ESG Economist - Climate Outlook 2026: Beyond 1.5 °C

Surpassing 1.5°C global warming is increasingly near, and continuing current policies would lead to around a 2.8 °C temperature increase. The EU agreed on its NDC 3.0 just in time; however, ambition seems to have weakened increasing the chance that goals will not be met.

Introduction

The signs are not very promising. Ten years after the Paris Agreement, efforts to limit global warming to 1.5°C compared to pre-industrial levels are lagging behind. For the upcoming COP30 in Belém, countries were expected to submit new and more ambitious Nationally Determined Contributions (NDCs). However, delays in this process and a lack of ambition show that in many parts of the world, priorities lie elsewhere. This note discusses the current state of play against the background of COP30.

The future of the 1.5 °C target

Ten years after the Paris Agreement, COP 30 is taking place in Belém, Brazil amid serious challenges. When the Paris Agreement was signed in 2015, the world appeared to be on track for global warming of about 4 °C. According to the Emissions Gap Report, current policies are now linked to a projected warming of 2.8 °C. Although this signifies notable progress, it still falls significantly short of the Paris Agreement goal of “1.5 °C and at least below 2 °C”.

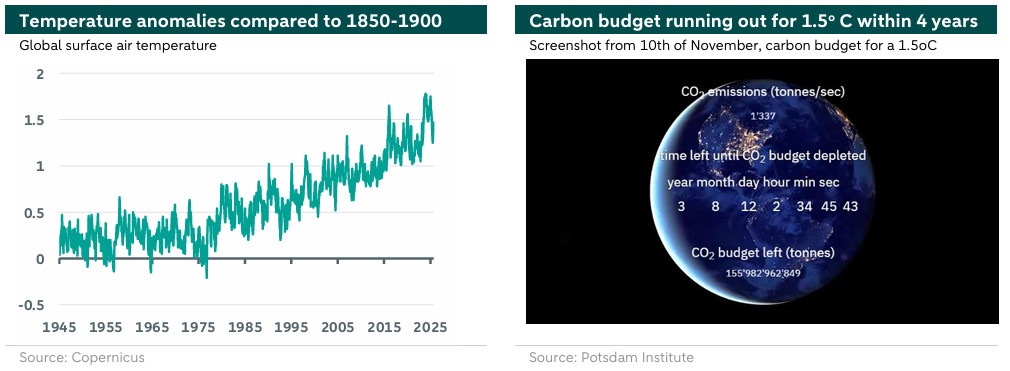

Many scientists no longer consider the goal of limiting the temperature increase to 1.5 °C to be credible. Global warming currently stands at about 1.4 °C and is projected to structurally overshoot 1.5 °C within a few years. This is firstly due to the fact that global GHG emissions are not on a reduction trajectory that would lead to 1.5 °C. Global emissions in 2024 have yet again broken records. Global greenhouse gas (GHG) emissions reached 57.7 GtCO2e in 2024, a 2.3 percent increase from 2023 levels, after having increased 1.6 percent between 2022 and 2023. According to the report, the increase in 2024 was more than four times higher than the annual average growth rate in the 2010s and comparable to the emissions growth seen in the 2000s. The carbon clock (that you can see below on the right, access here) suggest that at the current speed, the carbon budget for a 1.5 °C scenario will be consumed in less than four years. Secondly, there are signs that the climate is responding more sensitively to a certain level of emissions ().

A more sensitive response of the climate to emissions means that emissions must fall faster to achieve the same outcome: in terms of temperature increase, frequency of extreme weather events and surpassing tipping points. According to some scientists, at least one tipping point seems to have already been reached, namely that the oceans have warmed so much that large-scale coral reef die back has begun and is now inevitable (). Global losses due to natural disasters in 2024 were estimated to be between USD 320bn and 417bn, which is about double the average over the past 30 years. Insurers report that approximately one-third of those losses were covered by insurance. The protection gap (the uninsured or uninsurable part of these damages) continues to widen.

Despite the fact that the temperature increase will almost certainly exceed 1.5°C, the upper bound of the Paris Agreement of “1.5°C and at least below 2°C” appears to remain intact. This reflects a compromise between the scientific and political perspectives, and some policymakers fear that abandoning the 1.5°C target could undermine efforts. However, even if this target is not achievable, to minimize damage as much as possible, efforts must be made to limit climate change to the greatest extent possible.

