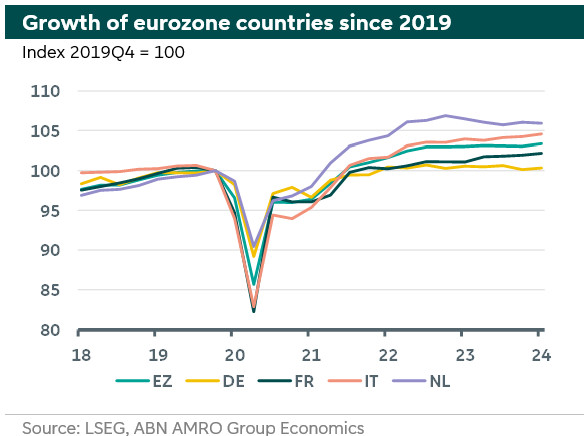

Weak start to 2024 for Dutch economy after unexpected contraction

The Dutch economy surprisingly contracted by 0.1% qoq in Q1 while unemployment stayed low. Imports stagnated while exports contracted. Quarterly private consumption growth fell back from 2% qoq in Q4 to 0.7% qoq in Q1.

The Dutch economy surprisingly contracted by 0.1% qoq in Q1 (ABN +0.2%, consensus +0.3%) while unemployment stayed low. The first quarter contraction follows a weak 2023. Indeed, in 4 of the last 5 quarters the economy has now contracted. The contraction was driven by a negative contribution from net exports and further stock depletion. This is somewhat surprising given the upside surprises we have seen in the eurozone (+0.3% qoq) and main trading partner Germany (+0.2% qoq), which seem partly to have been driven by stronger exports. Domestic demand on the other hand was strong as expected; particularly from households and the government.

The weak start to 2024 puts downward pressure on our annual growth forecast of 0.7%. However, we continue to expect more sustained but low growth over the course of 2024, as economic momentum has recently been on an improving trend. Rising real incomes continue to support household spending, government spending remains firm, and – more importantly – increasing global trade volumes and further bottoming out of the eurozone industrial sector as well as a pickup in overall eurozone growth should lead to a modest recovery in external demand.

Looking at the subcomponents, starting with the trade balance, imports stagnated while exports contracted (-0.1%). Goods exports (-1.3%) caused this decline while exports of services actually expanded (+4.7%). The weak export environment and high interest rates have depressed investment in recent quarters, particularly in construction. Overall, investment grew by 0.4% qoq. Businesses have favoured replacement investments in machinery and transport equipment over expanding production capacity.

Quarterly private consumption growth fell back from 2% qoq in Q4 to 0.7% qoq in Q1. Two opposite effects influenced this change; spending in Q4 was supported by the energy allowance for low income households, and this support fell away in Q1. On the other hand, improving purchasing power from rising real incomes will continue to support household spending throughout the year.

Overall, while the downside surprise to Q1 will make it harder to achieve our 2024 growth forecast of 0.7%, we continue to expect low but positive quarter-on-quarter growth over the course of 2024.

Unemployment stays low while labour market tension eases a bit. Labour market data for the first quarter of 2024 were in line with our expectations. The unemployment rate held at a historic low of 3.6% in March. Some cooling of the labour market is visible in a number of indicators suggesting that peak labour market tightness is behind us. Looking ahead, the Dutch labour market will remain tight, as labour demand – particularly in skilled jobs – remains high.