ESG - At least 16% of Article 8 and 9 funds currently in breach of the new ESMA guidelines

As investors show increasing interest in sustainability matters, there has been an increasing inflow of money towards funds that portray a sustainability focus. As a result, some funds have adopted sustainability-related terms in their names, as a way of promoting and attracting more attention. Although investors should consider more than a funds’ name when deciding in what to invest, the name of a fund acts as an efficient marketing tool. This might ultimately create the wrong incentives for funds that, despite not investing in sustainable companies, misuse sustainability-terms in their names.

Following concerns about this risk of greenwashing, the European Securities and Markets Authority (ESMA) published guidelines for funds’ names. The final report, which was disclosed last May (see ), follows a public consultation conducted in 2022 and subsequent changes made to the draft proposal.

The guidelines are asking funds that use ESG-, transition-, and impact-related terms in their names to meet a quantitative threshold for sustainable investments and minimum safeguards.

The structure of this note follows as: in the second section we discuss the guidelines for funds’ names. In the third, we discuss which and what type of funds might get affected by these changes. And, finally, we conclude with an estimation of the costs of complying with the guidelines, and a few remarks about the next steps.

ESMA recently introduced name guidelines for European funds under the UCITS European Directive

Article 8 and 9 funds that have ESG-related terms in their names have to comply with a quantitative threshold of at least 80% invested in sustainable assets and meet minimum safeguards as per the EU Paris-aligned Benchmark (PAB)

To avoid penalizing transition funds, ESMA allowed funds with transition-related terms in their names to adopt the exclusion criteria by the Climate Transition Benchmarks (CTB)

In this note, we analyse the number of Article 8 and 9 funds using ESG- or transition-related terms that are breaching the minimum safeguards as per PAB and CTB

According to Bloomberg, there are 1,826 Article 6, 8 and 9 funds with ESG-related terms in their names, and 52 Article 8 and 9 funds with transition-related terms, under the UCITS directive

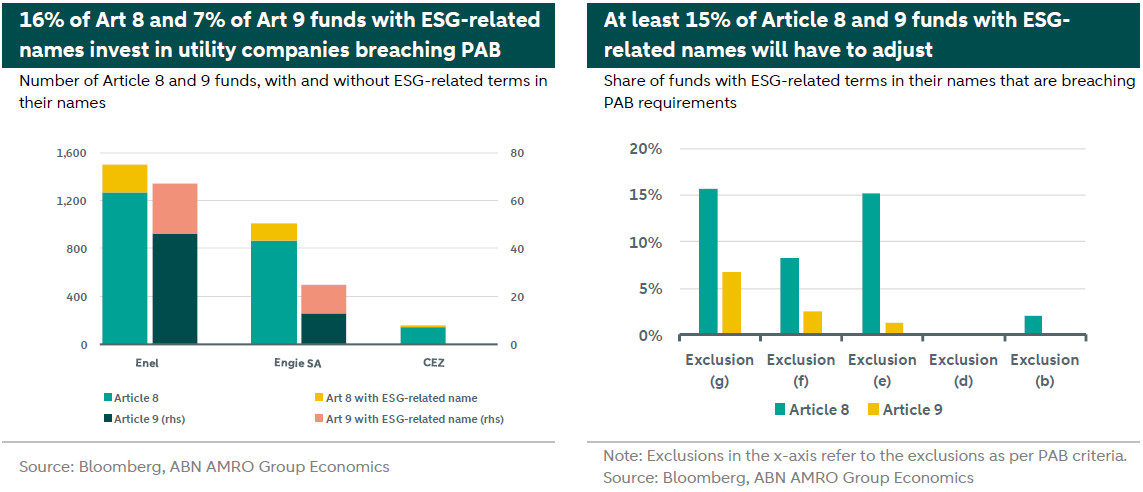

Our analysis shows that, of the Article 8 and 9 funds with ESG-related names, at least 16% and 7% of funds, respectively, invest in companies currently excluded by the PAB…

… ultimately meaning that an aggregate of at least 15% of funds would need to enact some changes in order to not breach the new ESMA’s guidelines

Of the funds with transition-related terms, at least 1% has to change either their name or portfolio

According to some funds calculations, these changes might cost each fund between EUR 20k and EUR 100k. Hence, in aggregate, we expect this guideline to cost EU funds at least EUR 18.3 million

What are the new ESMA guidelines?

The requirements for funds’ names vary depending on whether they include either ESG-related terms, transition- related terms, or impact-related terms.

