ESG Economist - EU remains vulnerable in supply of critical materials

The EU remains heavily dependent on imports of critical materials, despite efforts at diversification and strategic partnerships with resource-rich countries. Dependence on resource-rich countries increases the EU’s vulnerability to supply chain disruptions. The EU aims to increase mining, processing, and recycling by 2030, but long lead times and high costs make achieving these goals uncertain. The Netherlands plays a central role in the EU trade of critical raw materials, primarily through transit via ports without significant added value. The EU faces technological and economic challenges in effectively recycling critical materials, particularly rare earth metals.

Introduction

Critical materials are indispensable for the energy transition, strategic industries, and Europe’s economic resilience. This analysis examines the extent to which the EU, through the Critical Raw Materials Act, is on track to reduce dependence on external suppliers and increase security of supply. Several key questions are central to this analysis: What are the 2030 targets for the mining, processing, and recycling of critical materials, and how feasible are they? What do recent import trends reveal about the vulnerability of European supply chains? What role does the Netherlands play in the trade of critical materials? And to what extent do diversification and recycling help mitigate geopolitical risks?

Goals of the EU Critical Raw Materials Act (CRMA) under the microscope

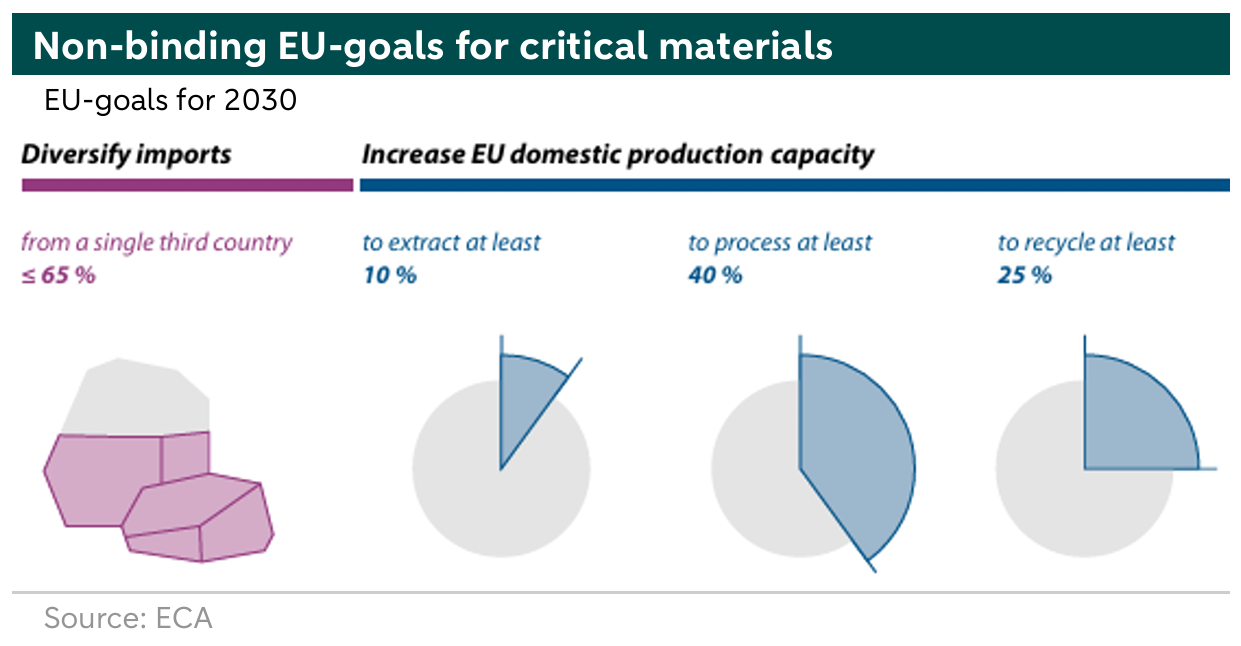

The EU Regulation on Critical Materials (CRMA) aims to ensure a reliable and sustainable supply of critical materials. This will reduce dependence on external suppliers. The regulation includes both binding and non-binding provisions for EU member states.

