Green bond impact not resonating in real estate credit

EUR IG residential real estate bond issuers have all started publishing their green bond impact reports, which showcase the energy demand and carbon emission in the properties allocated to green financing. This allows for a comparison against the climate credentials of the overall issuer real estate portfolio, but also benchmarking amongst the issuers. German bellwether Vonovia/Deutsche Wohnen achieves the largest reduction from the regular portfolio. Finnish residential real estate issuers Kojamo and Sato have better starting points in terms of energy use and emission against German and Dutch names, which is remarkable given the harsher weather conditions in their operating region. However, the bond market (or green bond investors specifically) seem to assign zero weight to the superior profile of the green assets, as none of the underlying green bonds trades at tighter credit spreads.

Green bond investors are looking for climate impact in terms of the assets they specifically finance. The real estate sector, which has strong decarbonization objectives, should therefore find strong appetite at green bond investors looking for impact. Previously, we have indeed shown that in secondary market many real estate bonds trade at a lower spread than their non-green equivalents. Although the market for real estate credit has incurred significant spread widening, we would have expected that green bond investors would stick to their principles for a stronger bid, especially now that issuers can clearly demonstrate the climate superiority of the assets they have put-up for finance under the green bond. By looking specifically at the residential real estate part of the market, since all the issuers in this segment that have printed EUR green bonds have published allocation reports, we try to figure out whether this higher bid still holds.

The EUR green bond residential real estate universe is small, only comprising four issuers being Vonovia (largely Germany - Vonovia recently acquired Deutsche Wohnen), Vesteda (Netherlands), Kojamo (Finland) and Sato (Finland). Still, we do note that some form of consistency is being applied across residential real estate issuers in the sense that the measurement of energy usage and emissions also spans tenant scope. There might be some differences in approach, such as the fact that tenant electricity usage is not included in the energy and emission numbers published by Vonovia. While the Finish operators have managed to proceed to live tracking of energy usage at their tenants, Vonovia and Vesteda calculate energy and emission impact on the back of energy labels. The table below shows a summary from the latest published green bond allocation reports and issuer 2021 sustainability reports.

Clearly the Vonovia green bond holder achieves the largest impact in comparison to the regular Vonovia bond holder. Energy intensity and emissions sit roughly 60% lower than at overall company level, and in the case of its recent Deutsche Wohnen acquisition, the green bond properties emit nearly 65% less CO2 per square metre (sqm). When we extrapolate the 24.6 KWh per sqm tenant electricity usage as reported by Dutch peer Vesteda (since Vonovia does not report on electricity), the energy usage on green bond assets rises from 64 KWh per sqm to 85 KWh per sqm. This would still imply a 54% lower intensity than at regular bond level, which again reflects much more impact than at the other issuers.

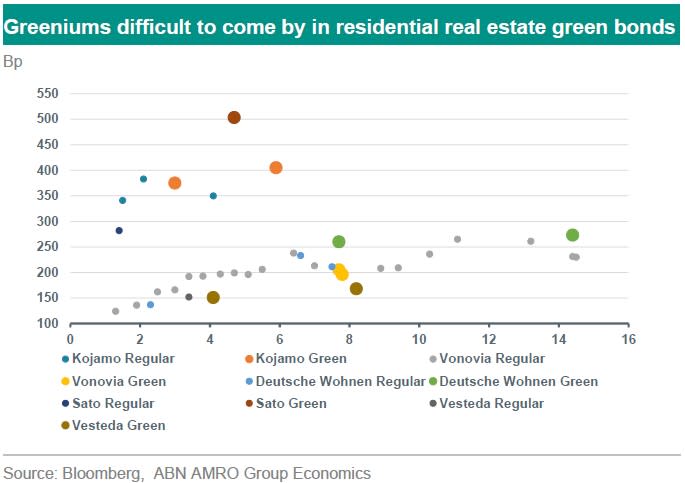

Despite data showing lower emissions, greeniums are difficult to come by

We highlighted the superior energy intensity and carbon footprint at Vonovia, but this feature is also available across all issuers, as one would expect. Hence, if the green bond is funding assets with better climate impact, even if the difference only amounts to 5% as reflected in the case of Kojamo, the green bond holder should be willing to pay up. The chart below shows that this is clearly not the case and in some cases we are even seeing green bonds trading at wider credit spreads today. The best example is the Deutsche Wohnen 0.5% 2031 green bond which trades at 20bp pick-up to the Deutsche Wohnen 2031 1.625% regular bond. Valuations should speak in favour of the green bond, given the huge difference in energy usage and emissions to company level.

Green bond valuations in the Finnish names are also off-course. The Kojamo 2% 2026 green bond trades at 25bp of pick-up to the Kojamo 1.875% 2027 regular bond, despite featuring a 1y less in duration. In the case of Sato, the 1.35% 2028 trades at the highest (222bp) spread steepness in this universe to its shorter dated equivalent non-green bond, being it the 1.375% 2024. Such steepness is not visible at similarly BBB2 rated Kojamo, while Sato on a stand-alone basis reports lower ND/EBITDA (12.6x) than Kojamo (14.3x), according to the latest rating agency adjusted financial metrics. Presumably the Sato bonds are still reeling from the negative credit outlook issued at parent company level, although this has been recently revised back to stable. Clearly, investors have pushed ESG features on this bond to the backburner.

Finally, we see a flat credit term spread between the Vesteda 2% 2026 non-green and the Vesteda 1.5% 2027 green bond. But this does not seem to be driven by the green label of the 2027 bond, since we see similar flatness in term premia on Vonovia non-green bonds as well. Also, one might deem the 40bp tighter spread on the Vesteda 0.75% 2031 bond vs the Vonovia 0.75% 2032 bond as a sign that perhaps in this instrument the greenium has materialized. But one needs to take the one-notch credit rating differential between Vesteda (A3) and Vonovia (BBB1) into consideration, which for example, in the commercial real estate space contributes to 27bp of difference, judging by the difference in valuations in Gecina (A3) and Covivio (BBB1), for example. This then leaves only 13bp of greenium, which seems scant given that Vesteda’s green bond portfolio generates nearly half the emissions as to what is reported at Vonovia company level.

Clearly, investors are not spending too much time on assessing impact report, because we would have ideally seen greeniums manifesting across all issuers. This is likely due to the poor state of the real estate credit market, where credit spreads have gone through the roof and liquidity has all but evaporated. However, given the occurrence of greeniums in the past, we would not be surprised that once the market normalizes, that the green bonds would outperform their regular equivalents. Especially since issuers are providing hard data these days on what kind of impact their green bonds are having.

This article is part of the SustainaWeekly of 14 November 2022