Spotlight - Oil’s bearish turn premature, but worst looks behind us

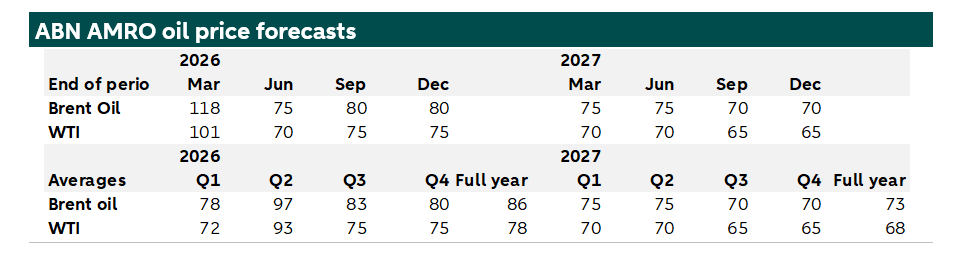

Oil prices have fallen sharply, but current levels appear low relative to tight physical market conditions. Inventories remain low, while summer travel and refinery activity should support oil demand. Supply is expected to recover next year, while demand growth should be limited by ongoing decarbonisation in transport. Our new end-year forecasts are USD 80 per barrel for Brent and USD 75 for WTI; for end-2027 we expect USD 70 for Brent and USD 65 for WTI.

Oil prices stayed relatively contained during the crisis, even though the IEA described it as the worst energy shock on record. This was due to several factors. The shock hit an oil market that was oversupplied at the start of 2026, and global decarbonisation trends and eurozone efforts to improve energy security helped to further soften the effect of the crisis. Most importantly, there were also several important offsets. On the supply side, the US kept oil production close to maximum capacity and exported a large share of its output, even as domestic inventories declined. Saudi Arabia, the UAE and Iraq were able to increase supply through pipelines, limiting the fall in oil exports.

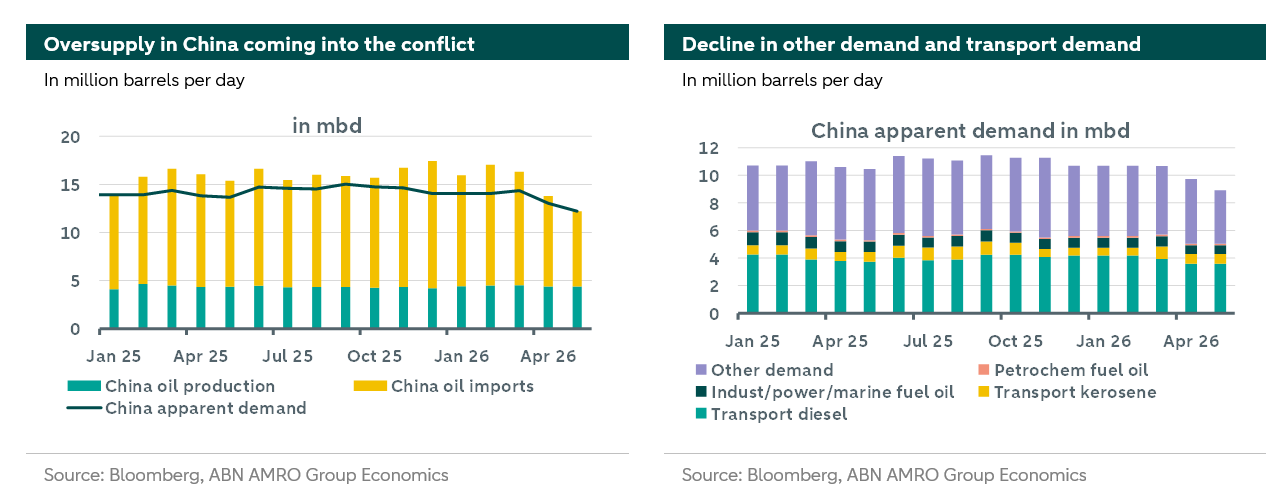

On the demand side, Chinese oil imports dropped significantly. Before the conflict, China had been importing more oil than it needed, adding the extra supply to its reserves. When the Strait of Hormuz closed, China was still able to secure a sizeable amount of oil from the Middle East, unlike Japan and some other Asian countries. China could also draw on its earlier supply buffer, limit its exports of refined products, and encourage domestic demand to shift away from liquid fuels towards coal and electricity, including electric vehicles. The chart on the left shows China’s oil balance, while the chart on the right shows which sectors recorded lower oil demand. Demand for diesel and gasoline in transport declined, but the largest drop was in “other demand”. It is unclear what this category includes, but we think it may include refined oil products, some of which are normally exported, mainly to the rest of Asia.