The non-binding 2030 targets are listed above. In essence, the EU aims to have a diversified import base by 2030, with no more than 65% of critical materials coming from any single country. In addition, the EU wants to boost mining and accelerate investment in processing capacity and the recycling of critical materials. The benchmarks are non-binding because EU member states cannot enforce them through regulation. The binding elements of the regulation are reflected in the streamlining of licensing and procedures, as well as stricter oversight of supply chains to prevent shortages of critical materials.

A 2026 study by the ECA (European Court of Auditors—the EU’s financial watchdog) shows that the non-binding targets have not yet been met. In the mining sector, approximately 8% of the EU’s consumption of ores and minerals was extracted within the EU in 2026. This appears to be close to the target, but when the CRMA was launched in 2024, this percentage was also 8%. Furthermore, this raises the question of whether the EU’s mining target was set with sufficient ambition.

There is a reason why progress in the mining sector is slow. Currently, the lead time for developing new mines is long. In Europe, it can sometimes take up to 20 years before a new mine begins production. The entire process of granting exploration and environmental permits, mining concessions, and land-use permits takes the most time. These long lead times make it difficult to achieve the 2030 targets, making a streamlining of procedures an absolute necessity. In addition, however, these are often capital-intensive projects that are frequently plagued by delays and cost overruns.

In terms of processing, the ECA estimates that capacity stands at 24%—16 percentage points short of the 2030 target—and for recycling, capacity is currently 12%, which is about half of the 25% target. Given these starting points, achieving the 2030 targets remains out of reach for the EU. Rapidly expanding processing capacity is a challenge for the EU. Relatively high energy costs make the feasibility of a new production facility difficult. In addition, international competitive pressure is strong.

To partially address these issues, the EU has established various funding programs to support investments and mitigate risks. The RESourceEU Action Plan includes a Critical Raw Materials Financing Hub. This is a fund with EUR 3 billion set aside specifically to provide various guarantees for projects involving critical materials. Projects eligible for this fund may focus on risk mitigation in investments, innovation, and storage. However, according to EIT Raw Materials (an EU-funded think tank), much more investment is needed. Their calculations indicate that at least EUR 10 billion is required to achieve the goals.

