SustainaWeekly - ESG ratings can add value over and above credit ratings

We show that ESG ratings have a modest positive correlation with credit ratings in the case of MSCI ESG ratings, but not of those from Sustainalytics. This MSCI correlation seems to be better when looking at high-yield (HY) companies. The fact that we find a correlation with MSCI ESG ratings, but not Sustainalytics, could be explained by the fact that MSCI puts more weight on governance factors, as credit ratings are usually focused on the ‘G’ pillar. We argue that screening companies for better ESG prepositions could add a new dimension for credit assessments and ultimately act as an important tool for bond investors to identify companies that have a better credit quality.

ESG factors can affect a company’s cash flows and therefore, the likelihood that it will default on their debt obligations. Besides numerous research studies confirming this, the point is also set out by the UN PRI (Principles for Responsible Investment) as one of the reasons why investors should incorporate ESG into investment decisions (see ). As credit ratings are ultimately an estimate of a company’s ability to fulfil financial obligations and reflect therefore its probability of default, one could assume that ESG factors are also incorporated into credit rating assessments. Is this the case in reality, though?

Relationship between ESG ratings and credit ratings

In order to investigate the inclusion of ESG factors into credit ratings, we make use of ESG ratings as a proxy for how a company performs with respect to ESG factors. MSCI ESG ratings, for example, “aim to measure a company’s resilience to long-term, financially relevant ESG risks”. Similarly, Sustainalytics’ ESG ratings “measure the degree to which a company’s economic value is at risk driven by ESG factors” (see ). Hence, a company that either has low exposure to material ESG factors, or manages them well (or both), will have a higher ESG rating.

If a company is less likely to have its firm value reduced due to ESG factors (that is, it has high ESG rating), then one could also expect it to have a higher credit rating (all else equal). For that analysis, we have looked at MSCI and Sustainalytics as ESG rating providers, and Moody’s and S&P as credit rating agencies – in both cases, due to the large universe of rated companies by these institutions. We have converted Moody’s and S&P ratings to numerical scores, with each rating class separated by 5 (this means that an AAA (S&P) / Aaa (Moody’s) rated company receives a score of 100, an AA+ (S&P) / Aa1 (Moody’s) company receives a score of 95, etc). For MSCI ESG ratings, which are also given in alphabetic form, we have converted it to numerical scores separating each class by 15 (AAA rating is a score of 100, AA rating is a score of 85, and so on). Sustainalytics’ scores were also rounded to the nearest 5 to ensure less variability (this did not affect our final results). Our analysis universe involves both, corporates and financial institutions, although we will use the term “company” going forward for simplification purposes. We do not limit our analysis to EUR issuers. This allows us to have a big sample universe, with around 1,000 observations per ESG rating provider.