NDCs have been delayed and if available, lack sufficient ambition

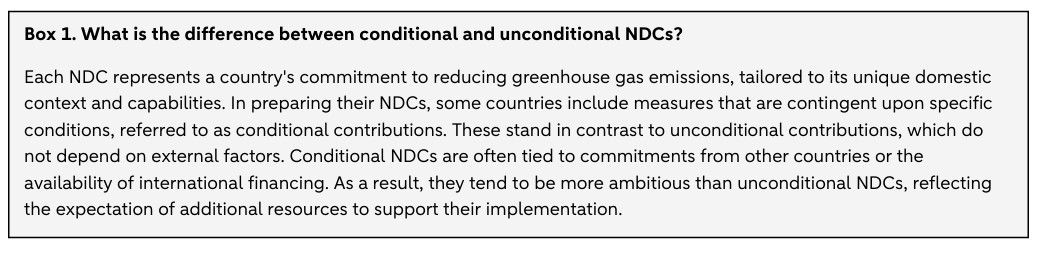

In order to limit global warming as much as possible, nearly 200 countries agreed ten years ago during the Paris Agreement to prepare, communicate and maintain successively more ambitious Nationally Determined Contributions (the key commitments made by countries to reduce greenhouse gas emissions and adapt to climate change). Starting in 2023, and then every five years, governments will take stock of the implementation of the Agreement to assess the collective progress towards achieving the purpose of the Agreement and its long-term goals. The outcome of the global stocktake (GST) will inform the preparation of subsequent NDCs, to allow for increased ambition and climate action. The 2023 GST concluded that collective efforts were not on track to meet the 1.5 °C target, while the 2 °C target was also at risk. Countries were therefore urged to increase the ambition of their “NDC 3.0” proposals. These NDC proposals, which include the extension of the NDC time horizon until 2035, were initially due to be submitted in February, but many have been delayed. Some, such as those of the EU, are becoming available on the eve of the COP30 and some may only become available later. At the time of writing, 60-70 countries have submitted their NDC 3.0. The NDCs that have been submitted are generally considered insufficient to give the 1.5 °C target a good chance of success.

EU: Last-minute agreement on the 2040 emissions targets

Shortly before the COP30 deadline, the European Council reached a last-minute agreement on amendments to the EU climate law ). The amendments include setting a 2040 target for greenhouse gas (GHG) emissions and introducing certain ‘areas of flexibility’. These amendments will take effect after approval by the European Parliament. The main point is that the EU has kept the earlier proposed target of reducing net GHG emissions by 90% in 2040 compared to 1990. However, three flexibility options were introduced. To begin with, ‘high-quality’ international carbon credits can make up 5% of the 1990 emissions, implying that the EU’s own reduction goal will be limited to 85% by 2040. In addition, there will be an (unspecified) role for domestic permanent carbon removals under the EU emissions trading system (ETS). Finally, there will be ‘enhanced flexibility within and across sectors and instruments, allowing member states to address shortfalls in one sector without compromising overall progress’.

Last, but not least, the Council agreed to strengthen the review clause of the existing European climate law, introducing a ‘biennial assessment to track progress towards intermediate targets. This assessment will be based on the latest scientific evidence, technological advances and the EU’s global competitiveness’. Among other aspects, the biennial review will address the ‘evolving challenges to – and opportunities to improve – EU industries’ competitiveness’. Based on the findings of the review and where appropriate, the Commission will propose revisions to the climate law, which ‘may include adjusting the 2040 target or other additional measures to strengthen the enabling framework, namely, to secure the EU’s competitiveness, prosperity and social cohesion’. In other words, the 2040 climate target is less strict and less predictable compared to the 2030 target, potentially allowing more room for delays and creating greater leeway to fail to meet the goals.