EU-imports critical materials on lower level

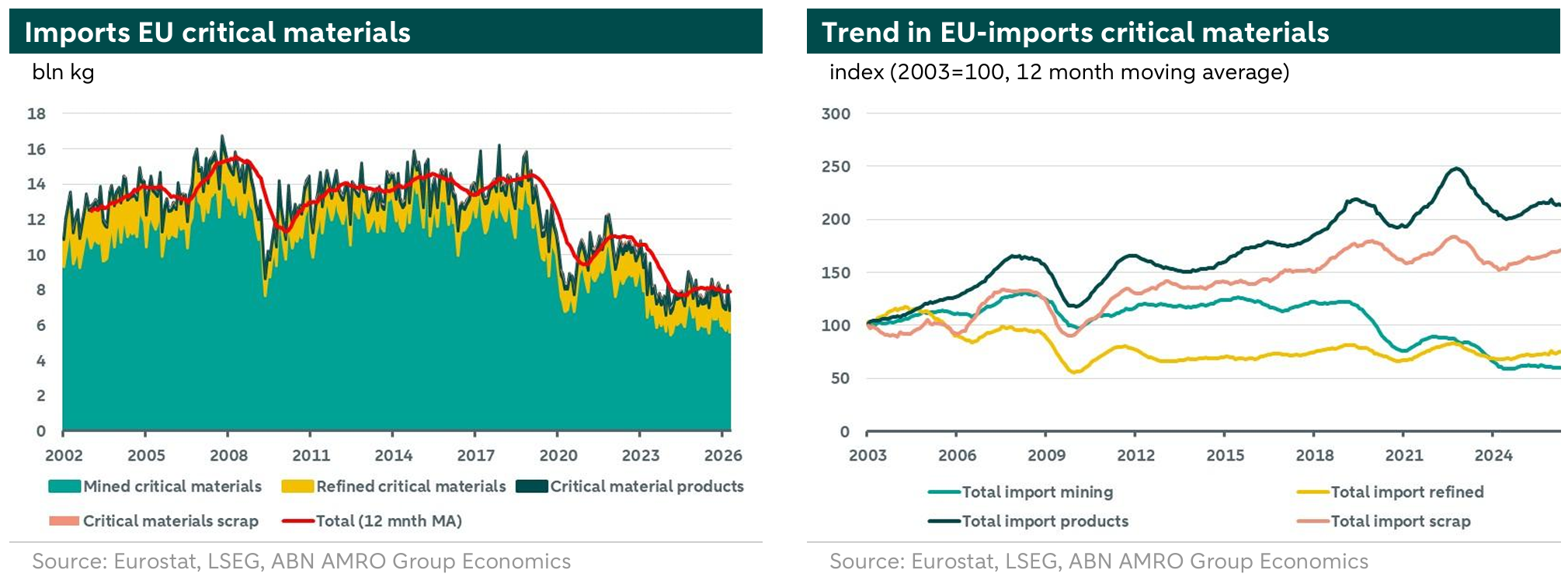

When it comes to the import of critical materials, we distinguish between four categories. These include the import of raw critical materials (ores and minerals), refined materials (i.e., purified materials extracted from raw ores or recycled scrap), products made from critical materials (such as copper wire, foils, chains, or pipes), and scrap (secondary materials obtained from recycling). Total imports of critical materials remained at nearly the same level each year from 2010 to 2018. After that, imports declined sharply, mainly due to the decrease in imports of raw critical materials. This was not only the result of export restrictions in countries rich in critical materials and ores, but also due to the decline in processing capacity and production in the EU caused by higher energy costs and intensified international competition.

However, imports of scrap and products made from critical materials are on an upward trend, while imports of refined critical materials remain virtually stable. In its policy, the European Commission (EC) emphasizes that dependence on these imports makes strategic sectors—such as industry (particularly clean tech), healthcare, energy, aviation, technology, and defence —highly vulnerable to disruptions in global supply chains.

