First signs of Germany’s fiscal spending spree

Defence spending is surging, according to monthly government spending data. The spending jump is now visible in factory order data, with the recent strength driven primarily by weapons and aircraft orders. Defence spending is likely to provide a cyclical tailwind to industry. But it will not be a saviour by itself given structural headwinds. A key uncertainty remains how quickly spare capacity in German industry can retool to new sources of demand.

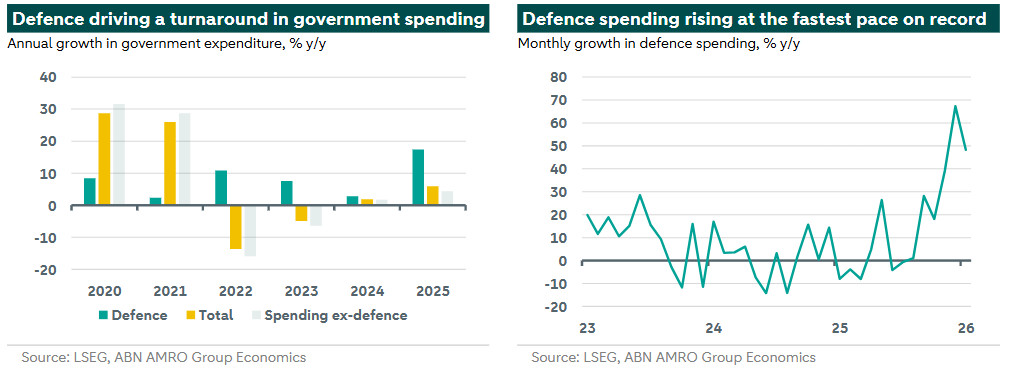

As noted in our latest Global Monthly, German government spending and factory order data released in recent months suggests the long-promised (see here) surge in spending on defence is finally materialising. Government finance statistics show the ramp up started in earnest last September and has continued to gain momentum since, with defence spending growing on average by 50% y/y in the three months to January. For 2025 as a whole, defence spending grew 17.4%-the fastest pace in at least 17 years (when comparable records began). This helped push overall government spending higher by 5.9% in 2025, the biggest rise since the pandemic period when – like in other European countries – spending jumped on the back of wage subsidy schemes. However, even excluding defence, spending still rose significantly in 2025 (by 4.3%) and other spending has picked up further moving into January (+8.5% y/y). We will explore other drivers of the government spending rise – for instance in infrastructure – in a future publication.

As well as helping to strengthen Germany’s defence capability, the spending surge is a crucial cyclical driver of the German economy; after years of fiscal tightening–when the government was a major drag on growth–it is becoming a significant positive impulse again.

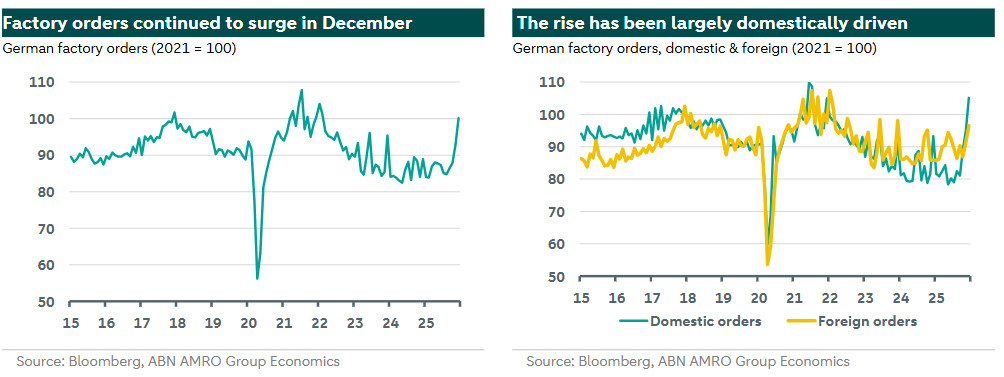

How is this spending manifesting in the real economy? The clearest signs are in German factory order data. Orders unexpectedly strengthened further in December following a jump in November, with orders growth accelerating to 13% y/yfrom 10.6% in November. The details showed that, although a rise in foreign orders contributed, the surge was largely domestically driven.