Funds that have ESG-related terms in their name, (such as ESG, green-, environmental, etc), should use at least 80% of their investments to either meet environmental or social characteristics or sustainable investment objectives in accordance with their investment strategy. Moreover, they should meet minimum safeguards by excluding investments according to the (PAB). The PAB exclusions include

companies involved in any activities related to controversial weapons;

companies involved in the cultivation and production of tobacco;

companies that benchmark administrators find in violation of the United Nations Global Compact (UNGC) principles or the OECD Guidelines for Multinational Enterprises;

companies that derive 1% or more of their revenues from exploration, mining, extraction, distribution or refining of hard coal and lignite;

companies that derive 10% or more of their revenues from the exploration, extraction, distribution or refining of oil fuels;

companies that derive 50% or more of their revenues from the exploration, extraction, manufacturing or distribution of gaseous fuels; and

companies that derive 50% or more of their revenues from electricity generation with a GHG intensity of more than 100g CO2 e/kWh.

However, the PAB exclusions would unnecessarily penalise some funds that focus on transition strategies. As such, ESMA allowed for funds that use transition-, social-, or governance- related terms in their names, to follow the exclusion criteria of the (CTB). The CTB exclusions include:

companies involved in any activities related to controversial weapons;

companies involve in the cultivation and production of tobacco, and;

companies that benchmark administrators find in violation of the United Nations Global Compact (UNGC) principles or the Organization for Economic Cooperation and Development (OECD) Guidelines for Multinational Enterprises.

Where “environmental” terms are used in combination with “transition” terms in the name of a fund, the CTB exclusions should apply.

Finally, funds that use impact-related terms in their name, have not only to meet the quantitative thresholds and the minimum safeguards, but also to guarantee that their investments are made with the intention to generate positive, measurable social or environmental impact alongside a financial return.

Who gets affected by PAB minimum safeguards?

According to Bloomberg, there are a total of 1,826 funds under the UCITS European Directive that have English ESG-, or impact- related terms in their name (please refer to the annex for the full list of words used in this analysis). From a total of 1,826 funds, 3% are Article 6 funds (according to the Sustainable Finance Disclosure Regulation – or SFDR - definition), 80% are Article 8 funds, and the remaining 17% are Article 9 funds. Article 6 funds do not have, by default, any sustainable investment objective nor embrace investment in assets with environment or social benefits. As such, in order to comply with the new ESMA guidelines, at least 53 Article 6 funds will have to change their name in order to meet the new guidelines.

With regards to Article 8 and 9 funds, in order to assess whether those comply with the new ESMA guidelines, we need to check whether funds with ESG-, and/or impact-related terms in their names are meeting the minimum safeguards. That is, we need to check whether they are investing in companies that breach the PAB exclusions. For this analysis, we focus on exclusions (b), (d), (e), (f) and (g) from the list provided on the previous page. We use Bloomberg to check whether a company is excluded from PAB. Furthermore, and for simplicity, we are limiting our research to equity investments, only, and therefore not considering fixed-income investments.

In order to avoid double counting, we will analyse exclusions individually. We start the analysis by focussing on the funds that need to comply with the PAB.

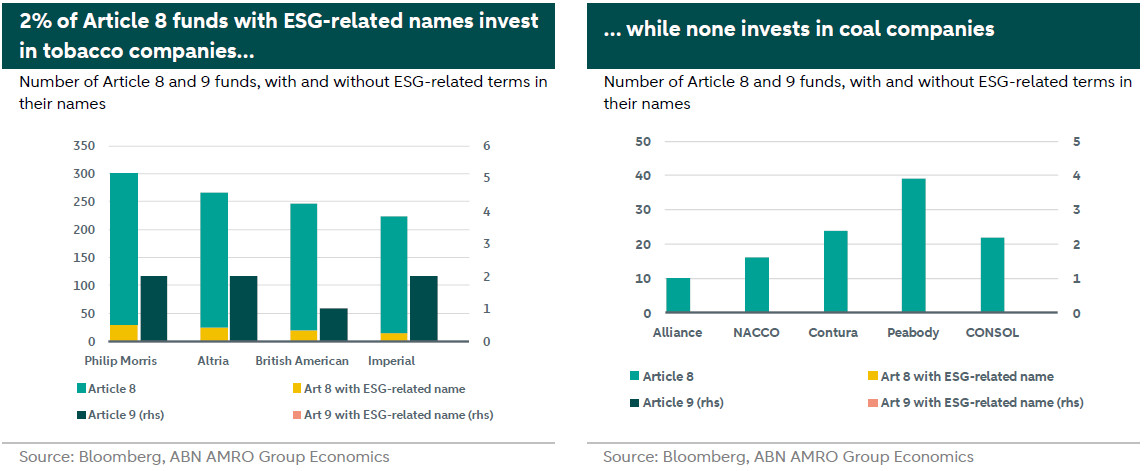

Exclusion 1: companies involved in the cultivation and production of tobacco

The following companies all breach exclusion (b) because they are involved in the cultivation and production of tobbaco: Philip Morris International, Altria Group, British American Tobbaco PLC and Imperial Tobbaco. Around 300 Article 8 funds still invest in at least one of these companies. However, from the Article 8 funds with an ESG-related terms in their names, only 2% invest in the aforementioned companies. There are no Article 9 funds (with or without ESG-related terms) that invest in these companies. Hence, we expect 30 funds will need to change either their investments or their funds’ name in line with the new ESMA guidelines.

