China - Reviewing our forecasts on the Iran conflict

Macro data have gotten more ‘bullish’ just before Middle East escalation. Slight adjustment of our growth forecasts for 2026 and 2027 on Iran conflict. Despite excess supply, cost-push pressures from energy price spike lead to higher inflation forecasts.

Macro data have gotten more ‘bullish’ just before Middle East escalation

China’s economy started the year on a strong footing (also see our recent China Macro Watch, On Iran, Trump-Xi, NPC and bullish data). The biggest improvement came from fixed investment, which turned back to growth in January/ February (+1,8% y/y) compared to a contraction of -3.8% in 2025. This turnaround was led by infrastructure spending, driven by local government bond issuance, but also by faster manufacturing investment and an easing slump in property investment. (Note, however, that China’s investment data are one of the least reliable, given all kinds of reporting issues.) The supply side keeps outperforming the demand side, amidst record external surpluses (see here). Industrial production accelerated to 6.3% y/y. Retail sales also picked up – partly helped by solid LNY spending, and despite falling car sales – but at 2.8% y/y remains relatively subdued. Earlier, the February PMIs showed a renewed divergence between the official survey (focus on large state firms) and the export-leaning RatingDog survey, with the export component of the latter jumping to a 5.5 year high. That was a prelude to the strong export growth reported for January/February (+21.8% y/y), partly driven by a firmer global business cycle – led by tech/AI – in the run-up to the Iran conflict.

Slight adjustment of our growth forecasts

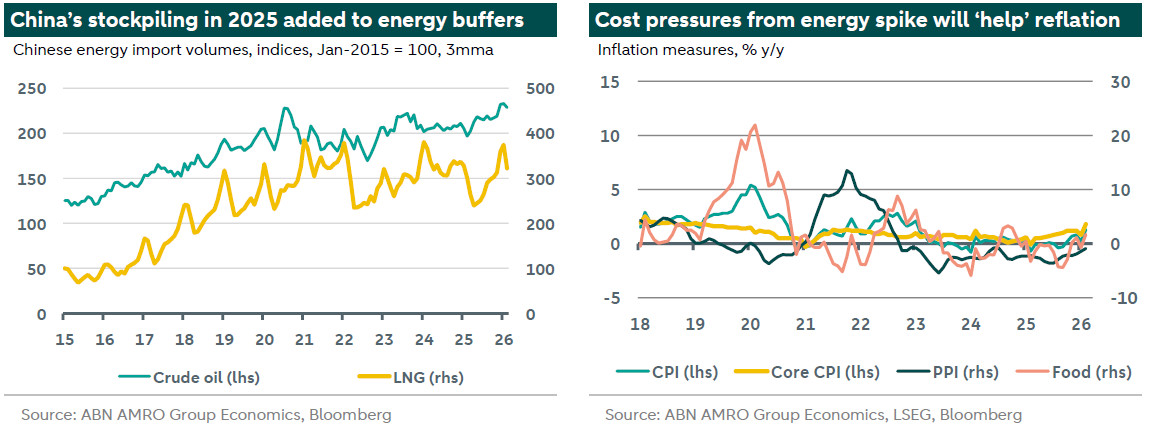

As the world’s largest energy importer and the key destination of energy shipments crossing the Strait of Hormuz, China is impacted by the Iran conflict. We still think there are various cushioning factors (e.g. high oil buffers, access to Russian energy – see here) that will mitigate the impact. However, downside risks have risen due to the conflict, taking into account direct effects, and also indirect ones such as the hit to global demand. Meanwhile, other geopolitical/geo-economic risks (e.g. trade relations with West, Taiwan) remain. We do not think the delay of the Trump-Xi meeting, originally planned for end-March/early April, is a prelude to a (sharp) escalation in US-China tensions, despite the US launching a fresh Section 301 survey into China and other countries post SCOTUS-ruling. We still think that both countries have clear incentives to extend the fragile tariff/chokepoint truce, amongst an increasingly complex global geopolitical landscape. All in all, we tweaked our quarterly GDP growth profile somewhat (stronger Q1, weaker Q2), and as a result slightly cut our annual growth forecast for 2026, to 4.6% (from 4.7%) – within the government’s target zone of ‘between 4.5% and 5%’, as announced earlier this month. We slightly raised our 2027 growth forecast to 4.5%, from 4.4%.

Reflation likely to continue in short term, as cost-push pressures rise on Iran conflict

Despite ongoing domestic excess supply, the spike in energy prices will lead to higher (cost-push) inflation in the coming months, even though the impact is cushioned. Before the conflict erupted, CPI inflation rose to a two-year high of 1.3% y/y in February, driven by LNY spending, food prices and base effects. Core inflation jumped to a seven-year high of 1.8% y/y, while annual producer price deflation eased further. We expect CPI inflation to pick up in Q2-26, before easing again later in the year. We raised our annual CPI forecasts for 2026 and 2027 to 1.2% and 1.4% (from 0.9% and 1.2%). We think this firmer inflation path will delay further additional (piecemeal) monetary easing steps to some extent.