Carbon Market Strategist - Bullish momentum amid changing dynamics

Gas and carbon prices are decoupling due to sufficient gas storage and upcoming LNG capacity in 2026. Industrial demand recovery in Europe has slowed, reflecting weaker demand for EUAs. US tariffs are expected to hinder industrial recovery until late 2025. Anticipation of a market deficit in 2026, tighter emissions caps, phaseout of free allocations, and early positioning by traders are driving the bullish trend in EUA prices. We foresee EUA prices to rise, averaging 80 EUR/tCO2 in Q4 2025 and reaching 100 EUR/tCO2 by end of 2026.

Introduction

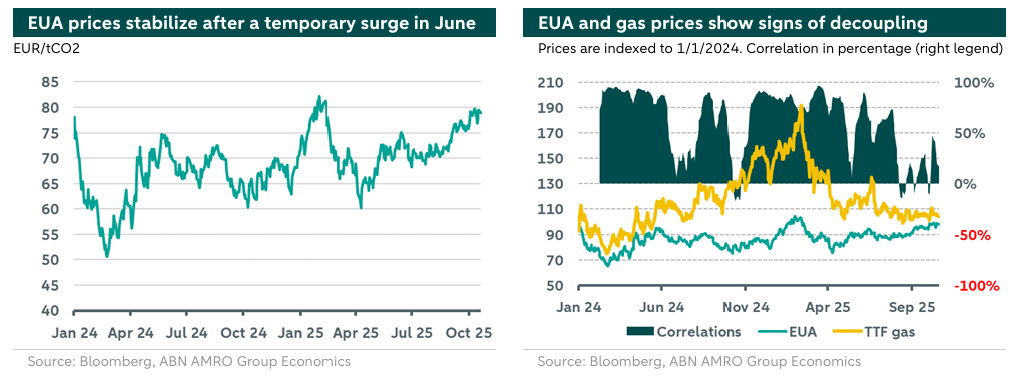

In Q3 2025, European carbon prices averaged 72.6 EUR/tCO2. However, Q3 marked the start of an upward trend, with prices climbing to levels last seen in January, a period of significant gas market uncertainty. Since the summer, there has been a decoupling of gas and carbon markets, which has shifted the primary drivers of carbon prices (EUA prices) increases to supply constraints, market sentiment, and forthcoming regulatory changes. As a result, market positioning has largely leaned bullish. Despite this, European carbon prices remain sensitive to weather variability and geopolitical risks, which influences power and heating demand. As of now, EUA prices are trading around 79.3 EUR/tCO2.

Carbon market developments

The European gas market is entering the heating season with sufficient storage and positive supply outlook as new LNG capacity is scheduled to become online in 2026. This has spurred relief in the market and has driven a decoupling between European gas and carbon prices, as illustrated in the right chart above. More details on recent European gas market developments can be found in our gas market monitor here.

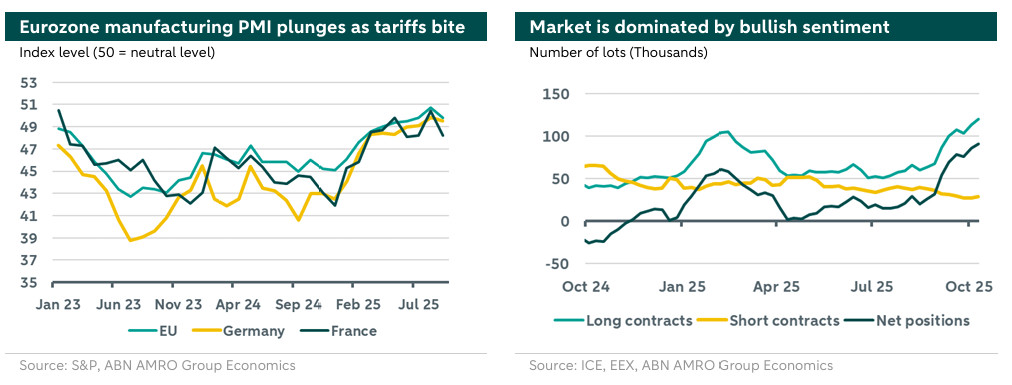

The recovery of industrial demand in Europe is experiencing challenges. In September, the Manufacturing PMI (Purchasing Managers' Index, see left chart below) showed a decrease, reversing the moderate improvements seen in earlier months. Since Manufacturing PMI often reflects trends in gas demand, this will translate into lower demand for emission allowances. The initial boost from stockpiling before the introduction of US tariffs appears to be fading away, and we anticipate that these tariffs will continue to hinder industrial demand recovery until late 2025. However, we are optimistic that economic recovery in Europe will gain momentum in 2026, driven by increased government spending on defense and infrastructure projects. However, the economy will also feel the negative effects of US tariffs on the global economy, disrupting trade flows and shipping. As a result, emissions from voyages to and from European ports will decrease, reducing the demand for EUAs in that sector (shipping and aviation), particularly in the latter half of 2025. Meanwhile, emission from the power sector in the third quarter remains below historical averages.

Despite this lower demand, the anticipation of a supply deficit in 2026 has emerged as a major bullish driver. EUA prices have been rising steadily since July, reaching 80 EUR/tCO2, a level not seen since January. Traders and compliance entities have started positioning early, with auction volumes high in 2025 but expected to drop significantly in 2026 due to delays in cancelling surplus shipping allowances. Additionally, the tightening of the cap—through a higher linear reduction factor—and the gradual phaseout of free allocations are limiting medium-term supply, encouraging hedging and speculative buying. The bullish trend gained further support as power sector participants purchased allowances ahead of the winter compliance season and compliance demand rose ahead of the September 2025 surrender deadline. However, this was dampened by growing optimism about higher liquidity, as the EU and UK carbon markets edge closer to potential linkage talks.

Furthermore, several policy changes boosted market sentiment, including the planned implementation of the Carbon Border Adjustment Mechanism (CBAM) in 2026 and the possible tightening of the Market Stability Reserve (MSR), both of which point to a more constrained market outlook.

Meanwhile, the European Union's Parliament has approved updated measures to simplify the Carbon Border Adjustment Mechanism (CBAM), focusing on reducing compliance costs and improving reporting processes for importers. Further clarification on carbon leakage risks, downstream product coverage, and emissions calculation are due before the full implementation by 2026.

Outlook

With the heating season approaching, the link between gas and carbon prices may temporarily reemerge due to factors like adverse weather—such as cold spells or slow wind—or geopolitical risks, including an escalating US-China trade war or new sanctions and tariffs from the US Administration. Meanwhile, we remain bullish, prompting an upward revision of our outlook for the coming quarters. For Q4, we now forecast an average price of 80 EUR/tCO2 (previously 75 EUR/tCO2). This upward trend is expected to continue into 2026, driven by Germany's fiscal stimulus and tighter allowance supply. The table below outlines our updated EUA price outlook for the next quarters. See more on long term projections and potential regulatory shift in the EU-ETS in our earlier publication here.