Exclusion 2: companies that derive 1% or more of their revenues from exploration, mining, extraction, distribution or refining of hard coal and lignite

Our analysis shows that there are 39 Article 8 funds that invest in companies that derive at least 1% of their revenues from the exploration of coal. Of these 39 funds, none has an ESG-related term in their name. There are also no Article 9 funds that invest in such companies. As such, there seems to be no fund breaching the new ESMA guidelines in what concerns exclusion (d) of the PAB.

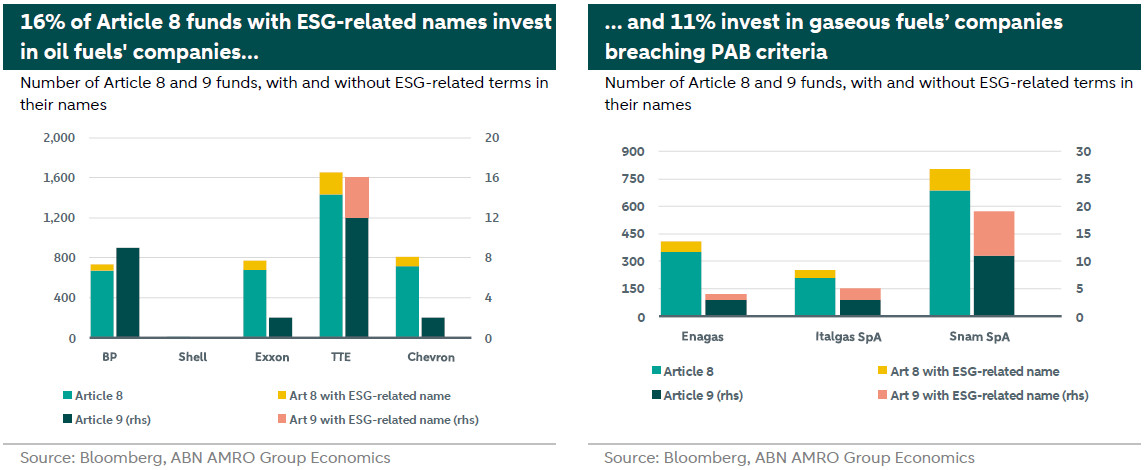

Exclusion 3: companies that derive 10% or more of their revenues from the exploration, extraction, distribution or refining of oil fuels

There are currently 1,650 Article 8 funds and 16 Article 9 funds that invest in at least one company that derives more than 50% of their revenues from the exploration of oil fuels. Nevertheless, considering the Article 8 and 9 funds with an ESG- or impact-related term in their name, only 15% and 1% of funds, respectively, are breaching the new guidelines. So, in total, we expect at least 225 of funds with an ESG-related term in their name that invest in oil companies to change either its name or its investments.

Exclusion 4: companies that derive 50% or more of their revenues from the exploration, extraction, manufacturing or distribution of gaseous fuels

While the scope of companies that might be in breach of this PAB exclusion might be broader, for simplicity, we focus our analysis on the gas distribution and transportation companies. Furthermore, as we previously mentioned, since our analysis is focused only on equity investments, we also only consider the companies that are publicly traded. This leaves us with three entities that are excluded by the PAB: the Spanish Enagas Financiaciones SA, and the Italians Italgas SA and Snam SpA. We however acknowledge that the exclusion scope might be broader, as such, there might be more funds currently breaching this requirement.

At least 805 Article 8 and 19 Article 9 funds still invest in one of three aforementioned companies. Nevertheless, looking at only the Article 8 and 9 funds with an ESG-related name, only 8% and 3% of the funds, respectively, invest in them. Therefore, we expect at least 128 of funds to enact some changes in order to not breach the new ESMA’s guidelines.

Exclusion 5: companies that derive 50% or more of their revenues from electricity generation with a GHG intensity of more than 100g CO2 e/kWh

Again, while the scope of companies that might be breaching this PAB exclusion can be vast, we focus for simplicity only on publicly-traded utility companies that have a large share of electricity generation coming from non-renewable sources. Of a total of 11 companies, only three are breaching PAB exclusions: ENEL, Engie, and CEZ. Almost 1,500 Article 8 funds and 67 Article 9 funds invest in at least one of these three companies. However, considering solely funds with ESG-term related names, only 16% of Article 8 and 7% of Article 9 funds invest in these utility companies. Hence, a total of 251 would be affected by the new guidelines.