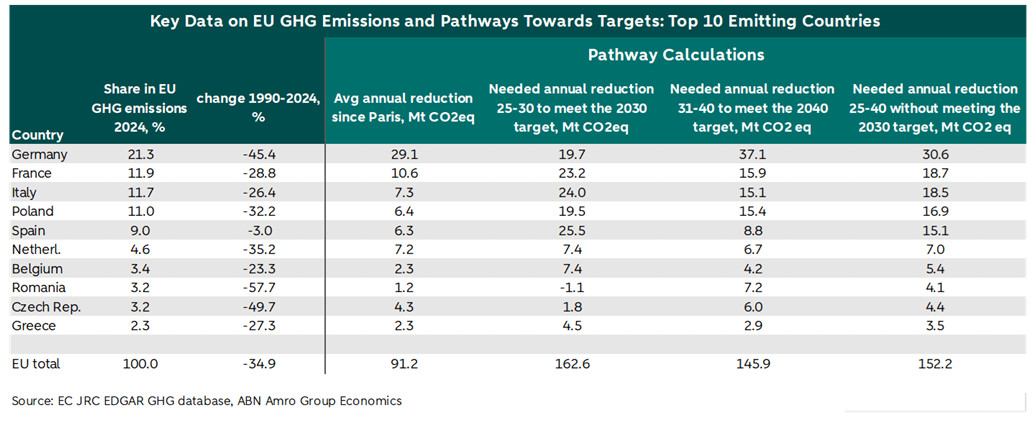

In the table below we present key data on GHG emissions by the EU’s top 10 emitting countries. This includes the annual average pace of GHG reduction since the Paris Agreement, the pace required to achieve the 2030 target of a 55% reduction compared to 1990 levels, and the pace needed to reach the 2040 target of an 85% reduction. Additionally, we have included a column showing the average annual pace of reduction required to meet the 2040 target directly, without first achieving the 2030 target. The data reveals that, to meet the 2030 target, the pace of reduction across the EU needs to nearly double compared to the post-Paris Agreement pace, with the largest acceleration required in Italy, Poland, Spain, and Belgium. Looking ahead to the reductions needed by 2040, the most significant acceleration is required in Italy, Poland, Spain, Belgium, and Romania.

China: underwhelming target, but may overperform

China has set comprehensive emissions targets for the first time this year. China is now the world’s largest source of greenhouse gas emissions, but at the same time a leader in clean energy production and technologies. The NDC submitted by China prior to COP30 is the first to outline a pathway that covers all forms of greenhouse gas emissions. In this NDC, China sets a target of a 7-10% reduction in emissions by 2035 compared to an undefined peak year. Although that peak is widely expected to be imminent (if not already reached), the scale of the reduction does not appear to be aligned with the 1.5°C target: according to Climate Action Tracker, emissions would need to fall by more than 50% by 2035 compared to 2023 levels to be consistent with the global 1.5°C goal. A mitigating factor is that in the past, China has tended to announce targets that appear disappointing at first glance, but subsequently overperform on them.

USA: Drill baby drill

The United States registered its NDC 3.0 in December 2024, but it withdrew from the Paris Agreement for the second time, shortly after President Donald Trump took office earlier this year. The US President is well known for his hostility towards efforts to combat climate change. Financing of green projects in the US has decreased, and tax credits have been restricted. President Trump has sought to stimulate domestic production of fossil fuels and exports of those products, and his administration is attempting to downplay, dispute or silence (the impacts of) climate change.