The Netherlands as a hub in the trade of critical materials

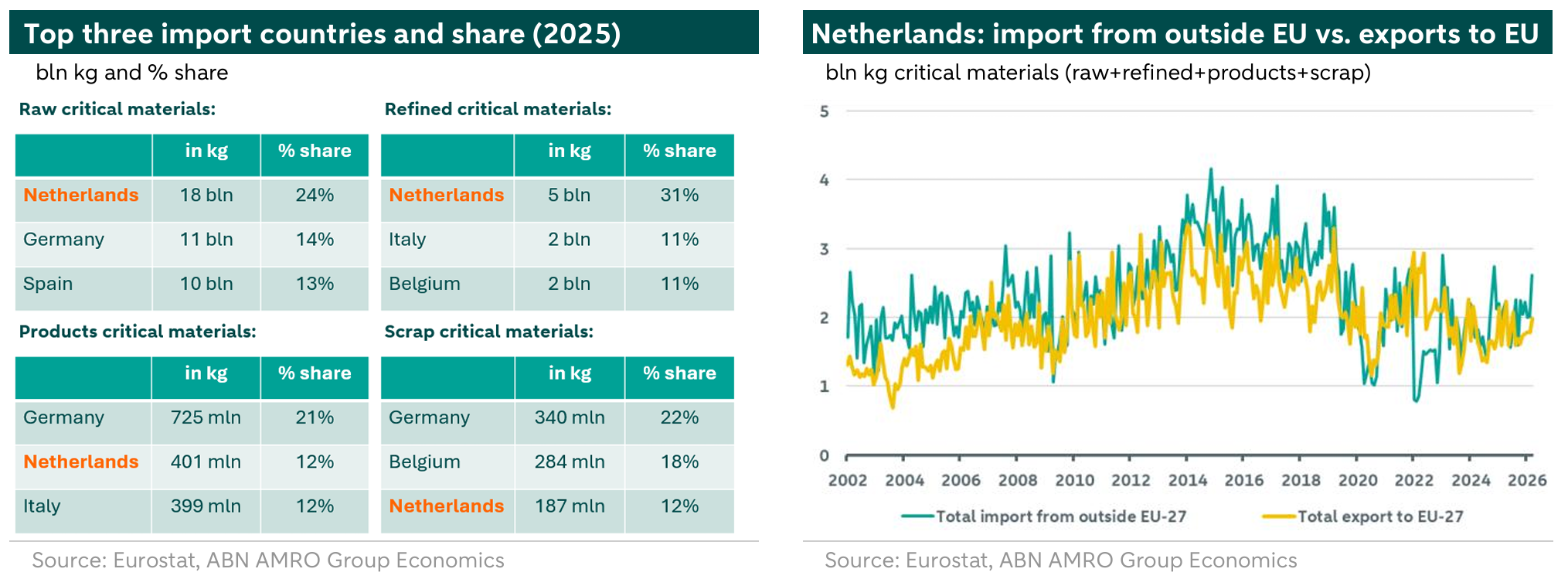

The Netherlands is the EU’s largest importer of critical materials and is therefore a key player in this field. Most imports consist of raw critical materials, of which coking coal – used in the steel industry – accounts for the vast majority. Officially, coking coal is classified as a critical and strategic raw material, although it is of lower value than other critical materials (such as rare-earth elements). However, even if we exclude imports of coking coal, the Netherlands remains a crucial player in the trade in critical materials, ranking second after Germany.

Most critical materials are destined for transit to other parts of the EU. No further processing is carried out on these critical materials, and on balance the Netherlands adds little value. This indicates that Dutch ports and the logistics infrastructure are of great importance to the trade in critical materials.

EU diversifies trade in critical materials

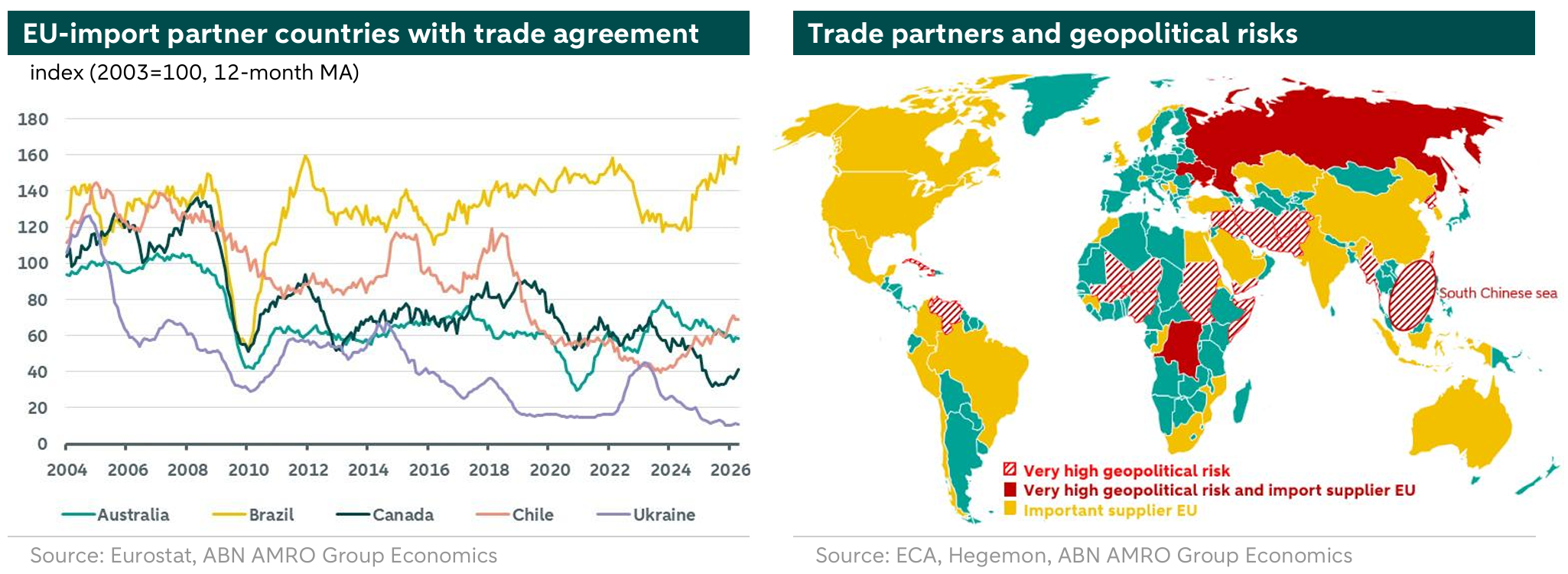

For a significant range of essential critical materials, China dominates global supply chains, and reliance on a single supplier (or a few) leaves economies vulnerable. China has regularly restricted the supply of certain rare-earth metals through export bans whenever international relations have become strained. The US and the EU are actively seeking alternative supply chains and attempting to diversify the long-term supply of critical materials to ensure continuity.

