China - Managing the growth slowdown amidst a ‘hot’ stock market

Domestic weakness broadened over the summer, with investment growth cooling sharply. We expect Beijing to add targeted stimulus to safeguard growth, but a ‘bazooka’ is still unlikely. Meanwhile, China’s stock markets do not seem to care about weaker macro data.

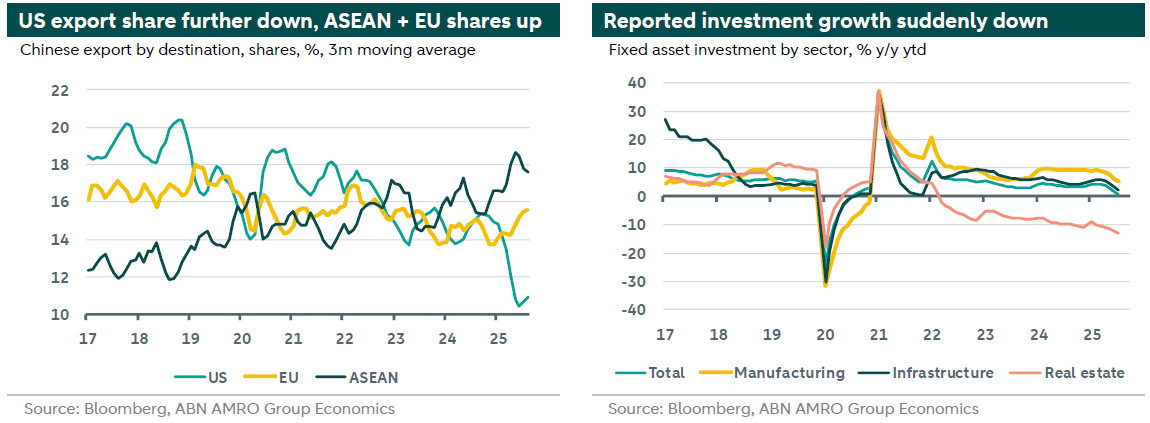

Domestic weakness broadened over the summer, with investment cooling sharply

China’s real GDP growth was remarkably resilient in the first half of this year, despite the US raising import tariffs since February (also see our previous Monthly update here). That resilience partly stems from trade rerouting (mainly through South East Asia) and reorientation to other destinations (including to the EU), offsetting the drop in direct exports to the US. However, slowdown signs are building in Q3, with July/August activity data generally disappointing (see China: Another month of weak data). Most striking is the broad slowing of investment, with year-to-date growth in manufactu-ring and infrastructure investment sharply down and property investment falling even deeper into contraction territory. The crackdown on excessive competition/overcapacity and the ongoing property sector slump are key drivers of this; going forward, a fading fiscal impulse (ceteris paribus) would bring headwinds too. Other recent hard data also point to a slowdown, with the supply side (industrial production) still stronger than the demand side (retail sales). The jobless rate picked up to a six-month high of 5.3%. In contrast, the August PMIs on balance brought a more positive picture, with the composite index from RatingDog (the new sponsor of the alternative PMI) rising to a nine-month high of 51.9.

We still expect Beijing to add targeted stimulus to safeguard growth, but no bazooka

Recent data are in line with our assumption of a material slowdown in annual GDP growth in the second half of 2025. That partly reflects base effects from a strong Q4-24. These weaker data will likely add to policymakers’ sense of urgency. We still expect Beijing to add further targeted fiscal support, aimed at supporting domestic demand (both consumption and investment) and stabilising the property sector. Some national consumer stimulus measures and local easing of housing restrictions have already been announced. On the monetary front, we expect some modest rate cuts and RRR cuts in the coming quarters to support the economy and fight deflation. The Fed’s September rate cut creates additional room for manoeuvre. Still, the PBoC will likely remain cautious, also taking financial stability angles into account (including a ‘hot’ stock market, see below). Also given the GDP outcomes in 1H25 (5.3% y/y ytd), we do not expect a ‘bazooka’, as the growth target of ±5% remains within reach. However, too much of a slowdown in 2H-2025 would not only bring this year’s target into jeopardy, but also lead to negative spillovers for next year, and it’s unlikely Beijing would tolerate a sharp downturn in annual growth for 2026. All in all, new stimulus initiatives are still likely to be more about limiting the downside in GDP growth rather than sparking a real new boom.

Meanwhile, China’s stock markets do not seem to care about weaker macro data

Despite the recent weakening of macro data, China’s stock markets remain quite ‘hot’. Over the past three months, China’s key stock index (CSI300) gained 17%, compared to the global average of ±10%. Measured over the past twelve months, this outperformance is even larger. Enthusiasm about AI breakthroughs in China (DeepSeek etc), the US-China truce in May (extended to mid-November - fresh US-China talks just concluded in Madrid), the anti-involution campaign that may support corporate profits, and hope for more stimulus are likely the driving factors behind this.