMI widens further

The flash estimates of the eurozone PMIs for May showed a further widening of the gap between the Manufacturing PMI and the Services PMI. The Manufacturing PMI staged another drop in May, falling to 44.6, down from 45.8 in April. The Services PMI declined more moderately, to 55.9 from 56.2. As a result, the composite PMI fell to 53.3 from 54.1, which was in line with our expectations. The gap between the Services and Manufacturing PMIs, which already reached an unprecedent high level in April, increased further in May. This exceptionally large gap between the two PMIs suggests that the normal cyclical drivers of activity in the two sectors are still disrupted, for instance by the post-pandemic normalisation in certain parts of services. Having said that, only activity in the art, entertainment and recreation category (with a share of 4% in total services) has not yet returned to the pre-pandemic level. In most other parts of services, activity has already fully recovered and returned to the pre-pandemic trend. Although the level of the services PMI during the past few months would be consistent with high growth in the sector, we estimate that actual activity in total services grew by only around 0.0-0.2% qoq in Q1, based on the monthly data that have been published for activity in manufacturing and construction and total GDP in Q1. This implies that the high level of the Services PMI is somewhat more sentiment driven than in the past.

All in all, we think that recent changes in the Services and Manufacturing PMIs and their current levels still are consistent with our view that the eurozone economy is cooling on the back of past and upcoming interest rate hikes by the ECB, the end of the post-pandemic catching up effects in certain parts of services and the weakening of global growth and world trade. We continue to expect moderate declines in GDP during the rest of the year. (Aline Schuiling)

US PMIs a mixed bag that is difficult to interpret

Flash PMIs for May suggested a weakening in the manufacturing sector – which dropped back below 50 to 48.5 – but a strengthening services sector, with the PMI rising to a 13 month high of 55.1. This led to a rise in the composite PMI to 54.5 from 53.4 in April. While pointing to a pickup in growth momentum in May, we must add the caveat that the PMIs have been unreliable predictors of activity in recent quarters – bordering on being contrarian indicators: in the second half of 2022 they were pointing to contractions in GDP, but GDP grew at well above trend rates (the opposite was the case in the first half of 2022). Meanwhile, there were signs of significant weakness below the surface of the May report: new export orders for manufacturing fell back to near the post-pandemic low of 43.8 while the new orders index dropped to 47.2. Indeed, similar to the eurozone, there is a widening gap between the manufacturing and services PMI, although not as historically big.

We put more weight on activity data in the current environment

Overall, we judge that it is difficult to take a clear signal from the PMIs given their poor track record over the past year. As such, we continue to put more weight on activity data in judging where we are in the cycle – this points to a clear slowdown in activity following the above-trend growth of H2 2022. For instance, the weekly Redbook retail sales data (also released today) suggests retail volumes are contracting on a y/y basis. (Bill Diviney)