The EU has now established several strategic partnerships in the field of trade in critical materials, including with Chile, Australia, Ukraine, Norway, the Democratic Republic of Congo, Uzbekistan, Kazakhstan and Canada. In addition, the EU is in negotiations with Brazil to further diversify the supply of critical materials. Of all these partnerships, a significant volume of critical materials comes from Australia, with imports of alumina (a key raw material for aluminium production) dominating. However, import volumes of critical materials from Australia have been on a downward trend since the end of 2023, whilst those from Chile have been rising more sharply since then.

Eurostat trade figures also show that trade in critical materials with Brazil is booming, and that imports from Ukraine have fallen sharply since the war with Russia. It is here that the geopolitical risks for the EU are greatest. For the EU, most suppliers are often countries with a low geopolitical risk. Countries such as Russia, Ukraine and the Democratic Republic of the Congo are the exceptions to this. However, the risks associated with China also remain high, given the interests surrounding the South China Sea and Taiwan. An escalation here could strain international relations and thereby significantly reduce the availability of critical materials.

On balance, partnerships with resource-rich countries have so far done little to reduce supply risks. Imports of critical materials are declining rather than increasing. Furthermore, the relatively high energy costs in Europe are not helping, forcing production facilities to scale back their output or, in some cases, cease operations entirely.