Emissions Gap Report concludes that time is lost with little progress

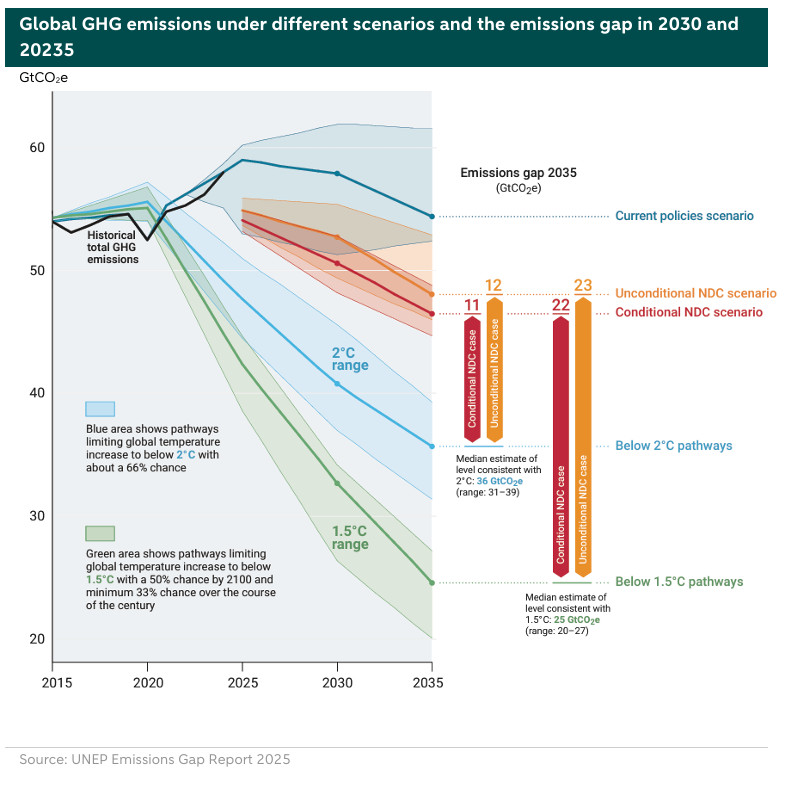

On the 4th of November, UNEP published their Emissions Gap Report . According to their definition, the emissions gap corresponds to the difference between the estimated global greenhouse gas emissions (GHG) resulting from the full implementation of the latest nationally determined contributions (NDCs), and the levels of emissions consistent with limiting warming to levels associated with the long-term temperature goal of the Paris Agreement. In other words, the gap represents the difference between what countries are pledging they will do, and the emissions required to keep global warming limited to well below 2oC. This section provides a stock take of the report’s main conclusions.

As mentioned previously, global emissions reached 53 GtCO2e in 2024. Looking forward, the current policies scenario results in global GHG emissions in 2030 and 2035 of 58 GtCO2e and 54 GtCO2e, respectively. The 2030 estimate is slightly higher than last year’s assessment (about 1 GtCO2e), mainly due to policy rollbacks in the US. For 2035, the estimate is about 3 GtCO2e lower, due to the impact of improved 2035 policy estimates, methodological updates, and harmonization, offset by policy changes in the US.

A continuation of the mitigation effort implied by current policies is only sufficient to keep global warming below 2.8oC over the century with a 66 percent chance. This level of warming would be reduced to 2.5oC if unconditional NDCs are fully implemented by 2035 and similar efforts continue. Even with efforts sufficient to meet the conditional NDCs in full, warming would only be kept below 2.3oC, with at least a 66 percent chance.

Moreover, the most optimistic pledges-based scenario included in the report, which combines the full implementation of conditional NDCs and all net-zero pledges, would limit warming over the course of the century to 1.9oC degrees with a 66 percent chance. This estimate is unchanged compared to last year.The updated policy projections and new NDC targets have lowered these warming projections by about 0.3oC compared to last year’s assessment. However, about 0.1oC of this limited progress would be cancelled out once the forthcoming official withdrawal of the US is accounted for. As for the remainder, 0.1oC is due to methodological updates, while only 0.1oC is due to updated policy projections and new NDCs. Therefore, the improvement in comparison to last year is almost non-existent.

All in all, the 2025 Emissions Gap Report highlights yet again that surpassing 1.5oC is increasingly near, and the risk of even higher levels of warming is rising fast.

