Steady ECB rates as far as the eye can see

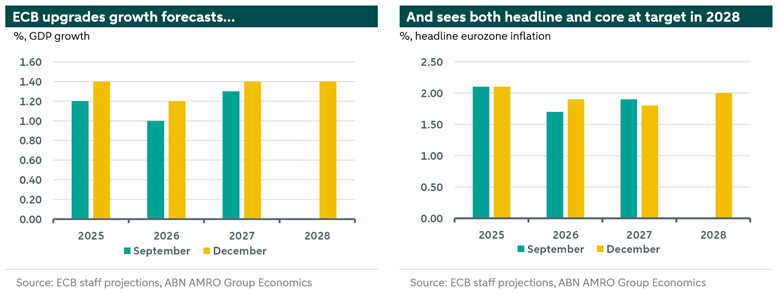

The ECB kept its key policy rates on hold as expected at the December Governing Council meeting. In the press conference following the decision, President Christine Lagarde repeated that the ECB was in a ‘good place’ with regards to interest rates, but also that this does not mean that the policy would be ‘static’. Indeed, the Council continued to signal that it would ‘follow a data-dependent and meeting-by-meeting approach to determining the appropriate monetary policy stance’. However, with economic growth revised up in the projections and inflation (especially stripping out energy prices) broadly seen on target, a rate change in either direction does not seem on the cards anytime soon, absent of a new shock. Indeed, we expect the ECB to keep its deposit rate at 2% in the coming months.

The ECB’s confidence in the economic recovery rests on ongoing strength in domestic demand. This rests on positive drivers of consumer demand on the one hand (real incomes and an expected decline in the savings ratio) and investment on the other (business investment and substantial government spending on infrastructure and defence). Domestic demand also supported growth in third quarter, and the ECB noted that the other side of that was strength in the service sector, especially in the information and communication sector. Indeed, Lagarde noted that survey evidence suggested that corporate investments in AI were an important driver in these trends.

Inflation is expected to fall below target in 2026 and also in 2027. However, this is not seen as a reason to respond with interest rate cuts. First of all, the undershoot is not large. Second it reflects a drags from energy prices. Indeed, excluding energy prices, inflation is either above or at target on average over the coming years. Third, inflation is expected to return to target in 2028.