Carbon Market Strategist - Geopolitical risks drive market volatility

Geopolitical risks put upward pressure on EUA prices through their impact on energy markets. EUA demand from main sectors remains low as emissions from power generation retain its downward trend, while Eurozone PMI composite shows weak signs of industrial recovery . As we approach the surrender date in September, we expect a limited increase in demand. The bearish sentiment is still dominating the market, though markets remain responsive to unusual weather conditions and geopolitical tensions. Our outlook for the EUA price to is to range between 67 and 73 €/tCO2 during August and September.

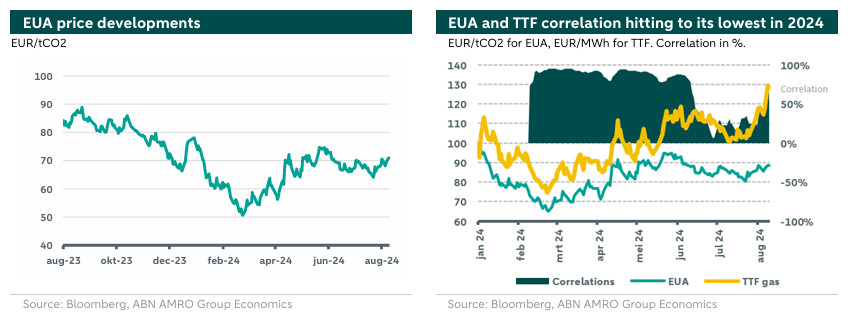

EUA prices averaged 68 €/tCO2 since the beginning of July. The market has been relatively stable during the summer. However, the revive of geopolitical risks are affecting prices upwards through their impact on energy markets. That is, the correlation between EUA and gas prices is regaining importance after a period of decoupling since the start of June. Demand from main sectors remains weak and the bearish sentiment is still dominating the market. Demand for allowances could increase as we approach the upcoming surrender date in September. EUAs are trading around 71 €/tCO2, at the time of writing.

EUA price drivers

The decoupling of EUA prices from the gas prices that started in June is getting weaker as fears of LNG supply disruptions amount following the revive of tensions in the Middle East. The correlation between EUA and TTF prices is now 68% (was 6% in June), as shown in the right hand chart below, which Increases volatility, at least in the short term. However, in the long term, as the share of renewables increases with more deployments, and LNG supply risks dissipates with additional operating capacity (new additional LNG capacity in Qatar and the USA is expected to be online in 2026), events in the gas market will become less important in driving EUA prices.

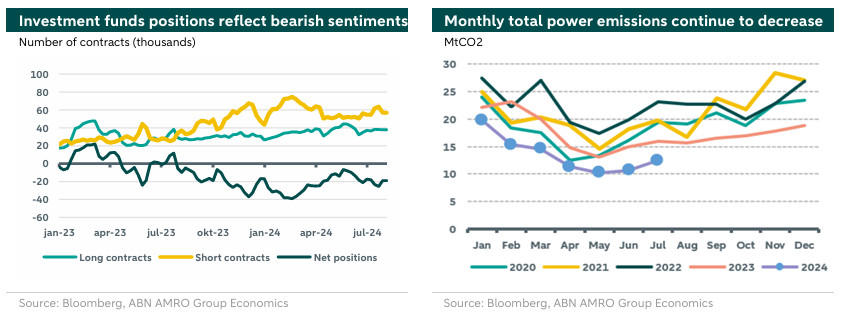

Monthly emissions from the power sector are still below historical levels (see right hand chart below), reducing demand for EUAs from this sector. This trend is mainly driven by the rising share of renewables in the electricity mix.

Demand from industry also remains low as the expected recovery in economic activity shifts towards the end of the year. Similar to June, there were still no signs of recovery in industrial production in July as reflected by the composite Purchasing Power Index (PMI) for the Eurozone. More precisely, the index declined in July compared to that for June, entering the stagnation territory (at 50.1, down from 50.9 in June). Furthermore, the manufacturing PMI stayed far in contractionary territory at 45.6 (down from 45.8 in June). Weakness in output and demand, particularly in the German manufacturing sector is a main reason for this (see more in our note here).

One important event for carbon markets is the coming surrender date on the 30th of September which could increase demand for carbon permits in the coming period, putting an upward pressure on prices. However, we think such impact would be limited given the current market conditions and because 2023 emission levels were relatively low from both power and industrial sectors, while demand from the shipping sector is only relevant for 2024 emissions.

All in all, market sentiment is still bearish on the outlook for EUA prices as illustrated in the left-hand chart below where net short positions by investment funds have been dominated by short contracts. So, investors that held a positive view on prices have maintain their positions in July while a large majority of investors remain negative on prices.

Outlook

Given the above-mentioned developments, we think that market fundamentals are stable while geopolitical uncertainty remains a main driver for volatility. That is, prices will remain responsive to geopolitical developments in the Middle East and Ukraine affecting the gas market in the coming month. Similarly, extreme weather events, such as heat waves or slower wind would also affect prices upwards. Accordingly, our outlook for the EUA price is to range between 67-73 EUR/tCO2 during August and September.