Tight US labour market keeps pressure on the Fed

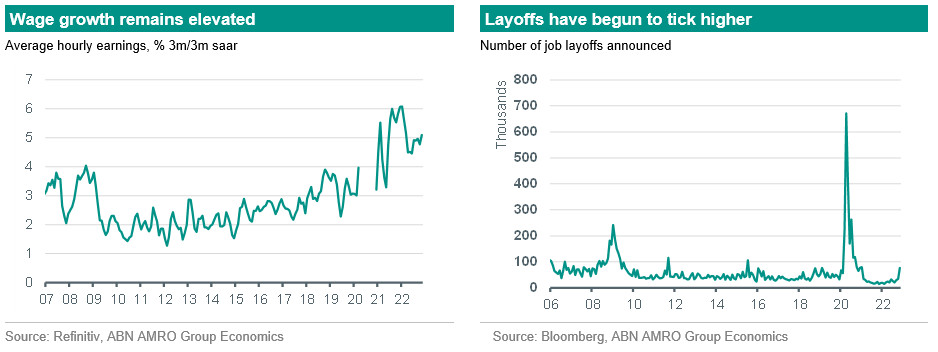

Nonfarm payrolls surprised to upside in November, with jobs growth of 263k, higher than our and consensus expectations for a 200k rise. Unemployment was stable at 3.7%, with a drop in participation offsetting a modest fall in employment in the household survey. More concerning for the inflation outlook, hourly earnings growth staged an unexpected uptick, rising 0.6% m/m, with October also revised up to a 0.5% m/m gain from 0.4%.

This took annual earnings growth up to 5.1% y/y, which is well above levels consistent with the Fed achieving its 2% inflation target; Chair Powell this week said that wage growth is currently running 1.5-2% above levels consistent with the Fed’s inflation target under reasonable assumptions of long-term productivity growth. Wage growth had been on a moderating trend for much of 2022, despite the extreme tightness of the labour market, and so today’s data comes as an unwelcome surprise that will concern Fed officials, just when other indicators are suggesting inflationary pressure is starting to ease off.

Labour hoarding is slowing the loss of labour market momentum

Indeed, the labour market overall does look to be cooling, albeit at a very sluggish pace. This week we saw a further modest decline in job vacancies to 10.3mn in October from 10.7mn in September. This took the number of job vacancies per unemployed person down to a still-elevated 1.7 from 1.9 (in more normal times, this ratio is below 1). The Challenger report on job cut announcements released yesterday also showed a rise in layoffs, although this rise is not yet consistent with recession-like conditions in the labour market. This is in line with findings from the Fed’s Beige Book, which cited ‘scattered layoffs’, although it also noted that “some contacts expressed a reluctance to shed workers in light of hiring difficulties, even though their labor needs were diminishing.” Ultimately, the labour market lags shifts in the broader economy, and we still expect broader economic weakness to drive a more significant loss of momentum in the labour market as we move into 2023, with the unemployment rate expected to rise to around 5% by end 2023. However, the situation of extreme tightness in the labour market that we are coming from means that this process could take longer, raising the risk that the Fed will be minded to go further with its interest rate rises than we currently expect.

Fed still likely to hike 50bp this month

While the continued tightness in the labour market will concern Fed officials, we think we are still on course for a downshift to a 50bp hike at the 13-14 December meeting, provided that the November CPI report (due out 13 December) does not surprise significantly to the upside. Following the December hike, we continue to expect a further downshift to 25bp hikes at the February and March FOMC meetings, with the upper bound of the fed funds rate expected to peak at 5%.