The Netherlands - Households supported by purchasing power recovery

Despite the Q1 contraction (1), growth is expected to pick up and to average 0.5% in 2024. Government spending and household consumption will be the drivers of this gradual growth. The stimulus measures in the newly announced coalition agreement are reason for us to slightly increase our growth estimate for 2025 from 1.2% to 1.3%. Inflation (HICP) will continue to gradually come down, averaging 2.5% in 2024 and 2.1% in 2025.

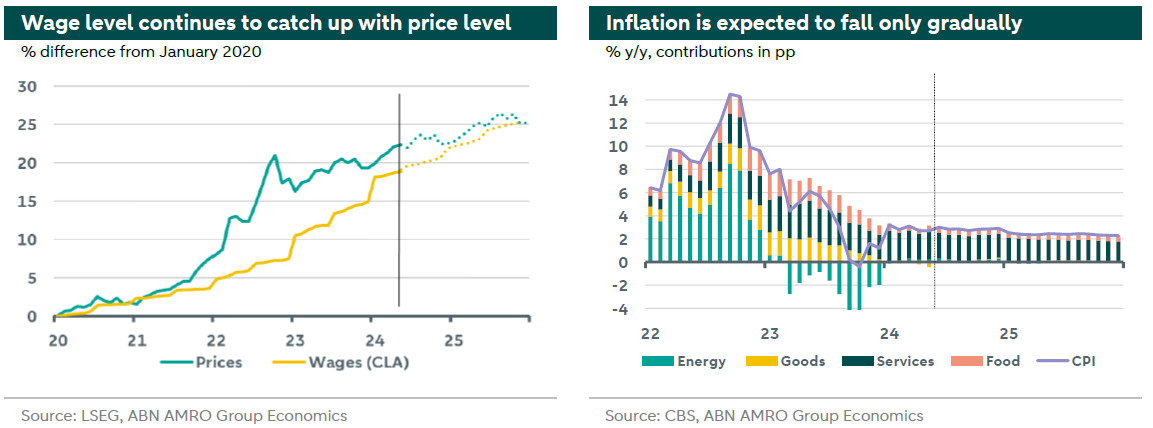

The second quarter is almost nearing its end, and so far the incoming data has confirmed our view that households and the government will drive economic growth in 2024. Since the last quarter of 2023 private consumption has been picking up, and we expect this trend to continue through 2024. Households are benefiting from three factors that are positive for purchasing power. Firstly, inflation is expected to fall further, although the 2% mark will remain out of sight for some time (see below). Secondly, the combination of lower inflation and strong wage growth is driving a recovery in purchasing power: the that opened up between wage and price levels since the pandemic and the energy crisis has now fallen to 3.5pp in May 2024, down from the peak in October 2022 when the difference was 13.8pp. As we expect wage growth to exceed inflation going forward, wage growth will have caught up with prices towards the end of 2025. Third, the caretaker government is also supporting real incomes in 2024, for instance through higher rental allowances and tax cuts for middle-income households. Lower income households in particular are benefitting from such redistributive policies. All in all, we expect household consumption to grow by 2.2% y/y in 2024 and to drive overall GDP growth.

The outlook for investment is weak in the short term. Because of the weak external environment, high interest rates, and low capacity utilization rates, there is little impetus to expand production capacity. We do see some investment growth in order to replace the existing capital stock. The tight labour market and shortages of skilled personnel is also weighing on both public and private investment. As a result, demand for credit is weak in the short term, as shown by survey results from the ECB’s Bank Lending Survey. Investment growth will improve when the expected easing of financial conditions happens and exports pick up, especially for sectors which operate internationally and are more rate-sensitive.

In 2024, the downward path in inflation has continued, although disinflation is slowing. Energy prices are playing a smaller role. Instead, labour-intensive services are making their mark on inflation. Although the risk of a wage-price spiral is limited, the current elevated wage growth is causing inflation to stay above the ECB’s target of 2% for the time being. Wage growth has peaked, which is why we expect services inflation to ease slowly over the coming quarters. Given the volatility in the global economy in recent years, the risks to our inflation forecasts are primarily to the upside. The main upside risks come from the geopolitical situation, for example escalation of the conflict in the Middle East and possibly contagion effects to energy markets. The coalition agreement will also have a small upward effect on inflation in 2025, as product-related taxes increase. All in all, we expect inflation to average 2.5% in 2024 and 2.1% in 2025.

(1) On Monday the second calculation of Q1 GDP showed a q/q contraction of 0.5% instead of 0.1% (read here). The backward looking adjustment will negatively impact our forecasts, it however does not change our view on the Dutch economy going forward. We are still reviewing our forecasts.