US and EZ GDP releases - Not just a frontloading story

US Macro: Import surge exaggerates GDP weakness. Eurozone upside surprise materializes before heading into a US tariff induced slowdown. France disappoints as underlying data looks worse. Germany solid start to the year moving into trade uncertainty German. Dutch growth slows to 0.1%, partly expected, partly unexpected.

US Macro: Import surge exaggerates GDP weakness

Q1 GDP came in at -0.3% q/q saar. As expected, underlying demand remained solid, with consumption growing 1.8%, and the weakness almost entirely driven by a surge in imports of 41.3%. Looking ahead, we expect underlying growth to slow more meaningfully and for the economy to skirt recession. This will be driven by both the real income shock from higher tariffs, as well as the uncertainty weighing on business confidence and investment. Our base case does not foresee a recession, though the risk is clearly elevated. See here for more on our view of recession risk.

Eurozone upside surprise materializes before heading into a US tariff induced slowdown

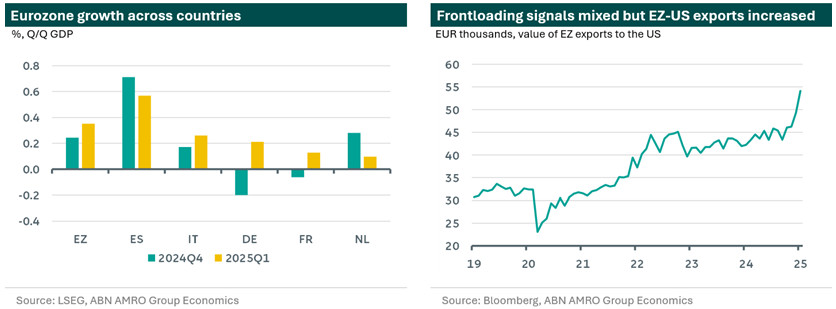

Eurozone Q1 growth surprised to the upside at 0.4% q/q (consensus 0.2%, ABN AMRO 0.3%) after growing by 0.2% q/q in 2024Q4. While the full breakdown is published later, the chances of an upside surprise increased after yesterday’s GDP releases, amongst which an Irish blowout (3.3% q/q), possibly due to frontloading as Ireland’s role as tax base for US multinationals, and a Spanish surprise (0.7% q/q). But even without Ireland there was some genuine strength. Next to Spain, Italy and Germany (see below) noted a solid start to the year. While the eurozone aggregate breakdown, as well as the country breakdowns lack at this stage, according to statistical offices, domestic demand has been a driver of growth in most countries. This fits the incoming data which showed solid momentum across industry, construction and services. As well as our view of elevated but easing wage growth, together with inflation moving towards target, leads to real income gains. Alongside the positive credit cycle this should lead to increased spending by consumers in the eurozone.

The big question mark was what happened on the external side. The signs of frontloading in Q1 were there. Such as increasing eurozone exports to the US (see graph), higher manufacturing PMIs and rising non-eurozone factory orders in Germany. But in the GDP data today the picture is mixed at best and it is likely not the factor driving today’s upside surprise. In some countries that did already report more details, such as Italy, France and the Netherlands net trade acted instead as a drag. In line with our view, frontloading likely provided a short term cushion for the ailing industry, especially in Germany, rather than something that has massively moved the macro needle.

Looking ahead, the first quarter high is unlikely to persist and the eurozone economy is expected to slow this year on the back of US tariffs and weaker global growth more generally. In Q2 there might also be some payback due to frontloading being largely over. In 2026 we anticipate eurozone growth to pick up on the back of an extended rate cut cycle by the ECB – with the deposit rate ending up at 1.5% in September – feeding through to economic activity and the slow ramping up of fiscal spending in Germany.

France disappoints as underlying data looks worse

French growth came in at the expected 0.1%, after contracting by -0.1% in Q4. The disappointment lies behind the headline as growth was mainly held up by inventory buildup and government spending amid a broader weakening of domestic demand, with private consumption and investment contracting. Particularly business investment, now without growth for four quarters in a row, is weak. France is less exposed to US tariffs directly than say Germany, but growth in France is set to stay weak in the coming quarters on the back of a broader slowdown in growth in the currency bloc.

Germany solid start to the year moving into trade uncertainty German

The German economy noted a solid start to the year, growing by 0.2% q/q after contracting by 0.2% in 2024Q4. While a detailed breakdown becomes available on May 23, points towards rising consumer spending and investment, coming from a low base, as factors driving growth. Details lack on the impact that frontloading had. Judging from the fact that it was not mentioned in the Destatis press release, we stick with our view that US companies frontloading their inputs from German firms acted as a cushion for the struggling industrial sector rather than something that added to overall growth. Looking forward German growth is expected to stay weak this year as structural issues in the industrial sector persist and more importantly, US tariffs will hit the eurozone’s biggest exporter. Further out, the German growth outlook is more positive as the slow ramping up of fiscal spending has lifted the growth prospects for the German economy, and thereby the eurozone, from 2026 onwards.

Dutch growth slows to 0.1%, partly expected, partly unexpected

Economic growth in the Netherlands slowed to 0.1% q/q from 0.3% q/q in 2024Q4. Looking at the subcomponents it shows a poor start to the year before US tariffs hit. International uncertainty has likely played a part in today’s figures, in part due to declining exports. Private consumption contracted (-0.2% q/q) contrary to our expectations. Consumers, which have record low confidence, spent less on food and cars amid real income gains and a tight, albeit, normalising labour market. Indeed, the period of extreme tightness in the Dutch labour market is behind us and while the unemployment rate is still very low and stand at just 3.9%, it has been creeping up slightly in the past months. The contraction in investment was expected due to payback of a policy change that incentivised a frontloading of investment in 2024Q4. Inventories held up growth, after a historically high rundown in the previous quarter. The government acted as a cushion on both growth, government consumption expanded by 0.5% q/q, and on the labour market, as indeed employment in the government sector grew contrary to some of the business sectors. Looking forward growth is set to remain low as tariffs hit Dutch exports directly and indirectly via main trading partners but resilient domestic demand should contribute to growth.