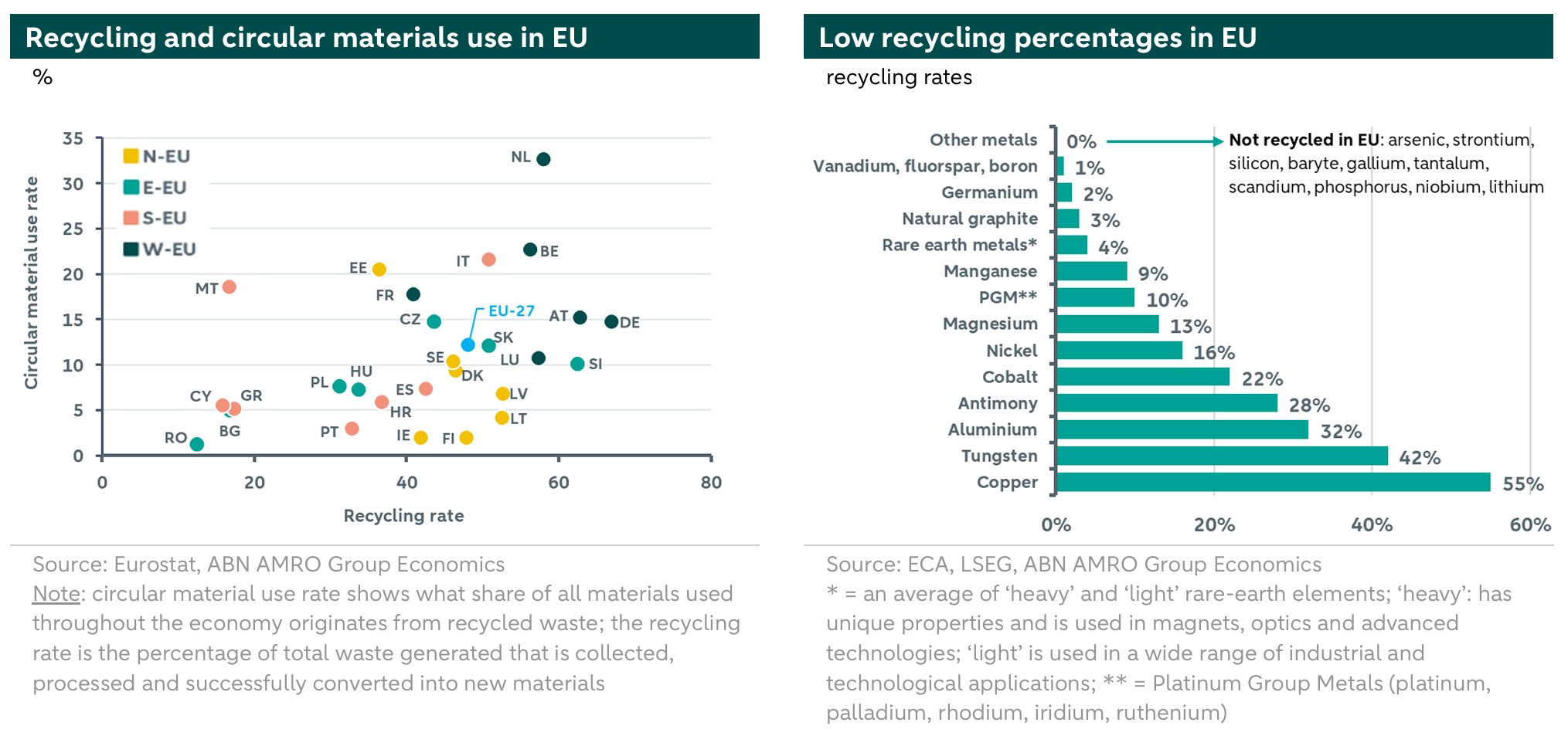

Recycling critical materials insufficient

Another source of critical materials is the material incorporated into products, infrastructure and waste streams. This stream can be of value to economies. It reduces dependence on imports from countries outside the EU (which carry higher geopolitical risks) and makes the supply chain less vulnerable.

Recycling rates in the EU are relatively high, particularly in Western Europe and in many countries in Northern Europe. However, recycling in Eastern and Southern Europe is still in its infancy. Recycling mainly takes place on waste electrical and electronic equipment that is collected. This allows base metals – such as copper, aluminium, nickel and cobalt – to be recovered in larger quantities. However, the quantity of recycled critical raw materials – particularly rare-earth elements – remains marginal. This is because the EU lacks the appropriate technology and industrial processes to recycle critical materials on a larger scale. Critical materials are often incorporated in microscopic quantities – sometimes in combination with other substances – into complex equipment. It is therefore not straightforward to rapidly scale up recycling capacity for critical materials in the EU, as, in addition to high research and capital costs, there is still considerable uncertainty regarding the economic viability of such projects.

Research and innovation are essential to accelerating the recycling of critical materials. This, too, requires investment, which could be provided in part through multi-annual EU funding programmes or via NGOs that make risk capital available to further scale up initiatives in the field of critical materials recycling.

Furthermore, supportive EU policies can also help to reduce the risks associated with investments in recycling capacity, including the provision of government guarantees for supply and procurement contracts with key end-users (such as manufacturers of clean tech or electric cars).

Promoting the circularity and recycling of critical materials is of fundamental importance to the EU and must therefore be high on the policy agenda. Not only from the perspective of reducing dependence on powerful external suppliers, but also for the transition to a climate-neutral economy.

Conclusion

Critical materials will continue to play a key role for the EU for the time being. The energy transition, digitalisation and the EU’s independence in the field of critical materials hinges on the availability of these raw materials. Although the EU is attempting to reduce its dependence on a few dominant suppliers by entering new trade partnerships, increasing processing capacity and boosting recycling, the figures show that this strategy has not yet yielded the desired results. At the same time, geopolitical tensions, high energy costs and international competition are putting further pressure on security of supply.

The analysis shows that Europe remains vulnerable due to its dependence on external suppliers, with China as the dominant player and relatively high global geopolitical risks that have the potential to severely disrupt Europe’s supply chains in the long term. The question is therefore whether Europe can afford to remain dependent on these external supplies, given that demand for critical materials is set to rise sharply in the coming decades.

One of the main challenges lies in strengthening the European circular economy. As long as the recycling of critical materials – and rare earth elements in particular – lags due to technological and financial constraints, the EU will remain vulnerable to external disruptions. Investment in research and innovation, the provision of government guarantees for projects involving critical materials, increased recycling capacity and strategic policy will help Europe to partially mitigate these risks.