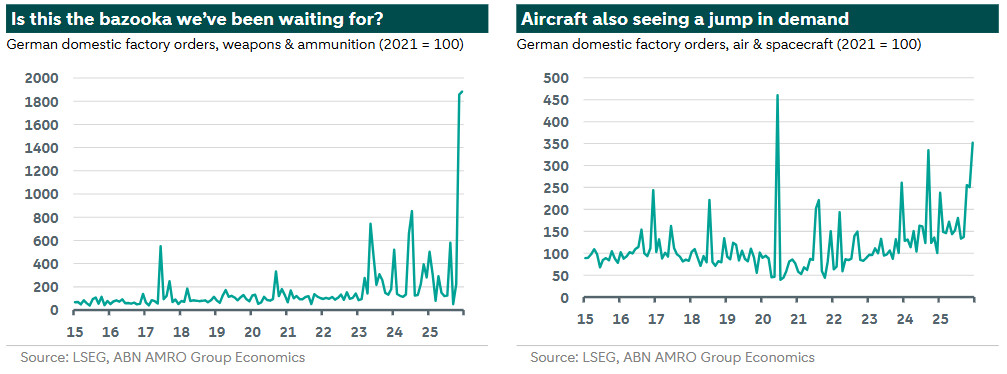

Perhaps unsurprisingly, defence-related sectors such as weapons and ammunition were the chief contributor –where orders were up a whopping 569% y/y in December. While orders in this category had already seen significant increases following Russia’s invasion of Ukraine – and some of the recent rise probably also reflects pledges by the previous government to raise spending – what we are currently seeing is clearly of an entirely different magnitude to before.

Another sector seeing a significant increase is in the air & spacecraft category. As the chart below-right shows, this is very volatile category, reflecting the lumpiness of civilian aircraft orders (Hamburg is a final assembly plant for the Airbus A320 family). However, Airbus has reported a record order intake in its defence division, boosted by Germany’s commitment to buy 20 new Eurofighter jets to modernise its air force.

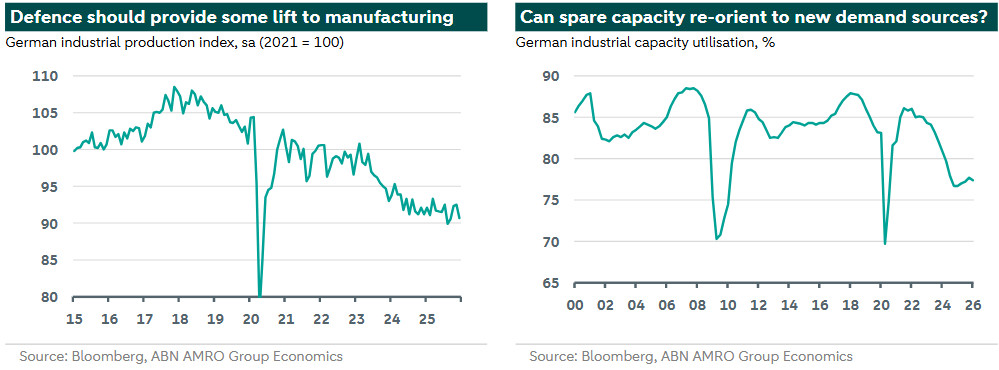

Is defence the saviour that German industry has been waiting for? Not quite, but it will help. While defence spending will clearly provide a boost to still - weak industrial production levels in Germany, a significant part of the spending boost will inevitably leak out in the form of higher imports–some of which neighbouring European countries are likely to capture. Moreover, German industry continues to face broader structural headwinds, from still - high energy prices, to intense competition from China, and a failure of the car sector to adapt more rapidly to the EV transition. These factors are likely to keep overall industrial capacity utilisation at relatively subdued levels, though there remains a question mark over how much and how quickly spare capacity in German industry will re-orient to the new sources of demand.

Finally, although defence spending tends to have a relatively low growth multiplier in the short-run (particularly now in Europe due to the reliance on imports), it has proven historically to have significant spillover effects to other areas of the economy – notably via R&D spending. This leaves us hopeful that it may have some positive impact on Germany’s longer term growth prospects (see our previous note on this here). Defence is also but one part of the overall spending push by Germany. We will explore this further in a future publication.