The Netherlands - Heading into budget and election season

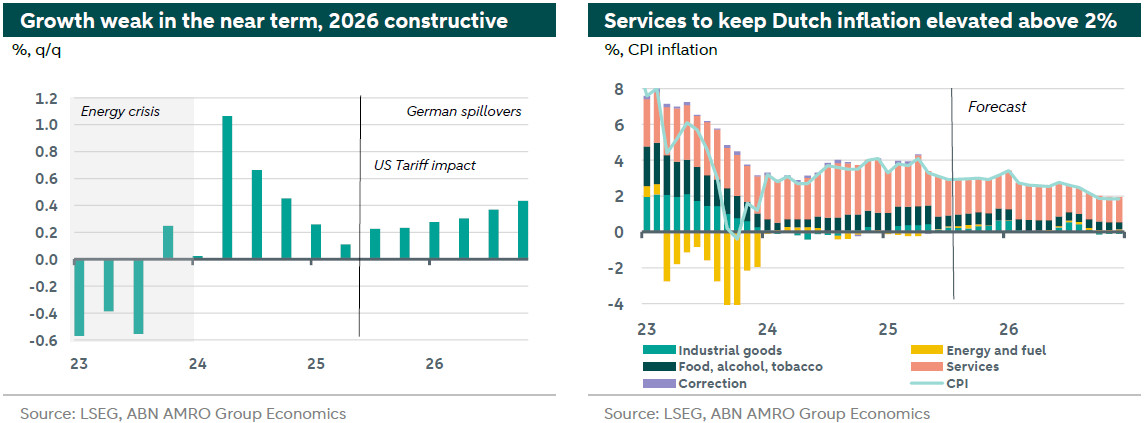

Q2 GDP came in at 0.1% q/q, roughly in line with our expectations (0.2% q/q), leading to small tweaks to our annual forecast of 1.5% in 2025 (from 1.6%) and 1.1% in 2026 (from 1.3%). Tariffs will weigh on activity in the near term, directly and indirectly via main trading partners. 2026 growth benefits from rate cuts, solid demand and fiscal spending in main trading partner Germany. After summer, it is all eyes on the Hague, with the caretaker government presenting the 2026 budget, and the election campaign ahead of the 29 October elections.

After the summer break it is all eyes on the Hague in the upcoming months. First, the third Tuesday of September is the traditional timing of ‘Prinsjesdag’; Dutch budget day. The current caretaker government will present the 2026 budget. More likely is that budget negotiations are taken hostage by the elections that take place roughly a month later. Typically, the caretaker status of government would mean that no new policies or large changes are forthcoming in the 2026 budget. But in light of the elections, however, the cabinet might announce some additional purchasing power measures to sway voters. Furthermore, we expect some news in areas where earlier decisions were postponed, such as financing of nitrogen policy and additional climate measures. Finally, perhaps the government will provide a first glimpse of how it intends to reach the new NATO target of 3.5% of GDP in core and 1.5% indirect defence spending, for which there was broad support in parliament. In any case, long term decisions and reforms, which are much needed given the many supply side constraints and future challenges faced by the Dutch economy, are not expected soon and subject to the outcome of the upcoming elections and following the formation process. Indeed, 1.5 month later, budget day is followed by the elections. Recently, the political campaign is slowly picking up steam. Current polls, which obviously can still change a lot, already signal large shifts in voting intentions. The previous government, before the far-right PVV quit the coalition, is projected to have just 56 seats left from the 88 seats they currently have in parliament, with more recent polls signalling an even bigger decline. While too early to be conclusive, a more centrist government, after the previous right-wing government, seems likely at this stage, but a lot can still happen.

In the background the economy is performing as expected. After a solid Q1, growth slowed in Q2 and is expected to stay weak in the near term, partly on the back of a direct and indirect impact from US trade policy, tariffs and uncertainty. It is private consumption and government spending that remain resilient and drive growth over the coming quarters. This is helped by a strong labour market. After ticking up slightly at the end of 2024, unemployment has been roughly stable at 3.8% in the year to date and is set to creep only a little higher, to average 3.9% in 2025, on the back of slowing employment growth and further easing in labour market tightness. Looking through to 2026 the outlook is more constructive. Uncertainty should decrease from current levels, which should also lead to some normalisation in the household savings rate. Also supportive of private consumption is the fact that CLA wage growth remains elevated, while inflation continues to moderate. Other factors supporting activity in 2026 are the pass through of ECB rate cuts, leading to a more accommodative credit cycle, and the expansive fiscal stance in Germany which has spillovers to the Netherlands. Finally, perhaps by 2026 we will have the initial contours of a new government, which should provide some clarity on the domestic policy front.