A record year for green bank debt

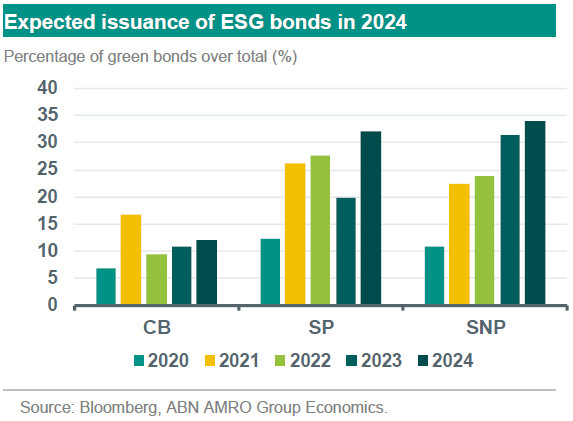

Issuance of euro benchmark ESG bonds in the financials space is set to break records this year. As the energy transition steps up pace, we expect supply of ESG bonds to rise again next year to a total of EUR 75bn (versus EUR 70bn in 2023). We expect supply of senior non-preferred bonds to rise to EUR 35bn, while the supply of green covered bonds is likely to remain stable.

Issuance of euro benchmark ESG bonds in the financials space is set to break records this year

Use of proceeds bonds tend to be the preferred ESG instruments both for investors and issuers

Senior non-preferred bonds are the preferred rank of debt to issue ESG-labelled bonds

As the energy transition steps up pace, we expect supply of ESG bonds to rise again next year to a total of EUR 75bn (versus EUR 70bn in 2023)

We expect supply of senior non-preferred bonds to rise to EUR 35bn, , while the supply of green covered bonds is likely to remain stable

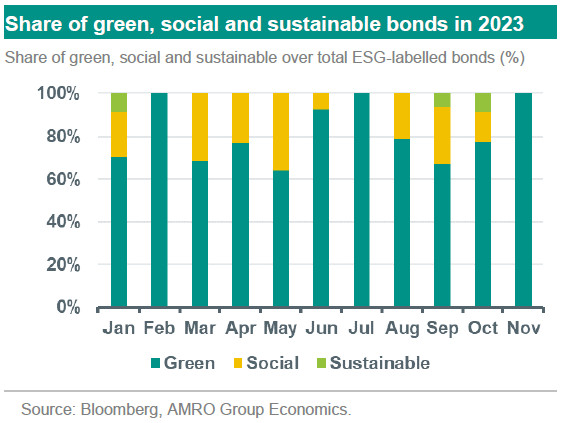

Issuance of euro benchmark ESG bank bonds in 2023 is set to be the highest on record. Now standing at around EUR 70bn, this number is already higher than the total amount issued in 2022 (EUR 66bn). Furthermore, the preferred ESG label remains the green use of proceeds one. From a total of 97 bonds issued, 74 were green-labelled, 20 had a social label, 3 were sustainable, and one was considered a novelty given its sustainability-linked loan funding framework (see ). This preference for green bonds corroborates with the results of our ESG investor survey, conducted in July this year. That coupled with a more advanced legislative environment for standards in green bonds make them the instrument of choice for both issuers and investors.

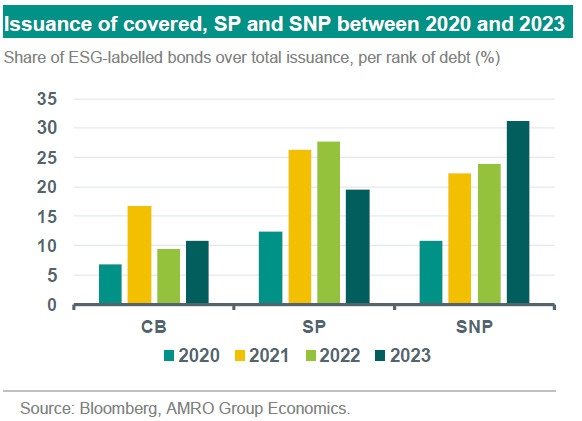

Furthermore, banks tend to prefer issuing senior non-preferred ESG bonds. For instance, a total of EUR 28bn of ESG-labelled senior non-preferred bonds were issued this year, which represents a share of close to 30% of total issuance. On the other hand, only 10% of total supply of covered bonds was ESG-labelled (EUR 18.5bn). And, in the senior preferred market, 19% of total issuance was ESG labelled (EUR 17.15bn).

The decreasing share of green covered bonds since 2021 regards the massive supply of covered bonds that banks have issued between 2022 and 2023. The rise of interest rates coupled with the volatility and the uncertainty lived in financial markets drove both issuers and investors to search for the safe-haven nature of covered bonds. However, as the pricing advantage of green covered bonds over standard covered bonds is only marginal, there were not sufficient reasons (from a funding cost point of view) for banks to prefer issuing a green covered bond over a non-green one. In terms of the use of proceeds, both covered and senior non-preferred bonds can finance several projects, from renewable energy projects to the mortgage of a house with an energy performance label ranking within the top 15% of the housing stock of a specific country. Nevertheless, there is a clear pricing advantage for an issuer to print a green senior non-preferred bond over a standard one, and that might explain the increasing issuance of green senior non-preferred bonds over the last years.

Considering the above, we expect issuance of green senior non-preferred bonds to increase in 2024 to an all-time high of EUR 35bn. As the energy transition becomes more and more urgent, banks are likely to increase lending to finance companies’ investments related to the energy transition. Therefore, banks will be able to issue more ESG-labelled bonds to finance these loans. Furthermore, as interest rates are expected to gradually decrease in the second half of 2024, it will become more attractive for companies to borrow and finance projects in order to accelerate the green transition.

With regards to green covered bonds, we expect supply to increase modestly to EUR 20bn. As mortgage lending growth is likely to remain modest, despite some pick-up in the second half of the year, green covered bond issuance will most likely be similar to that of this year.

This article is part of SustainaWeekly of 13 November 2023