The Netherlands - Resilient consumers may surprise Q4 print

GDP expected to contract in Q4 2022 and Q1 2023, with growth to resume in second half 2023. The underlying trend in the broadening of inflation will continue well into 2023, but we expect headline inflation to decrease to an average of 4.3% in 2023.

Similar to the eurozone, the Dutch economy is showing resilience in the face of the energy crisis and high inflation. A better performance of the eurozone bodes well for Dutch external demand, while sturdy domestic consumer spending poses upward risks to our expectation of small contractions in Q4 2022 and Q1 2023. Even so, growth is still likely to be lacklustre in the first half of this year. We expect inflationary pressures to ease in the course of 2023. Government support and spending, as well as elevated wage growth, will lead to growth resuming in the second half of 2023.

Official consumption figures, available until November, show resilience despite inflation being still in double digits. There are however large sectoral differences. Overall, consumption is being supported by the catch-up in services, but goods consumption has been negative in annual terms since May 2022. As more households are exposed to inflation, through both higher energy prices and the broadening of inflationary pressures, we expect consumption to contract in the coming months.

On the back of rising interest rates and tighter monetary policy, the Dutch housing market has turned a corner. Whereas house prices rises in recent years have supported consumption via the wealth-channel effect, the turning of the tide in house prices means this support is falling away. We expect this negative effect to become larger in the course of 2023, forming another drag on consumption. An even larger, short-term effect on GDP from lower house prices comes from declines in housing investment. In similar fashion, overall investment is set for a weak year, being hampered by elevated uncertainty, weak prospects for demand and higher interest rates.

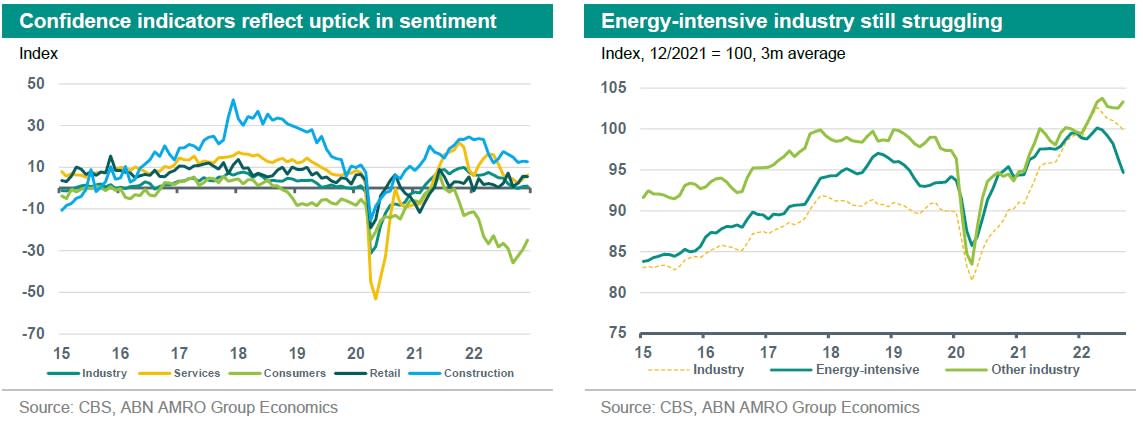

The effects of higher energy prices on the supply side have been less pronounced than anticipated. Still, this does not mean there is no scarring from record rises in energy prices at all. Total industrial production, albeit declining in recent months, remains quite robust. However, when decomposing industrial production, we see output in energy-intensive industrial subsectors falling significantly further.

Inflation has been declining for three consecutive months since the September peak of 17.1% yoy, to 11% in December. The recent declines are primarily energy related. We expect energy prices to contribute negatively to inflation in 2023, as wholesale energy prices have seen large drops recently and the price ceiling will cap household energy bills from January onwards. The underlying trend of broadening inflation in goods, services and food is continuing. Our view is that this trend will continue until well into 2023. This view is supported by our research on energy spending done by SMEs. We see that still a significant share of firms is not yet faced with higher energy prices due to fixed contracts. With these contracts ending, more firms will be exposed to higher energy prices and be forced to pass these on to customers (read more here). With average HICP inflation in 2022 coming out at 11.6% we expect inflation to decrease to an average of 4.3% in 2023.

This article is part of the Global Monthly of 23 January 2023