Overall, assuming the least common denominator, it is fair to assume that at least 14% of a combined of Article 8 and 9 funds with ESG-related terms (that is, a total of 251 funds) will have to change either their name or their portfolio in order to comply with the new ESMA guidelines. In all fairness, as we previously noted, this is most likely an underestimation of the real number due to our screening limitations.

Who gets affected by minimum safeguards CTB?

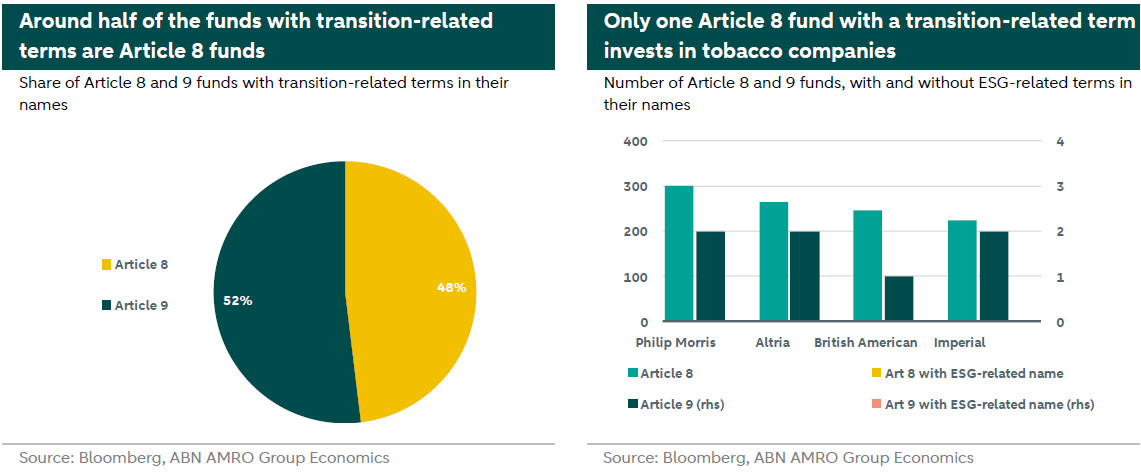

We now focus our analysis on funds that carry English transition-, social-, and/or governance-related terms in their names. We find a total of 52 Article 8 and 9 funds under the UCITS directive that include them in their names (please refer to the appendix for the full list of terms used). From these, 25 are Article 8 and the remaining 27 are Article 9 funds.

CTB exclusions are less stringent than PAB exclusions, allowing funds to invest in, for instance, utility companies or companies that derive their revenues from gaseous or oil fuels. As such, in this section, we are only considering exclusion (b), which regards companies involved in the cultivation and production of tobacco.

Using the same four tobacco companies as before, we know that 300 Article 8 and 2 Article 9 funds invest in tobacco companies. From these, however, only one fund has a transition-related term in its name, mainly a fund that invests in both Philip Morris International and Altria Group.

Overall, from the funds with transition-related terms in their names, 1 (or less than 2%) will have to either change its name or change its portfolio in order to comply with the new ESMA guidelines.

How much will it cost?

ESMA has received from some funds an estimate of the cost related to complying with the new guidelines. These costs would include prospectus updates, staffing, post-contractual information, internal coordination, training for financial advisors, among others. Some funds mentioned a one-off cost of EUR 20k, while others mentioned as much as EUR 100k. Assuming the median between these two values, we get to a total of EUR 60k per fund. As such, and assuming that at least 305 Article 6, 8 and 9 funds need to make changes, we estimate an aggregate cost of at least EUR 18.3 million.

What are the next steps?

The new guidelines will be translated to the official EU languages soon, and adopted by each country, accordingly. Following the publication of the translations, existing funds are expected to adopt the guidelines in nine months, while new funds created after the date of application of the guidelines should apply the guidelines immediately.

At the same time, the pathway to adoption might not be so smooth. Critiques have already been made to the final report, as stakeholders (e.g. ICMA, funds) agree that it might be premature to set numerical thresholds, as the definition of sustainable investments needs to be better defined. They also believe that the minimum safeguards should be less stringent than the ones adopted. As such, it is yet to be seen whether ESMA will release more clarity on these topics going forward.

Annex: list of words

English ESG-, and impact-related words

Climate / Clim

Environment

Environmental

Environmentally

ESG

Green

Impact

Impacting

Impactful

Sustainability

Sustainable / Sust

SRI

Responsible

PAB

Paris-aligned

Carbon

Biodiversity

Clean

Net-zero

SDG

English transition-, social-, and governance- related words

Transition

Progress/ion

Transform/ation

Change

Adapt/ation

Improving

Social

Governance

Evolution