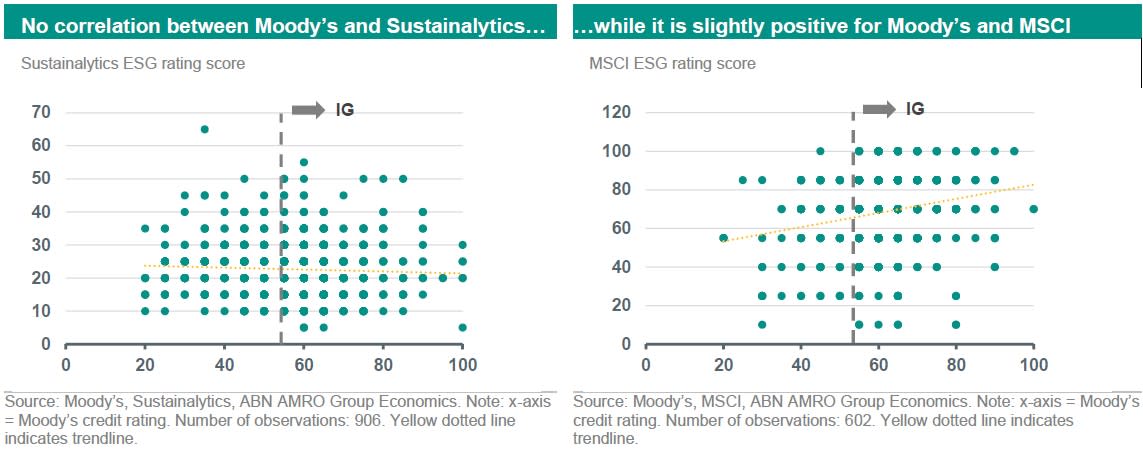

Let’s first look at Moody’s. The charts on the next page show the relationship between Moody’s credit ratings and both, Sustainalytics and MSCI ESG ratings. At first sight, we see a big dispersion between credit ratings and ESG ratings: for example, a Baa2 company can have a Sustainalytics’ ESG rating ranging from 5 (negligible risk) to 55 (severe risk). Same is true when also looking at MSCI ratings. However, MSCI ratings seem to have a higher correlation with Moody’s credit ratings than Sustainalytics’. And indeed, as shown by the trendlines on the charts below, there seems to be a small positive correlation between MSCI and Moody’s, while there is no correlation at all when looking at Sustainalytics. And indeed, the correlation between Moody’s and Sustainalytics stands at nearly zero (-0.05 to be more precise), while for MSCI this is 0.2. Moreover, the positive correlation between MSCI and Moody’s also makes sense: a company that performs better in terms of ESG, is, for example, exposed to less litigation risks, transition risks, governance risks etc, which could imply a lower probability of default and therefore, a better credit rating.

We have also analysed whether our conclusions change if we look at exclusively Investment Grade (IG) or High Yield (HY) issuers. This however does not seem to be the case. On the other hand, the correlation between Moody’s credit ratings and the MSCI ESG ratings seems to be slightly higher for HY companies (0.2 for HY and 0.1 for IG). HY issuers are usually less transparent and/or lack in the quality of their disclosures, which can impact both, the ESG and the credit assessments. Furthermore, HY issues usually have short or inconsistent track records and management turnover, which can affect assessment of management quality, which is also an input for both, ESG and credit ratings. Another point is that some HY companies have complex ownership structures and/or high ownership concentration (that is, more control of the board of directors by the owner), which could be driven by their higher risk tolerance. Lack of ownership independence also usually weights into both, ESG and the credit quality assessments. That could explain why we also find a higher correlation between MSCI ESG ratings and credit ratings for HY issuers.

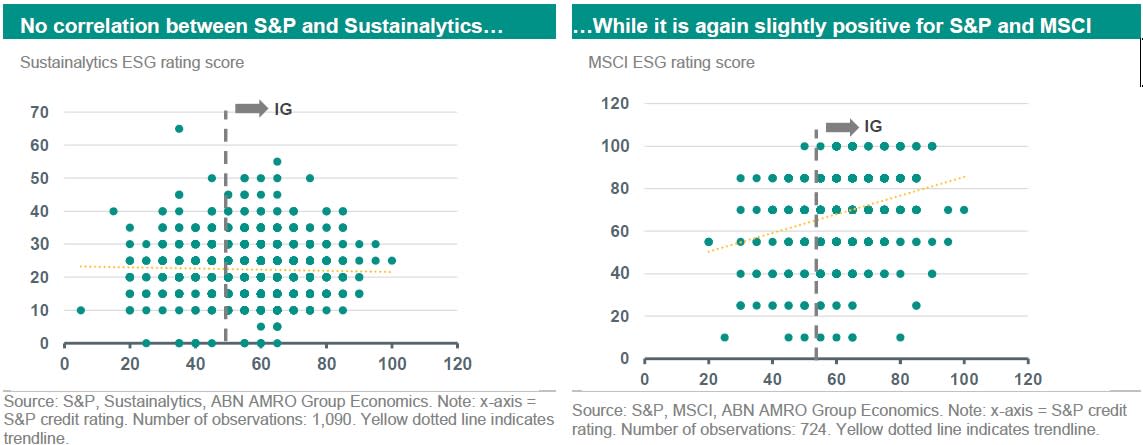

Looking at S&P credit ratings our conclusions are the same. There is no relationship between S&P and Sustainalytics ESG ratings, but we do find a positive correlation with MSCI. S&P credit ratings correlation with Sustainalytics stands at nearly zero (-0.04), but this is 0.3 for MSCI. Hence, there seems to be a stronger correlation between MSCI and S&P ratings than between MSCI and Moody’s ratings. Also when considering exclusively IG or HY companies, we see a stronger correlation between MSCI ratings and S&P ratings considered as HY (correlation of 0.2 vs 0.1 for IG issuers). Again, correlation with Sustainalytics ESG ratings are zero, independent of the credit rating threshold.