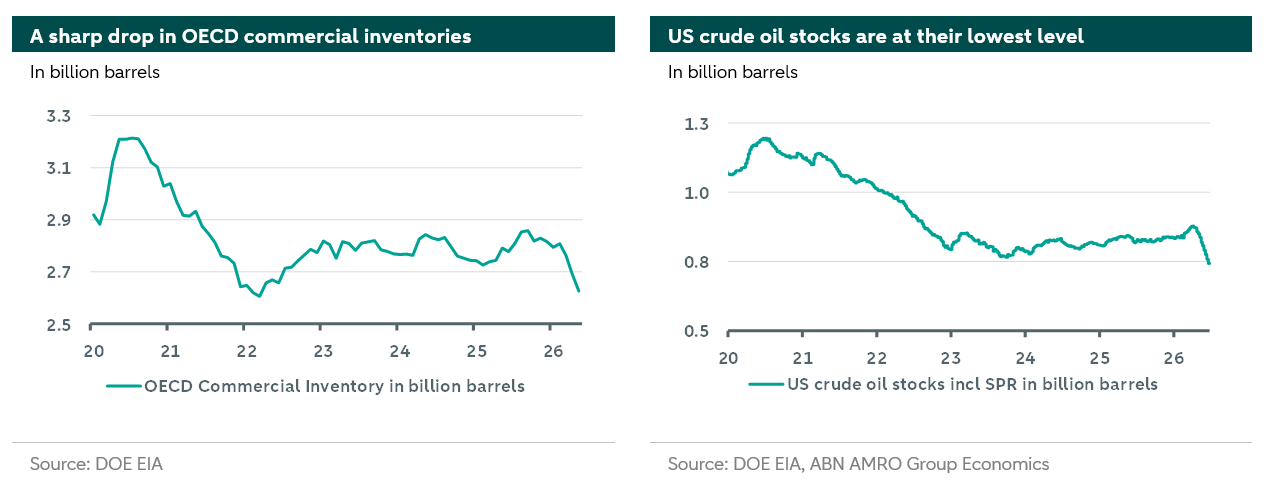

Despite the offsets the market was still in a deficit, so inventories fell sharply. Total global oil inventories are often estimated at around 7.5–8.0 billion barrels, but usable land-based reserves are only about half of that amount. The reserves that are reported are shown in the charts above. The chart on the left shows a sharp decline in OECD commercial inventories, which are approaching their 2022 lows. As the data are from the end of May, inventories are likely to have already have fallen below that level. The chart on the right shows US crude oil stocks, including strategic petroleum reserves, at their lowest level since the early 1980s. Putting these figures into further context, China’s crude oil reserves are estimated to have reached around 1.4 billion barrels by the end of 2025 after several years of reserve building, although these figures are not publicly reported. It is also not clear to what extent they’ve been drawn down over the past few months.

What to expect from oil prices going forward

Since the US and Iran agreed a Memorandum of Understanding and the Strait of Hormuz reopened, oil prices have fallen sharply to around USD 70 per barrel. This is more than 40% below the peak reached during the conflict and close to where prices stood when the conflict began.

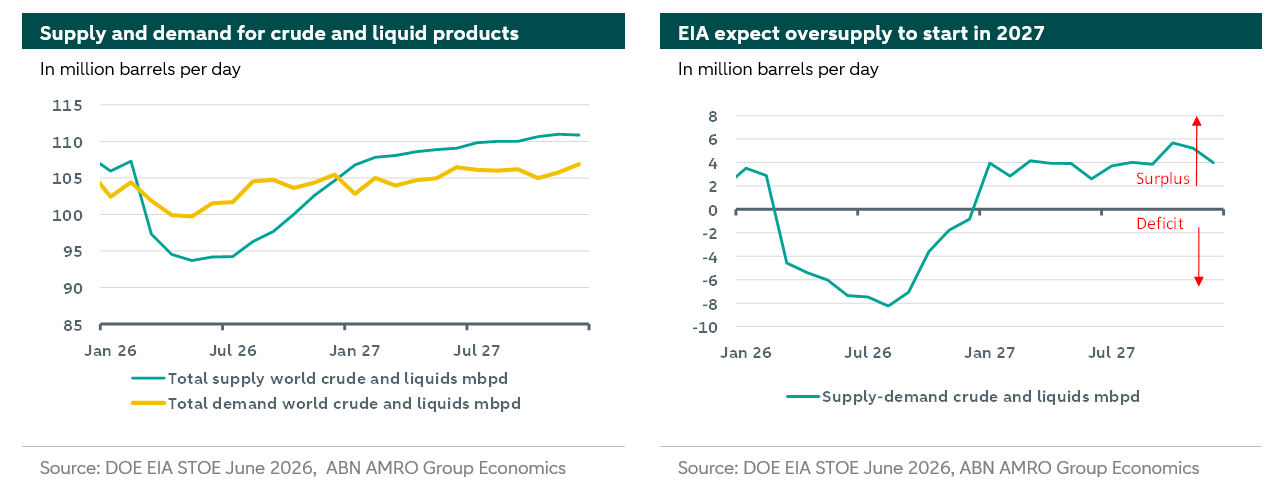

Looking ahead, we think the war risk premium in reference to the US-Iran conflict has now largely disappeared from prices. The strong US dollar has also contributed to recent oil price weakness. However, we do not think current oil price levels fully reflect the supply and demand balance in the market. Currently, oil prices and the forward curve appear to reflect expected oversupply next year but seem to ignore the undersupply this year. It will take time to restore oil supply in the Middle East. Meanwhile, demand is set to recover. Inventories are very low and prices are relatively attractive, so countries are likely to try to rebuild reserves to reduce their vulnerability to future shocks. Summer demand is also usually high, while product inventories, including kerosene, gasoline and other oil products, remain low. Refined product prices have fallen less sharply than crude oil prices, and refinery margins have increased. This is partly because Brent for immediate delivery has declined. This should support additional oil demand from refineries. On net, in line with the EIA, we therefore expect upward pressure on oil prices, and a continued drawdown of oil inventories this year. For next year, we expect supply to increase (see graph below on the left). This could come from the UAE after it left OPEC+, from Iran if the embargo is lifted, and from Iraq if it receives a higher OPEC quota. We also expect demand to recover, but to a lesser extent, as the transport sector continues to decarbonise, in particular the shift to electric vehicles. China is already well advanced in this process. As a result, we expect oversupply in 2027, as shown in the chart below right.

These dynamics are the basis for our revised oil price forecasts. We now expect Brent to end this year at USD 80 per barrel and WTI at USD 75 per barrel. For the end of 2027, we forecast Brent at USD 70 and WTI at USD 65 per barrel.