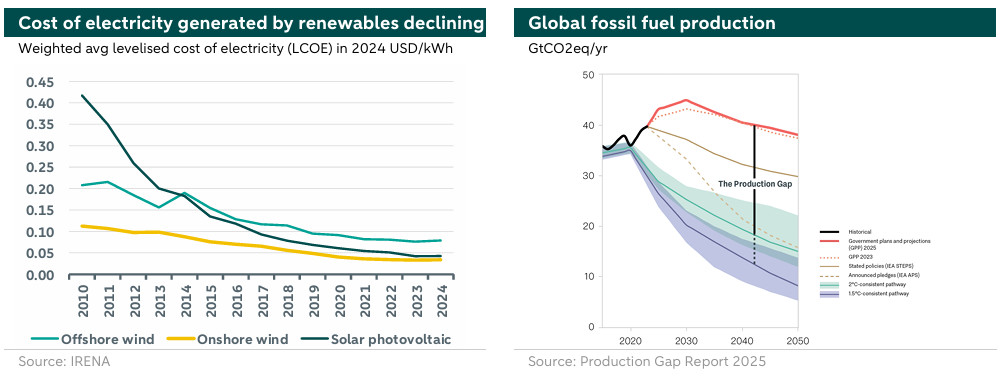

Fossil fuel production developments show widening gap with 1.5 °C goal

An important determinant of emissions reduction is the reduction in the use of fossil fuels. Fossil fuel production capacity needs to be phased down for a 1.5 °C scenario. Luckily, the cost of renewables such as solar and wind has been declining significantly (see graph below on the left). Solar PV panels have dropped in price by a quarter for each doubling of their installed capacity. Batteries have improved in quality and significantly decreased in price as their deployment has increased. This should be an important stimulus for transition, as the use of renewables is increasingly becoming the cheapest alternative. Also, there is a geopolitical argument: countries that don’t have their own fossil fuel reserves, can decrease their dependence on fossil fuel imports.

Still, the transition away from fossil fuels is going slowly. The 2025 Production Gap Report finds that the gap between the required fossil fuel production for a 1.5 °C scenario and the actual fossil fuel production has in fact increased rather than decreased compared to the 2023 Production Gap Report. The report analyses the 20 major fossil-fuel producing countries that are responsible for about 80% of global fossil fuel production. It finds that 17 of the 20 countries still plan to increase production of at least one fossil fuel by 2030. Moreover, eleven are currently expecting to produce more of at least one fossil fuel than they had planned in 2023. On the other hand, six of the 20 profiled countries are now developing domestic fossil fuel production aligned with national and global Net Zero targets, up from four in 2023. Still, overall, the countries plan to produce about more than double (120% more) the volume of fossil fuels in 2030 than would be consistent with limiting global warming to 1.5 °C, and 77% more than would be consistent with 2 °C.

More carbon pricing is vital, but political hurdles remain

To drive progress in reducing greenhouse gas emissions, implementing a robust carbon pricing system is essential. By attaching a financial cost to emissions, carbon pricing encourages lower emissions while generating revenue that can be reinvested in green initiatives or used to offset the burden of higher energy costs on households. However, political challenges have made it difficult to establish effective carbon pricing, leaving current rates too low to spur meaningful decarbonization.

A significant development in this area is the EU's Carbon Border Adjustment Mechanism (), set to launch in 2026 (although charges are only expected to become significant from 2030, when free emissions rights for EU producers run out). CBAM targets imports of carbon-intensive goods including steel, aluminium, cement, fertilisers, electricity and hydrogen. Under the system, importers must declare the CO2 emissions embedded in foreign-produced goods and purchase emissions certificates if those emissions exceed EU standards. CBAM is expected to draw considerable criticism as it is being perceived by some countries as a protectionist measure. There is a worry that the “carbon border tax controversy” will detract from other topics. Still, despite criticism, the carbon border tax concept appears to be gaining traction internationally. Britain plans to implement its own mechanism by 2027, and other countries are considering similar measures.

Not just further mitigation, but also implementation and adaptation

Despite the many challenges, COP30 will try to maintain the pressure on countries to do more to mitigate climate change. It is becoming increasingly evident that, while increased ambition levels are welcome, the implementation of such commitments is even more important. As expected, the USA will not be represented at COP30, but the Trump administration might still have an influence via its efforts to thwart other countries’ fight against climate change. All in all, expectations that significant increases in implementation or ambition will be agreed are low. Considering the current situation, the focus is shifting further from abatement and more towards adaptation. COP30 is meant to further develop a framework with indicators to track adaptation progress and, crucially, finance it.

Climate financing is likely to remain a point of contention between developed and developing countries. Developing countries argue that the flow of funds from the developed world is far too small in relation to their contribution to climate change and the costs of mitigating and adapting to climate change. Current financing needs for climate adaptation are many times the actual flows, see note here. 2025 (here) concludes that although there is some evidence of improved adaptation planning and implementation, the adaptation finance needs of developing countries by 2035 are at least 12 times as much as current international public adaptation finance flows. At COP29, it was agreed that USD 300 billion per year would be mobilized by 2035 to help developing countries mitigate and adapt to climate change, but developing countries estimate an additional annual USD 1trn is necessary.