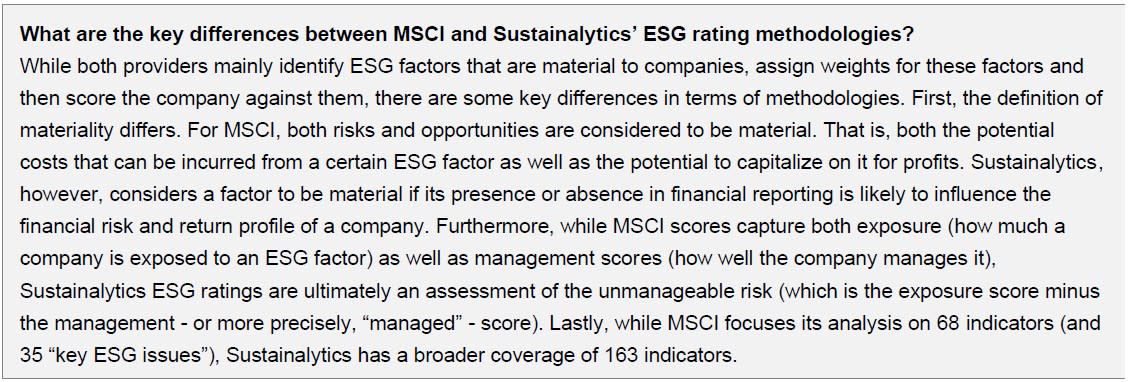

One reason that could explain why we only see a relationship between MSCI ESG ratings and credit ratings, is that perhaps MSCI puts more weight into governance factors than Sustainalytics does (see our box at the end of the piece for more details on the differences in methodologies). Credit ratings are usually more focused on governance factors, as some argue that weak governance translates into higher downside risks (as in, bankruptcy risks and therefore the ability of companies to pay back debt) than environmental and social aspects. In that case, fraud prevention and good governance are seen as better protectors against negative credit events, and are therefore more explicitly incorporate into credit analysis. This could also explain why we see a stronger correlation between HY credit ratings and MSCI ESG ratings, as HY companies have a history of performing worse in terms of governance than IG ones. Their smaller size also puts them on the backfoot in terms of strong governance systems versus a large investment grade company.

It is important to note that credit rating agencies have only recently started to incorporate ESG aspects. It was mostly only after 2016 that they started to look at a range of ESG factors to judge companies’ ability to reply to ESG risks and assess how these could have potential financial impacts. Hence, while credit ratings are still mostly focused on governance, it could be that as methodology develops, these agencies also start to look more exclusively at the ‘E’ and ‘S’ pillars from a downside risk perspective, rather than opportunity one, which seems to be the focused at the moment. Overall however, the fact that we find none (in the case of Sustainalytics) or very low (in the case of MSCI) correlation between ESG ratings and credit ratings highlights that the latter does not seem to fully capture ESG risks. That implies that ESG incorporation into investment decisions can add a new dimension for investors when assessing the credit quality of a company.

Small correlation between MSCI and Sustainalytics

The difference in results when looking at MSCI and Sustainalytics triggered us to also investigate to what extent MSCI and Sustainalytics’ ratings are correlated. An analysis from our sample allows us to see that there is almost no correlation between MSCI and Sustainalytics’ ESG ratings (see table below), while Moody’s and S&P have an extremely high correlation (of almost 1). And even more interesting: there seems to actually be a negative correlation between MSCI and Sustainalytics, of -0.3. That means that a company that scores very well in terms of ESG according to Sustainalytics, could actually score poorly according to MSCI. This negative correlation seems to be more apparent for IG companies.

The above shows why our conclusions have been very similar independent of when considering S&P or Moody’s as credit ratings, but have however yielded different results when looking at MSCI or Sustainalytics. A study by Berg et. al (see ) has shown that when taking into account only the governance dimension of these two ESG ratings, the correlation is even lower. The study shows that while on the environmental and social pillars, MSCI and Sustainalytics have a correlation of 0.37 and 0.27, respectively, this is only 0.16 for governance. Hence, once again, this reinforces our view that it is likely due to MSCI’s higher weight on governance factors compared to Sustainalytics, that explains the fact that only MSCI seems to be somehow correlated with credit ratings.

The very (negative) correlation between MSCI and Sustainalytics also allows us to conclude that while incorporating ESG into investment decisions can add a wider dimension to credit analysis of companies, in practice, the different approaches and hence, different views on the ESG profile of a company by different ESG providers should also make this process difficult to apply in practice.

Investors can use ESG to find companies with a better credit quality

Overall, this could prove to be an important factor of consideration for investors. If credit investors are mostly focused on a company’s ability to repay debt, whose likelihood is gauged by the credit ratings, a company which has a good MSCI ESG rating, or one which has just been upgraded to a higher rating, could also eventually prove to have a better credit quality. High ESG-rated companies are also usually more transparent, in particular with regards to their (ESG) risk exposures. They also have a better risk management and good governance standards, and all this should translate as well into a better credit rating, even if only in the long-term. We therefore show that besides financial implications from investing in ESG bonds (such as higher “greeniums” driven by high demand from dedicated ESG funds), credit investors could also add to the list the fact that better ESG-positioned companies (proxied by MSCI ratings) can also develop a lower probability of default. Investors should also therefore take into account the relationship between ESG factors and the financial impact it can have on companies.

This article is part of the SustainaWeekly of 21 November 2022